- Update

-

- Format

-

2 files (PDF report, Excel file)

- Pages

-

73

- Delivery

-

Immediate by e-mail

Buy Water electrolyser manufacturing capacity report

Price without VAT. Depending on your status and location, VAT might be applicable. Get in touch with us for more information.

Overview

The growing focus on low-carbon and renewable energy sources, such as wind and solar, is accelerating innovation in hydrogen production and electrolyser technologies. Enerdata’s electrolyser report analyses the leading electrolyser manufacturers across the two most widely adopted technologies: alkaline and PEM (Proton Exchange Membrane).

Manufacturers are classified into three tiers based on their annual operational production capacity and market maturity. First-tier companies are market leaders with more than 1.5 GW of annual operational capacity and a proven record in large-scale energy projects. Second-tier players are fast-growing challengers expected to exceed 1 GW by the end of 2024, while third-tier companies have smaller capacities or are new entrants focusing on alternative or emerging hydrogen technologies.

Recent developments have also reshaped the ranking of key manufacturers. Chinese players such as SANY Hydrogen and Tianjin Mainland Hydrogen Equipment (THE) have advanced into the first and second tiers, respectively, while McPhy and HydrogenPro have dropped from the second tier. This shift highlights a broader industry trend — the rapid scale-up and growing dominance of Chinese manufacturers, mirroring patterns already seen across other clean energy sectors.

In recent years, a significant gap has emerged between the industrial manufacturing capacity of electrolysers and actual market demand, with only a limited number of large-scale purchase orders being placed to date.

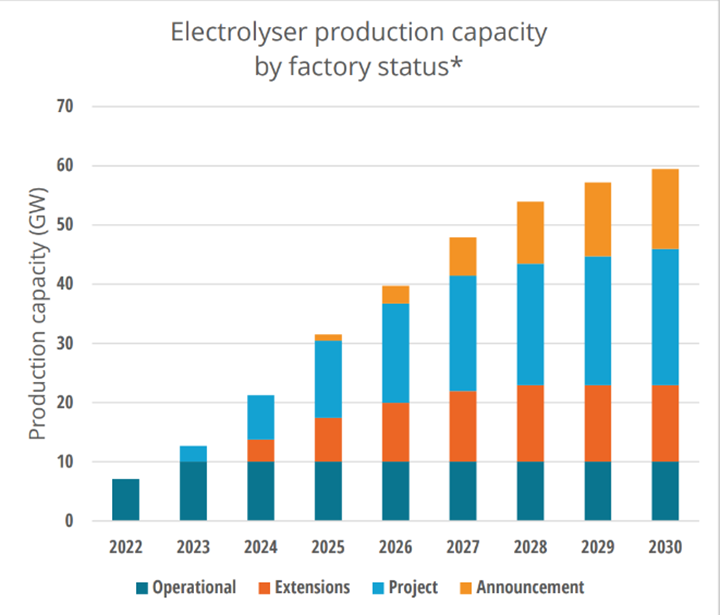

Electrolyser production capacity by factory status

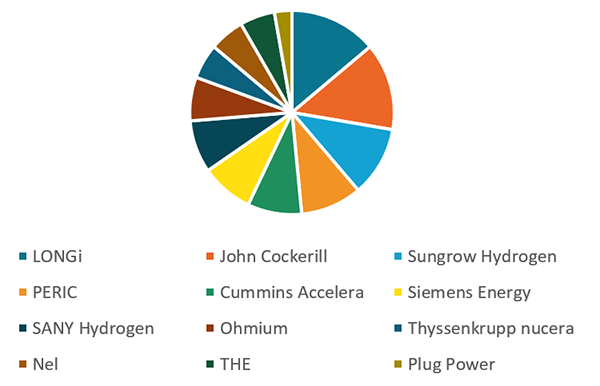

The main purpose of this report is to quantify the uptake of electrolyser manufacturing. We identified tier 1 and tier 2 manufacturers and integrators of water electrolysers over 156 industrial companies worldwide. This ranking of tier 1 and tier 2 companies is based on their existing and planned capacities up to 2030 and consists of 12 companies, among which there are LONGI, THYSSENKRUPP NUCERA, PERIC, SUNGROW HYDROGEN, JOHN COCKERILL, Tianjin Mainland Hydrogen Equipment (THE).

Each of these companies is profiled on their offer & technologies, finances, production & supply chain, and sales & project pipeline. We also localize each factory and provide a global analysis of key parameters such as investment cost, construction time, etc. Finally, we summarise by key region the installed capacity and put them in perspective with regional (European Union, U.S., China, South Korea, Japan, India, Canada) targets in terms of installations or H2 production.

The report's insights into key manufacturers, their capacities, and global installation status provide invaluable guidance for investors, policymakers, and industry stakeholders seeking to navigate the evolving landscape of green hydrogen production.

In this overview, we emphasise the importance of electrolyser on the way to reach net zero emissions. Their role in utilising renewable electricity sources, such as wind and solar power, is critical for a sustainable future. These insights into the size of the industry, its support from governments, and the years of research and development invested, highlight the direct impact electrolysers may have in shaping a clean energy future.

Discover in the report such topics, as:

- Electrolysers manufacturing capacity, globally and regionally

- Major electrolyser manufacturers – with a special attention to all 12 Tier 1 and Tier 2 manufacturers

- Hydrogen and electrolyser cost targets from companies

- Recap of USA, China, Europe, South Korea, Japan, India and Canada strategies on H2 and particularly green H2 production

Key Features

- Global coverage: from startup to corporate groups, all electrolyser producing companies are mentioned in the report. The special focus on leaders (in manufacturing capacity) is given, and all geographies are covered (Europe, North America, Asia), as well as all the technologies of electrolysis.

- Bottom-up approach based on equipment manufacturing: the forecast of production is built on exhaustive analysis of each of the 12 leading electrolysers manufacturers, in perspective of their project pipeline and cross-checked against multiple sources. It is a complementing approach to quantification based on the production of electrolyser that also helps differentiate the established makers from challengers out of the pool of participants in this market.

- Consolidated & summarized information by year, region, technology or factory project status, and the potential of H2 production from when the manufactured electrolysers will be installed.

Screenshots

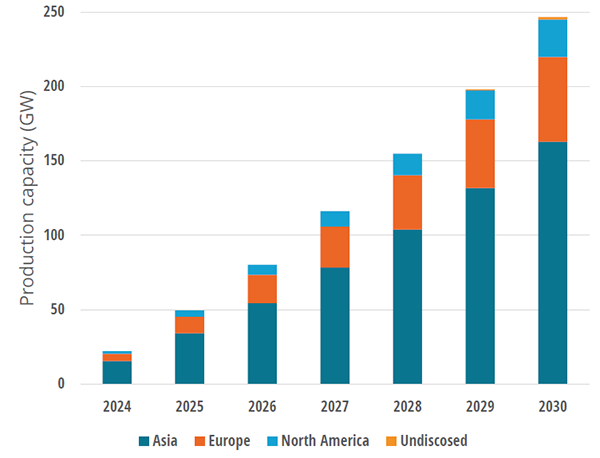

Cumulative electrolysers production capacity by region

Source: Enerdata electrolysers global manufacturing report

Manufacturer capacity by company