Request the Publication (FREE)

The invasion of Ukraine by Russia in 2022 and its aftermath exposed Europe's heavy reliance on Russian natural gas imports, making its energy systems vulnerable to geopolitical instability and supply disruptions. This is even more relevant amid rising geopolitical tensions, as the new U.S. administration shifts toward protectionism and reassesses existing trade agreements.

At both EU-wide and member state levels, new policies and targets have been introduced to reduce the EU’s reliance on natural gas imports. Leveraging a customized hybrid methodology, we produced initial 2024 energy consumption estimates by sector to examine how natural gas consumption has changed since 2021, and more importantly assessed the drivers behind these changes and their respective contributions. Below are the key takeaways from this analysis.

Natural gas consumption in the EU has declined sharply across all sectors

The EU’s total natural gas consumption is projected to reach 10.6 TJ in 2024, reflecting a 4% drop from 2023 and a 23% decline since 2021. This marks a significant reversal of the previous upward trend, when natural gas was considered a transition fuel replacing coal in power generation. The largest reductions have been observed in power generation and industry, but households and services have also contributed. Given that switching energy carriers is typically a slow process due to infrastructure constraints, this rapid decrease raises important questions about the underlying drivers.

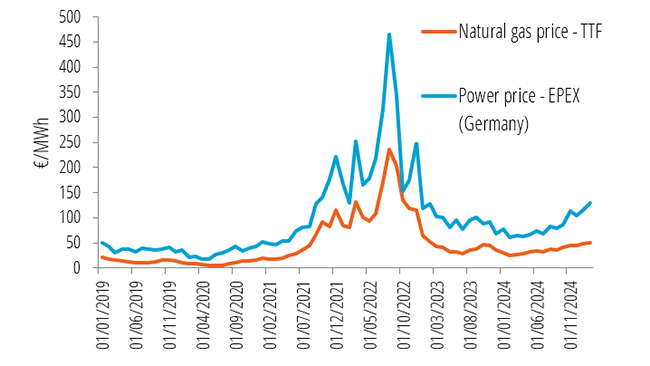

While difficult to quantify, energy sufficiency has played an important role in reducing natural gas demand

Breaking down the reduction in gas consumption shows that behavioural changes and sufficiency efforts played a key role. While an initial top-down decomposition suggests an important role for drivers such as fuel-switching and energy efficiency, a significant portion of the decline remains unexplained by technology alone, especially in such a short period of time, as fuel-switching and energy efficiency require investments in new equipment which don’t happen overnight. For instance, with regard to fuel-switching, end-users may have been able to replace natural gas by alternative fuels to an extent, but it is more likely that the decrease in the share of natural gas is linked to natural gas consumers were more exposed to higher prices and thus reducing consumption to a greater extent than other consumers.

Therefore, we conclude that households and businesses have actively reduced consumption in response to high energy prices, highlighting the role of sufficiency behaviours—i.e. consuming less energy rather than simply using it more efficiently.

The decline of energy-intensive industries has further reduced gas demand

While the overall manufacturing industry has remained stable (-1% since 2021), energy-intensive sectors such as metallurgy (-11%), non-metallic minerals (-15%), and chemicals (-10%) have seen sharp declines, largely due to high energy costs affecting competitiveness. This industrial shift accounts for 25% of the drop in industrial gas consumption. Additionally, the relative weight of less energy-intensive industries has increased, further contributing to the observed reduction. While this is classified as "fuel switching" in decomposition analyses, it is more accurately described as a structural economic shift, which may have long-term consequences for European industry.

Power generation from natural gas has dropped significantly, largely replaced by renewables

Electricity generation from natural gas has fallen by 26% since 2021, leading to a 1164 PJ reduction in gas input for power generation—accounting for nearly 40% of the total decline in EU gas consumption. While some initial switching in 2022 involved coal or oil, renewables have been the main replacement, with their share of total power generation increasing from 39% in 2021 to nearly 50% in 2024. The decrease in total electricity generation has also contributed to lower gas demand, as the EU’s overall electricity consumption has declined since 2021.

The electrification of final energy demand remains slow despite its importance for decarbonisation

Despite being seen as a key driver of the energy transition, electrification in final energy consumption is not progressing as expected. Electricity consumption across sectors has declined by 2% since 2021, and its share in total final energy consumption has only increased by 1 percentage point.

Key electrification technologies are starting to show signs of struggle, and their scope is very limited to specific uses:

- Electric vehicle (EV) sales have slowed dramatically (+0.8% in 2024 vs. +13% in 2023), even declining in some EU countries and represent

- Heat pump sales have fallen by 23% in 2024, and heat pumps only account for 8% of residential space heating.

Among the challenges that electrification is currently facing is the sharp rise in electricity prices during the energy crisis, which has partly discouraged both industrial and residential consumers from switching to electric alternatives. Additionally, low economic and demographic growth and the decline of energy-intensive industries have contributed to an overall reduction in energy demand, slowing down the need for electrification. This suggests that, in the short term, electrification is not yet driving the decarbonisation of final energy consumption at the scale needed to replace natural gas entirely.