Four Scenarios for the Economy and the Energy Sector

After a decade of relatively steady economic growth and changes in the fundamentals relevant to the analysis of energy markets (energy intensity, changes in the mix, impact of policies, etc.), 2020 marks a sharp turning point with very deep breaks in most of the ongoing trends. In a forthcoming dedicated report, Enerdata will be analysing in detail these trends in 2020 so as their expected impacts.

But beyond 2020, what will happen? Whether it is in terms of economic activity or energy and climate policies, will we return to the previous situation? On the contrary, will we see an acceleration in the transitions? Will international cooperation experience a beneficial rebound or will we see a continuation of the step-backs already observed in recent years?

Patrick Criqui, emeritus research director at the CNRS and associate expert at Enerdata, gives us his analysis of possible scenarios for the years to come. Based on these scenarios, Enerdata is currently developing a quantified analysis of four possible developments for this pivotal period from 2020 to 2025...

It is impossible to say today what the future of the global economy will look like. First of all, because the sanitary crisis is not over. The most likely hypothesis is that, while waiting for a vaccine,if any, we may have to live through a series of aftershocks and new waves of disease spread. Each time, each of these may lead to new episodes of lockdown and slowdown. Secondly, because the future will be what governments and citizens make of it, in a context of economic and social difficulties and radical uncertainty.

The points of view expressed in all types of media, either in terms of observations or recommendations, are countless, and it is difficult to derive a clear vision of the future out of them. However, it is possible to try to identify, from the different points of view expressed, the main fault lines. These are all means of structuring plausible images of future trajectories and future states of the world.

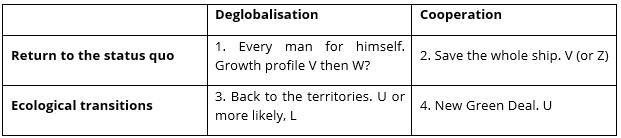

In the current debates, two sets of alternative choices can be identified, which can be combined to obtain four structural scenarios. The first relates to the state of international relations. Will we move in the post-crisis period towards a confirmation of a "deglobalisation", signs of which were already appearing before the health crisis? Or will we, on the contrary, see a return to international cooperation in the framework of a renewed multilateralism, due to a greater awareness of interdependence?

The second refers both to the aims and the means of the actions that will have to be implemented to restore economies and societies. Will the government seek the quickest possible return to the "status quo ante"? On the contrary, will they rely on the need for vigorous action by States to put economies and societies on the path of ecological transition, in a "building back better" logic?

For the next few years, up to 2030, the crossing of the two alternatives produces four scenarios. Each one presents a strong logic and internal coherence while being very contrasted with the three others. It is impossible today to give an opinion on their respective probability of occurrence. Let us simply note that each one is plausible:

- Scenario S1 combines the pursuit of deglobalisation and the search for a return to the status quo. It can be described as the "every man for himself" scenario.

- S2 is based on international cooperation aimed at avoiding a deep recession and the bankruptcy of many fragile states. Given the urgency of rescuing the economy, the demands of ecological transitions take a back seat or are largely forgotten. This is the "save the whole ship" scenario.

- The combination of the retreat of globalisation and ecological transitions results in the S3 scenario. It involves the relocation of productive activities and the search for greater autonomy: this is the "back to territories" scenario.

- Finally, the S4 scenario articulates the return of international coordination with an acceleration of energy and ecological transitions. This would be the European Green Deal scenario, or rather, in order to take into account the new situation into account a "New Green Deal".

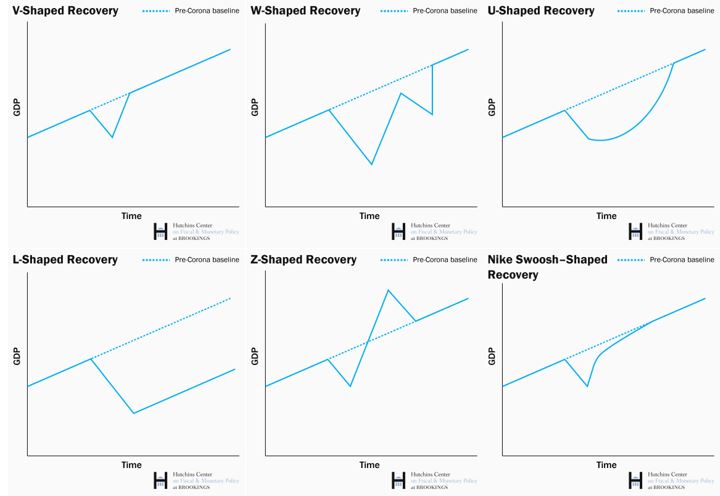

To this typology of possible futures, we can try to associate exploratory hypotheses on world economic growth and economic recovery. We must then consider different dynamic profiles for the recovery of the economy. Macroeconomists use a real alphabet system: profiles in V, W, U, L, or Z and Swoosh (Figure 1).

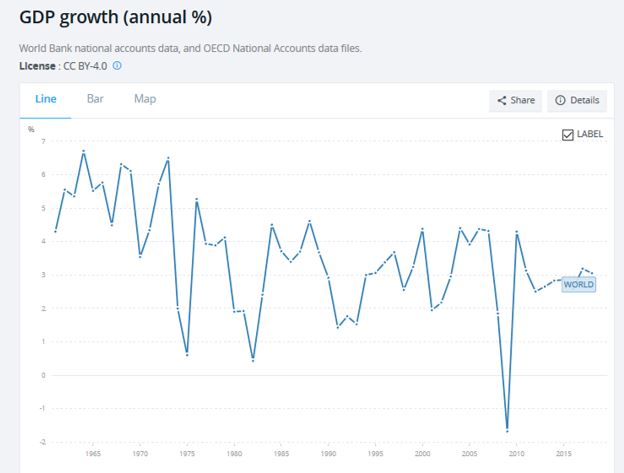

Over the last half-century, almost all of the patterns have been observed at some time, during the oil crises of the 1970s, the financial crises of the 1990s and finally the household debt crisis in the USA in 2008, followed by the European sovereign debt crisis (Figure 2). We will try to associate different types of recovery profiles to the four scenarios identified above.

Figure 2: Fifty years of growth and crises

Source: World Bank

Scenario 1: return to the status quo + deglobalisation = "every man for himself"

In this scenario, instead of leading to a refoundation, or even a simple different "after", the governments refocus on their direct short-term interests and reinforce their own tropisms and priorities (Dani Rodrik). In economic terms, it is a question of protecting themselves from external competition and relocating a large number of productive activities. For the USA, the objective is to resume the commercial and industrial conflict with China. For the other countries, it is to reverse a globalisation that is seen as bringing more destabilising elements than advantages in terms of lowering the cost of products and services (The China syndrome, David Autor). The economic response to the crisis aims to restore growth in the national economy as quickly as possible. The objective is therefore that of a rapid, V-shaped recovery. There is an emphasis on reviving existing activities independently of environmental considerations, or even a revision of existing protection policies.

On the energy front, the choice is therefore made to promote lower-cost solutions. In the short term, solutions based on fossil fuels are favoured, all the more so as the shutdown of part of the world economy is deeply lowering the prices of these energies. Oil consumption, driven by the restart of transport, is resuming, as is coal-fired power generation in Asia. Conversely, the crisis may adversely affect the development of renewable energies. Uncertainties and financing difficulties might hamper the development of new projects: even before the crisis, several governments were planning to revise, sometimes downwards, aid or incentive schemes (IEA). More generally, in both producing and consuming countries, brownfield activities (coal, oil, gas) are emerging as a means for lowering energy costs and save the economy. A V-shaped recovery is possible, but in the medium term a relapse remains possible. Either because of a second wave of the health crisis, or because of a mismatch between demand and supply on the commodity markets. That mismatch would generate price shocks: we would then have a W-shaped recovery and increased instability.

Scenario 2: return to the status quo + cooperation = "save the whole ship"

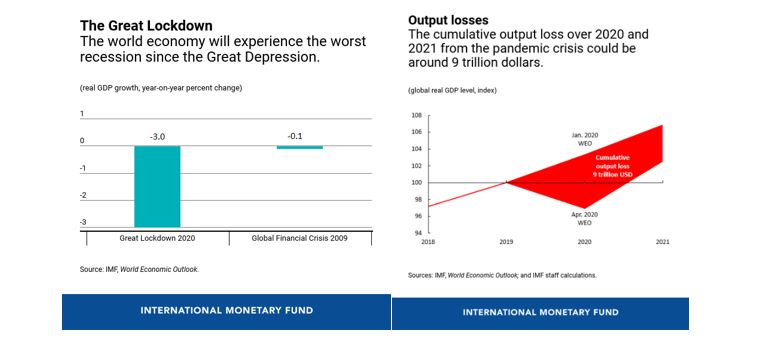

The first perceived threat is the default of many states in the South, but also in the North, which might be unable to pay their debts, thus worsening the international crisis. The risk is that of a major global crisis, comparable to the Great Depression of the 1930s, which the International Monetary Fund (IMF) has describe as the a Great lockdown crisis with a 3% decline in world GDP in 2020. The main consequence of such a development could be the bankruptcy of many fragile states, in the South but also among the most indebted countries in the North. The extreme urgency is therefore to introduce a debt moratorium and renegotiation, managed by the IMF and the World Bank (Reinhart and Rogoff). In a more Keynesian perspective, the introduction of liquidity through a massive injection of IMF Special Drawing Rights (SDRs) would help to amplify the recovery (Stiglitz). The expected result is a stabilisation of the economies and a rapid recovery of activity and trade. It would lead to a V-shaped recovery, or even a Z-shaped recovery if there is a strong rebound happens from 2021 onwards.

Figure 3: The great lockdown

Source: IMF

But this type of recovery, placing the urgency on the recovery of the world economy, may lead to sustainable development and the energy transition taking a back seat. Indeed, rescuing the economy can lead to an emphasis on a rapid return to pre-crisis consumption patterns, on safeguarding threatened businesses (automotive, air transport, tourism, etc.), and on investment in mature industries. In Europe, the question is whether the New Deal supported by Ursula Von der Leyen's Commission will resist the new priorities identified by the Member States and the delay imposed on certain "non-essential initiatives" (EURACTIV and Le Monde).

Scenario 3: deglobalisation + transitions = "back to territories"

The coronavirus crisis is part of a fundamental trend in favour of relocating activities (Thierry Gonard). Whether through an inability to implement strong international cooperation or rather through a deliberate desire to regain degrees of sovereignty through relocation, this scenario assumes that each State, each territory chooses to "rely on its own forces" to ensure ecological transitions. These are the result of a slowdown in consumption and a refocusing of industrial activity, the implementation of a new agricultural model and a regional planning that favours medium-sized cities more than metropolises (Dominique Bourg). The implementation of these new consumption and production models presupposes profound economic and social transformations. It therefore does not lead to a quick recovery, but rather to a gradual implementation. It would be a U-shaped or even a L-shaped recovery, taking into account the subsequent slowdown in GDP growth. Indeed, in this scenario, GDP recovery is no longer the primary objective and other indicators of well-being are favoured.

In terms of energy, this scenario incorporates a strong decrease in all polluting and fossil fuel-related activities, and the development of a greater degree of sufficiency makes the "consumption" engine of growth much less dynamic. The development of shorter production and logistics chains makes it possible to significantly reduce transport needs. In this scenario, renewable energies, in their decentralised configuration (photovoltaic, bioenergy, heating networks), play a major role for a carbon-free supply (example of the Greater Green project).

Scenario 4: cooperation + transition = « new green deal »

The shock of the coronavirus and the awareness of the risks incurred through global crises (virus or climate change) are leading to an awareness of at least some of the major players in the international community. They organize themselves to set up a reconstruction of multilateral institutions in favour of sustainable development, biodiversity protection, green investments and decarbonation of energy systems. A joint reflection is being conducted, for example between Europe, with its Green Deal (CEPS), and China, with the "new infrastructure" plans, OBOR and others (Criqui and Treyer). Coordinated "New Green Deals" are thus being set up, taking into account the lessons of the crisis for everything relating to security and environmental protection constraints. These investments are being put in place quickly enough to avoid prolonged stagnation. Consumption is mainly for green products, whereas investment is a powerful vector of growth. We then have a U-shaped recovery, or even a Z-shaped recovery if the economic spill over effect is quickly triggered, in a logic of reconstruction and green growth (Building Back Better).

This scenario refers to significant changes in energy efficiency and consumption patterns, particularly in transport (Mathieu Flonneau). But it is accompanied by a very ambitious effort to rebuild energy systems, mobilising all the innovations for low-carbon technologies. Among these, renewable energies should see very significant development (IRENA), whether in their decentralized or large-scale and grid-connected versions. The future of nuclear energy remains uncertain but it might be mobilized in some countries because of a significant decarbonated production potential. The same applies to Carbon Capture and Storage in industry or power generation.

What are the consequences for the oil market and prices?

One of the first questions raised by these contrasting visions of the future is related to the prices of fossil fuels at different time horizons. In a context marked by such profound uncertainties, forecasting in this area is obviously a high-risk activity. The dynamic adjustment of supply and demand on international markets will be the key to future price developments, whether upward or downward, regular or chaotic (Gonzalez Anaya). This adjustment will depend on the dynamics of demand and therefore on the economy and the supply side of OPEC, non-OPEC and non-conventional oil production.

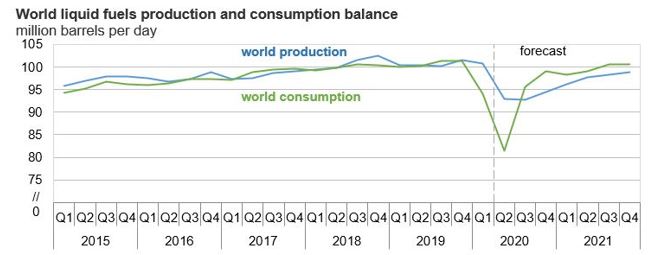

Figure 4: Oil supply and demand before, during and after…

Source: US Energy Information Administration

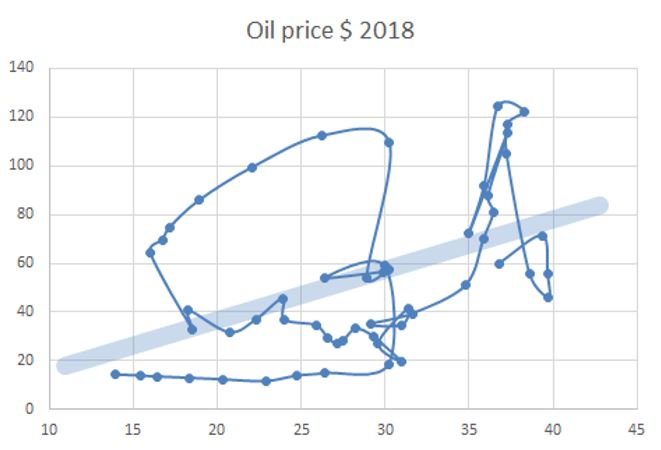

For oil prices beyond 2021 it is possible to refer to the so-called "snail's diagram" which makes it possible to observe, over more than fifty years, the historically observed relationship between oil prices and OPEC production. This relationship is complex and the diagram shows phases of over- and under-evaluation of the price, around a trend line that would correspond to a "fair price" or dynamic equilibrium price of oil.

OPEC production is in accounting terms equal to world production minus non-OPEC production. In order to project its evolution, it is necessary to assess the relative dynamics of world demand, which will be essentially dependent in the short term on economic (de)growth, and non-OPEC supply, which will depend on both economic factors (the variable cost of unconventional "marginal" deposits in the USA) and political factors (the production policy of major players such as Russia). At the height of the crisis, OPEC says it is ready to reduce its production by 10 Mbpd.

In the medium term, assuming a contraction in demand to OPEC of between 10 Mbpd (U or L recovery) and 5 Mbpd (V recovery), prices could then be expected to remain in the $30 to $50/bl range for several years.

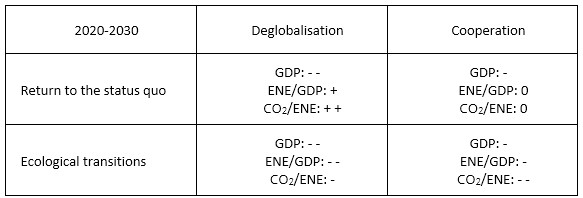

The fundamentals of the four medium-term scenarios (2025)

From an openly heuristic perspective and to open the debate, it is possible to attempt, from the “storylines” of the four scenarios developed above, a first characterisation - qualitative and before detailed quantitative modelling - of a few key variables.

It is possible to anticipate the framework of exogenous hypotheses of each scenario on the three key variables of the Kaya equation applied to greenhouse gas emissions. They describe the level of activity through GDP, the energy intensity of this GDP, and finally the CO2 content of the energy consumed:

CO2 = (CO2 /ENE) x (ENE/PIB) x PIB

Taking as reference a “central scenario” of 2019, like EnerBase, we will adopt the notation:

- for much lower,

- lower,

0 identical,

+ higher,

++ much higher.

In scenario 1 (status quo and deglobalisation) we will assume that the return to protectionism leads to a much lower level of activity (or an irregular W-type development). Energy efficiency efforts are slackened as they take second place in economic policies. The carbon content of energy increases a lot because the use of fossil fuels, unconventional hydrocarbons in the USA, and coal in Asia is less expensive in the short term and appears to be a central element of national strategies.

In scenario 2 (status quo and international cooperation), the decline in activity is less pronounced because cooperation allows a fairly rapid recovery, in V. Energy intensity and carbon content do not increase as in the previous scenario because the development of national fossil fuels is not a central element of national strategies. But they are not diminishing either because the energy transition objectives remain in the background compared to that of a rapid recovery.

In scenario 3 (transitions and deglobalisation), the level of activity, as measured by GDP, is much reduced, due to the weakness of trade and less emphasis on stimulating growth. The energy intensity of GDP is much lower thanks to the effects of the search for a greater sufficiency, at individual and collective level. The carbon content of energy is lower, with a significant development of renewable energies and a view to local supply and decentralized management.

Finally, in scenario 4 (transition and cooperation) the level of activity is slightly lower, as is the energy intensity due to the mobilisation of energy efficiency technologies. The decarbonisation of energy is very advanced because all the technological options are mobilised: from the very large-scale development of network renewable energies, to the use in certain countries of nuclear energy or carbon capture and storage.

This exercise is not a forecast because in a context of radical uncertainty it is impossible to deduce the future from the past. If these four scenarios are plausible, it is impossible to assess today their probability of occurrence. And still more to associate this probability with the desirability of each scenario. The most desirable is not necessarily the most likely ... but hopefully is the least desirable.

In any case, we can be certain that, at the end of the crisis, the political choices of governments, both in terms of international cooperation and the importance accorded to the imperatives of transition, will determine for several years the state of the world of tomorrow.

Patrick Criqui for Enerdata, May 2020

RELATED ENERGY ANALYSIS

Enerdata enlightens you on the consequences of Covid-19 and possible developments:

- Already available:

- Executive brief on the impact of Covid19 on energy consumption in France

- Global energy trends webinar

- Coming very soon:

- Global energy balance 2019

- 2020 forecast

- Coming soon:

- A detailed analysis tool for 2020 developments (by country - sector) is being finalised

- Regular updating of 2020 forecasts

- Analysis of possible scenarios over the period 2020 - 2025

- Development of a dedicated tool in progress

- Analysis from the scenarios published above

- Link with EnerFuture scenarios (horizon 2050)