See also

Transports, emerging economies and industrial processes – Can oil really be substituted?

Get this executive brief in pdf format (free)

Climate change is urging the phase out of fossil fuels. Last December at COP28, a deal to “transition away” from fossil fuels was reached by the parties. Among them, breaking away from oil represents a massive effort and probably the most complex challenge to undertake globally. The IPCC has warned: any new oil well pushes the world further from a +1.5°C warming mitigation path. However, from crude to refined fuels, and in petrochemical industries including packaging and clothes manufacturing, oil is ubiquitous. Globalisation and transport infrastructures are still deeply oil dependent. Despite some improvements and the emergence of new alternatives, oil substitution remains puzzling.

In a world where petroleum fuels 92% of the transport sector, where plastic and fibres derived from oil are everywhere and where we use oil by-products every single day, what is the future of this widely spread commodity in the context of energy transition?

Through this report, Enerdata aims to shed light on the latest trends in the oil market, and the challenges associated with gradually replacing it as a primary source of energy in many sectors. Leveraging cross-country data and insights on supply and demand side, this brief provides a snapshot of the current trends, before diving into the transition pathways with a prospective analysis designed from Enerdata-POLES model.

GLOBAL OIL MARKET

Much more than fuelling cars

Oil is known to be widely used in the transport sector. It is one of the most important commodities in the world and a pillar of globalisation having revolutionised travel modes and merchandise transport. Crude oil is refined into various petroleum products for end-use. They are essential in many different sectors and value chains, not only for transportation. Oil is ubiquitous in our daily lives and the goods we consume.

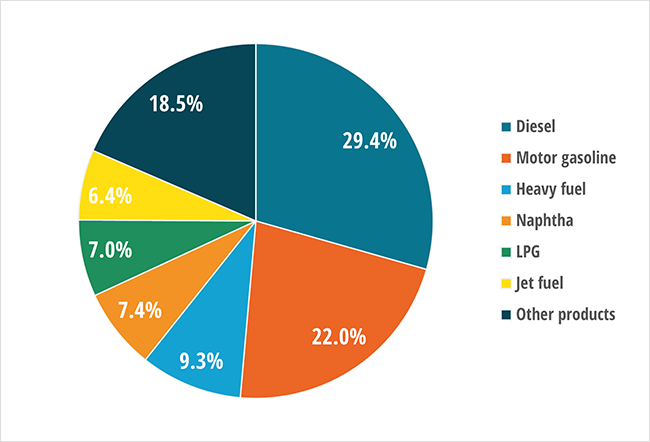

Figure 1: Global petroleum products output – 2023

Source: Enerdata, Global Energy & CO2 Data

Among the oil products, fuels for cars, ships, or aircraft represent more than two-thirds of refinery output. The other refined products are also crucial. They are notably used for heating and cooking (LPG), petrochemicals and plastics (naphtha), paving and roofing (bitumen), and other manufacturing activities such as textiles. For instance, around two-thirds of clothing is made from synthetic fibres, such as the well-known polyester, which is mostly derived from petroleum. But clothes are just an example among the thousands of goods containing oil derivatives.

The global effort required to wean our economies from oil is massive as it is present under miscellaneous forms and usages for which there are no or few substitutes.

Production side

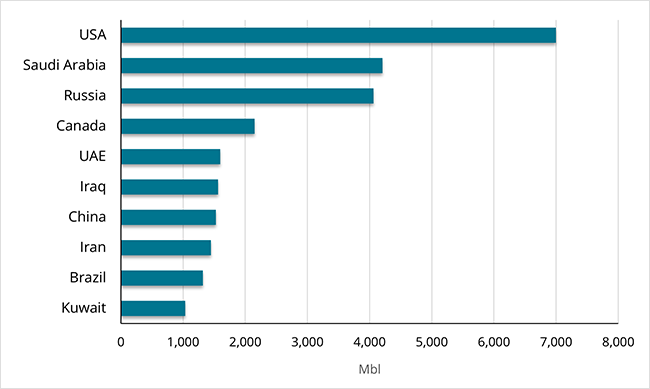

In 2023, the USA was the largest producer of crude oil and NGL by far, with 7,000 Mbl. The country’s production increased by a staggering 11% year-on-year, exploiting abundant shale oil reserves on top of the conventional ones.

Back in the early 2010s, Saudi Arabia and Russia were the largest producers with a production ranging from 3 800 Mbl to 4 300 Mbl per year. However, the USA accelerated the production drastically throughout the years by almost tripling the output from 2010.

Figure 2: Largest crude oil and NGL producers – 2023

Source: Enerdata, Global Energy & CO2 Data

Oil is a crucial resource for Middle Eastern countries which rely heavily on oil rents to sustain economic growth. The region represents 31% of global oil production with 5 nations ranking among the ten largest producers. Data from the World Bank (2021) estimated that oil rents account for 43% of the GDP in Iraq, 28% in Kuwait, 24% in Saudi Arabia, 18% in Iran, and 16% in the UAE. It reveals a crucial need for economic diversification in the Middle East to cope with energy transition stakes.

Alongside Russia, the USA, and Middle Eastern countries, Canada, China, and Brazil are also massive oil producers. Latin America and Africa are home to large oil fields, but the national productions are not sizeable to those of North America and Middle East.

A large share of global oil trade is controlled by the Organization of the Petroleum Exporting Countries (OPEC). The production of the member states1 combined represents 60% of the global supply. A large share of this production is exported, unlike the production in China or the USA being mostly consumed domestically. A larger group, the OPEC+, was founded in 2016 to include additional oil-producing countries such as Russia or Mexico.

The organisation has a strong influence in controlling the global oil market, deciding on the number of barrels produced by the members, which directly influences the price.

Demand side

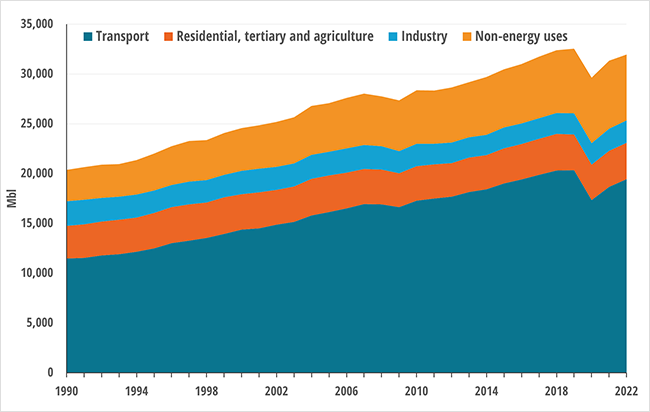

Apart from the 2008 financial crisis and the Covid-19 pandemic, oil demand kept growing every year since 1990. Over the past 30 years, final consumption increased by 57%. The distribution of demand among sectors didn’t significantly evolve, nonetheless.

Figure 3: Global final consumption of oil per sector

Source: Enerdata, Global Energy & CO2 Data

In 2023, final consumption of oil recovered to its pre-pandemic level after a 9.4% drop recorded in 2020. Overall, the transport sector accounts for 61% of total consumption, of which 47% goes to road transport. Industry represents 7%; residential, tertiary, and agriculture 11%; while non-energy uses account for the remaining 21%.

Oil represents almost all the energy consumed in the transport sector (92%). There is also a large demand for space heating in buildings and dwellings, and for various industrial processes.

The evolution of global demand for oil will massively depend on the activity and structural changes in the transport sector. An emphasis on the decarbonisation of the sector is presented later in this report.

At the country level, unsurprisingly, the USA and China are the largest oil consumers by far, followed by India, Japan, and Russia. It shows a tight correlation between GDP and oil demand.

Inelasticity of demand and price sensitivity

The demand for oil is quite inelastic to its price, as the historical trends have shown. The effects of price volatility and external shocks on oil consumption were much smaller than for other commodities.

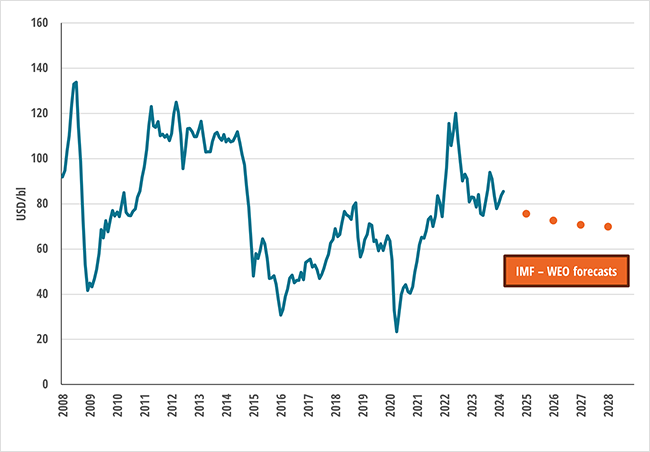

Figure 4: Brent spot price

Source: Enerdata, EnerMonthly

Brent (high-quality crude oil) price is a good reference for oil price worldwide. The monthly average data shows the volatility of oil prices over the past 15 years and their sensitivity to external shocks. OPEC strategic decisions, geopolitical tensions, and country policies on reserves exploitation are factors influencing the trading price. Monthly Brent spot price ranged up to more than $120/bl following the 2008 financial crisis and the invasion of Ukraine in 2022, and down to $23/bl due to an oversupply at the beginning of the Covid-19 lockdowns. In the coming years, the spot price for oil is expected to stabilise around $70-75/bl.

The pricing mechanisms will be different, nonetheless. As refined oil products feed 92% of global transports, trade and mobility still cannot occur without oil. Hence, as goods and passengers flow rise, the consumption of oil increases regardless of the price to sustain the extended demand. Historically, the price has been mostly driven by the level of supply. However, we can expect a more demand-driven price in the future as consumption starts to plateau or decrease in the longer term.

Since both supply and demand for oil are not very responsive to price changes, fluctuations can have a large impact on end-user’s purchasing power as well as on producing countries’ revenue. Furthermore, changes in oil price often impact the rest of the economy.

TRANSITIONING AWAY FROM OIL

The IPCC has warned that no more additional reserves should be exploited. Any new oil well moves the world further away from a +1.5 °C warming limitation path. Moreover, “limiting warming to 2°C or lower will result in stranded assets.” Experts estimate that about 80% of coal, 50% of gas, and 30% of oil reserves cannot be burned and emitted if warming is limited to 2°C. To limit global warming down to 1.5°C, significantly more reserves must remain unburned.

For the first time ever, at COP28 in December 2023, the parties reached on a landmark agreement to move away from all fossil fuels, including oil. Even though this agreement is still far from what is needed to maintain global warming below 2°C, it signals an acceleration of the global effort in transition.

The charts and figures presented in this section are derived from Enerdata-POLES model2 based on three scenarios: EnerBase, EnerBlue, EnerGreen. Explanatory documentation on scenarios definition can be found in appendix.

Future market: Oversupply and global peak demand by 2030?

Over the medium term, major international agencies and energy market experts anticipate a peak demand for oil between 2028 to 2030. From a global view, the oil demand is expected to plateau before gradually decreasing at the beginning of the 2030s. However, we observe strong regional disparities in forecasted consumption patterns.

Key sectors like shipping, aviation, freight, and petrochemicals are lagging in switching to alternative fuels. Hence, large areas of oil demand remain firmly entrenched.

Meanwhile, on the supply side, it is very likely that the market will be oversupplied. The OPEC+ is sticking to high demand forecasts for the next two years. Upstream oil and gas investments continued to increase in 2023, surpassing $US 500bn. This situation could drag the price down.

Additionally, new well drilling is still expanding especially in the Middle East where the economies massively rely on oil rents.

Structural and regional disparities – Economic growth influence on consumption patterns and Asia’s surging demand

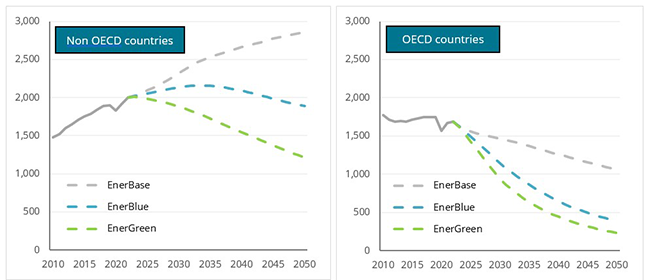

Developing economies are expected to see a rising demand for a longer period. As depicted in Figure 5, the demand in non-OECD countries is expected to grow at least until 2035 with the current state of policies. While the EnerBase scenario (business as usual) forecasts a continuously growing demand, the EnerBlue scenario (aligned with updated countries NDCs) sets the peak in 2034 for non-OECD countries. However, due to fast economic growth and energy affordability matters, final consumption of oil will remain high in developing economies. Over the longer term, it is expected to remain an important primary source of energy in many countries, even in the EnerGreen scenario (aligned with the Paris Agreement).

Figure 5: Final oil consumption forecasts - OECD vs non-OECD comparison

Source: Enerdata, EnerFuture

In OECD countries, final demand will start declining in the three scenarios. In 2023, a slight 1% drop was observed. This was notably due to the current conjuncture with sluggish growth, to efficiency improvements and a slow switch to other fuels such as e-fuels which can be used in various sectors and for which the production is slowly growing with renewables development. In OECD countries, it is very likely that demand already peaked just before the 2008 financial crisis and will now decline gradually. The magnitude of the decline will depend on the policies implemented and the level of investments involved to reduce oil consumption.

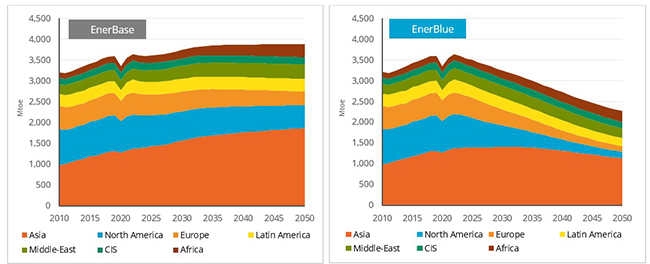

Asia is by far the region with the fastest growth in oil demand. China, India, and Southeast Asian emerging economies such as Indonesia, Thailand, and Malaysia, are driving up the demand. The region represents more than 1/3 of global final oil consumption, and this share is expected to climb to one-half in both scenarios displayed in Figure 6. As energy demand is increasing to sustain economic growth in Asia, the transport and industry sectors are absorbing larger volumes of oil. Undoubtedly, the capacity and pace of Asian countries to control and reduce oil demand in the coming two decades will determine the global transition path.

Figure 6: Final oil consumption per region

Source: Enerdata, EnerFuture

Different consumption paths are anticipated. Final consumption of oil is expected to grow in Africa to support the rise in population and economic development. Middle East and Latin America are likely to experience a rather steady pattern in oil consumption over the next 25 years, depending on whether stringent policies are implemented or not.

North America and Europe have historically been by far the largest consumers of oil during the 20th century and the early 2000s. However, if the stated policies to reduce oil use are thoroughly applied, we can expect a drastic drop in consumption by 2050. Currently, despite efficiency gains and the ongoing electrification of the transport sector, consumption remains high, tending to plateau rather than decrease. The USA remains the largest consumer of oil with a final consumption of 703 Mt in 2023.

How to reduce oil consumption and emissions in the transport sector?

The transport sector is the least diversified in terms of energy end use. 92% of the final consumption is filled by oil products. Oil is a crucial commodity for global trade as it fuels shipping, aviation, and merchandise trucks. Personal cars and motorbikes fleets are also constantly growing to serve population’s travel needs. Globally, the transport sector absorbs roughly 60% of oil consumption. Of this share, 47% is attributable to road transport. Hence, because of this oil dependency, the energy transition of the sector is puzzling, and it remains difficult to abate. However, the sector boasts fast innovation and new technologies readiness is evolving rapidly. As cleaner technologies such as electric vehicles (EVs) are becoming cheaper and more reliable, the demand for oil will tend to decrease in the long run.

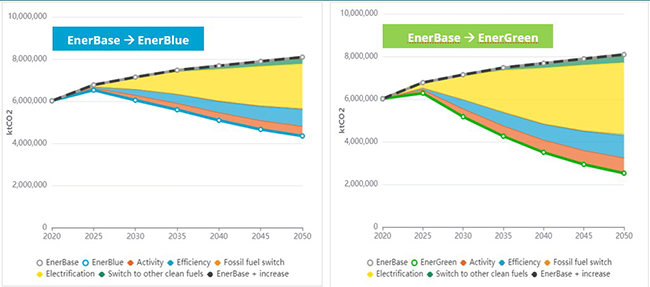

Enerdata’s Wedges tool assesses the levers for emissions abatement up to 2050. The figure below represents the contribution of various levers to shift from one scenario to another.

Figure 7: Transport sector – Global emission decreasing levers

Source: Enerdata, EnerFuture - Wedges tool

In both cases, electrification accounts for about two-thirds of the abatement efforts. A reduction in activity and passenger volume along with efficiency gains will also have a crucial role to play in reducing oil consumption and emissions subsequently. The development of biofuels and e-fuels is not to be neglected either as they are gaining significant market shares.

- Electrification

Among the solutions, electric vehicles (EVs) are at the centre of governments and manufacturers interests. EV sales have seen exponential growth from less than 1% market share 10 years ago to 14% of global car sales in 2022. Currently, China holds the largest market for EVs by far, being the number one manufacturer and having the largest fleet on its roads. While the USA and Scandinavian countries were early adopters, China’s market grew exponentially now representing 60% of global EV purchases and 35% of exports. China is also home to 80% of the Li-ion batteries manufactured worldwide which are crucial components of EVs. However, lithium’s scarcity will be a major issue over the medium and long term.

Manufacturers are also putting growing emphasis on developing electric trucks and buses. A lot of big cities around the world have recently significantly increased their electric public transportation offering.

- Activity and modal shift

Reducing activity and encouraging modal shift are also critical pillars to decarbonise the transport sector. In incentivising modal shifts and behavioural changes, governments have a key role to play. The development of public transportation infrastructures such as railways will play a pivotal role in developing countries, but also in the most advanced economies. In general, urban planning and reducing the average distance to all necessary infrastructures can help cutting the travel times and traffic. Behavioural changes from final consumers should also be encouraged. This could be accelerated by fiscal, and prices incentives on fuels, facilitating access to public transport (subsidies, larger networks) or even developing biking facilities and car sharing where it is feasible for small travel distances.

- Technology-based solutions with efficiency and clean fuels

Shipping and aviation are more challenging to decarbonise, and the improvements will come from technology-based solutions, coupled with slower growth in freight. However, it is very unlikely that we will see a reduction of flight volumes. But innovation in engine types can boost efficiency improvements for aircrafts, ships, and vehicles. To pursue an ambitious transition across sectors, changes in supply chain and logistics are expected. Globally, investments are growing to encourage the development of low-carbon fuels such as biofuels or hydrogen. These solutions boast a large potential but cannot be implemented on a large scale as it stands. Notably, carbon-free hydrogen production remains very limited.

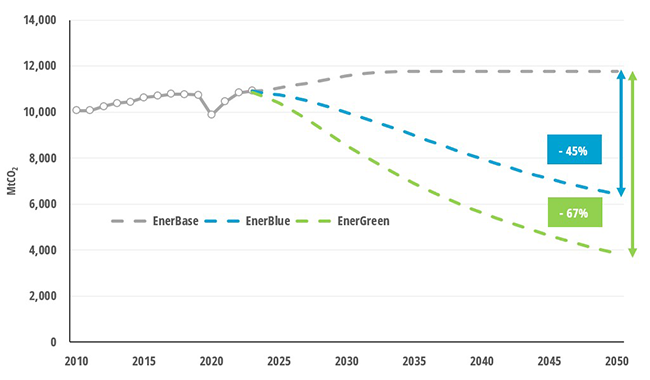

CO2 emissions pathways and environmental impacts

In 2023, oil combustion was responsible for 31% of global CO2 emissions from fuel combustion, after that of coal and mineral solids (47%). However, decreasing oil consumption is more challenging since substitutes for coal are more developed and affordable, especially in the power sector. Based on EnerBlue scenario aligned with the current NDC’s, CO2 emissions from oil combustion will hence decrease at a lower speed. Around 2035, oil emissions could be greater than the ones from coal.

Figure 8: CO2 emissions from oil combustion

Source: Enerdata, EnerFuture

Hypothetically, if all NDC’s and currently stated targets are thoroughly met, CO2 emissions from oil should be 40% lower by 2050 compared to the 2023 level (45% less than the BAU scenario mark in 2050). In the most ambitious scenario leading to a well below 2°C warming, emissions from oil combustion must be cut by 67% compared to the BAU trajectory.

On top of the global warming effects, oil and other fossil fuels burning is responsible for serious global health issues and environmental disasters. As a whole, fossil fuels are indirectly responsible for millions of deaths per year. WHO estimates that about 7 million deaths per year are attributable to outdoor and household ambient air pollution. Oil and fossil fuels in general are not the only sources of ambient air pollutants, but they contribute massively to the death toll. China and India record more than 60% of these deaths with big urban areas facing extremely high levels of air pollution which is the first cause of premature deaths.

Exploration and extraction of oil deposits is also harmful to the environment by disrupting the animal habitats and biodiversity. In the worst cases, accidents like oil spills in the sea are devastating with large ecosystems destruction and long-lasting pollution impacts.

KEY TAKEAWAYS

- Oil is much more than just a car fuel. It has been the catalyst of globalisation and remains a pillar of trade to this day. In majority of countries, daily life is flooded with unsuspected oil by-products.

- Crude oil exports is the main source of economic growth in the Middle East, where many countries sit on massive reserves and generate wealth and development by exploiting them. Despite the necessity to reduce oil drilling, the USA has recently accelerated their production substantially becoming the first global producer by far.

- The transport sector accounts for 61% of final oil consumption, 47% going to road transports. Oil is also an important source of energy for space heating and miscellaneous industrial processes in some countries. The largest economies absorb a very high share of global consumption.

- The spot price of oil is sensitive to external shocks and geopolitics. Historically, the price of oil has been more supply driven as the demand is quite inelastic due to the lack of substitutes.

- There are strong disparities in consumption patterns between advanced and emerging economies. Asia is the region with fastest growing demand for oil. It is very unlikely to see the demand decreasing in Asia, Middle East and Africa in the near future. In the scenario aligned with NDCs, the consumption in these regions should plateau, while North America and Europe to a lesser extent will have to drastically reduce consumption.

- In the transport sector, several decarbonisation levers to reduce emissions from oil combustion are clearly identified. Widespread electrification of road transport stands as the most impactful, notably with EV market growth. Modal shift and activity slowdown has also an important role to play. Technology-based solutions to foster efficiency and clean fuels can also help bridging the gap.

- All sectors combined; oil combustion represented 31% of CO2 emissions in 2023 (11GtCO2). To meet the pledges of the Paris Agreement, CO2 emissions from oil need to decrease by 60 to 70%. As of now, if NDCs are met, it would lead to a 40% drop, still insufficient to cope with the commitments.

REFERENCES

- IPCC, AR6 Synthesis Report, March 2023

- Cherif, Reda, Fuad Hasanov, and Madi Sarsenbayev (2024), “Call of Duty: Industrial Policy for the Post-Oil Era,” IMF Working Paper 24/74

- World Bank indicators

- Karn Vohra, Alina Vodonos, Joel Schwartz, Eloise A. Marais, Melissa P. Sulprizio, Loretta J. Mickley,Global mortality from outdoor fine particle pollution generated by fossil fuel combustion: Results from GEOS-Chem, Environmental Research,Volume 195, 2021

Notes

- Current OPEC member states: Algeria, Equatorial Guinea, Gabon, Iran, Iraq, Kuwait, Libya, Nigeria, the Republic of the Congo, Saudi Arabia, the United Arab Emirates, and Venezuela.

- POLES model: Global energy supply, demand, prices forecasting model.