Market status and potential

Get this Executive Brief in PDF format (Free)

Once insignificant in the European Union’s electricity mix just 20 years ago, solar PV has experienced a remarkable growth. By 2024, this energy source accounted for approximately 11% of the EU’s power supply and continues to expand at a rapid pace. To date, most of the capacity installed in the EU is on the roofs of buildings —both residential and commercial ones— helping to limit competition for land. However, the widespread adoption of rooftop PV, while beneficial for prosumers, also presents challenges such as grid congestion and rising costs for distribution grid operators. In this paper, we explore potential solutions to these limitations and examine the long-term role rooftop solar could play in achieving a net-zero energy system in Europe.

Recent developments in the solar PV market in the EU

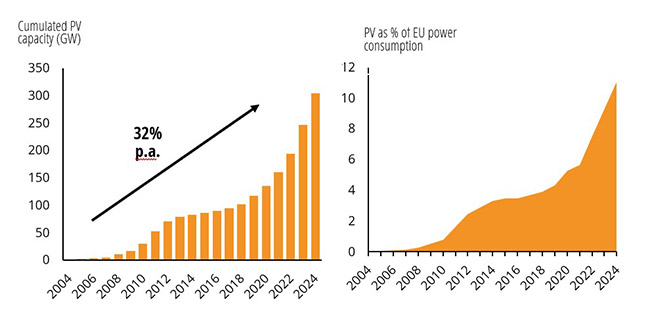

The solar PV market in the European Union (EU) has experienced explosive growth over the last 20 years. While the total installed solar capacity in the EU was only 1.3 GW at the end of 20041, it reached approximately 338 GW in December 2024, a remarkable 260-fold increase over the period (and a CAGR of 32% over 20 years). Of that total capacity installed today, Germany represents the biggest amount with close to 100 GW, followed by Spain, Italy and the Netherlands, with 47 GW, 36 GW and 26 GW, respectively2. Furthermore, despite slower growth compared to 2023, the annual installation rate reached an all-time high in the EU, with 65.5 GW installed in 2024. Of this, Germany accounted for 16.1 GW, Spain 9.3 GW, Italy 6.4 GW, and the Netherlands 3.0 GW—one of the few countries to experience a decline in annual solar installations. In addition, the share of solar PV in the EU’s power supply has surged from nearly zero in 2004 to approximately 11% in 2024. If electricity consumption in the EU continues to grow slowly —at around 1–2% per year— and if member states maintain an annual installation rate of approximately 60 GW, it is highly likely that by 2030, solar power will cover between 20% and 25% of the EU’s electricity consumption—a level currently reached only by Hungary in Europe.

Figure 1: Cumulated installed PV capacity (left), percentage of power generation from PV in the EU (right)

Source: Ember Climate

As can be seen in Fig.1, the rate of installation in the EU has not remained steady over the last 20 years. In the 2000s and the early 2010s, exponential growth was driven by relatively generous Feed-in Tariffs (FITs) in several countries, which contributed to the maturation of PV technology and a significant reduction in costs. As the supply chain was still in its infancy and relatively limited in scale, the cost of these incentives had little impact on public spending. The development of solar also had no meaningful physical consequences on the grid, as the generation was “diluted” in a mix largely dominated by traditional spinning generators such as thermal plants, nuclear and hydropower. The midday generation peaks did not cause significant drops in spot prices, as slight increase in production could be offset by adjusting other production sources

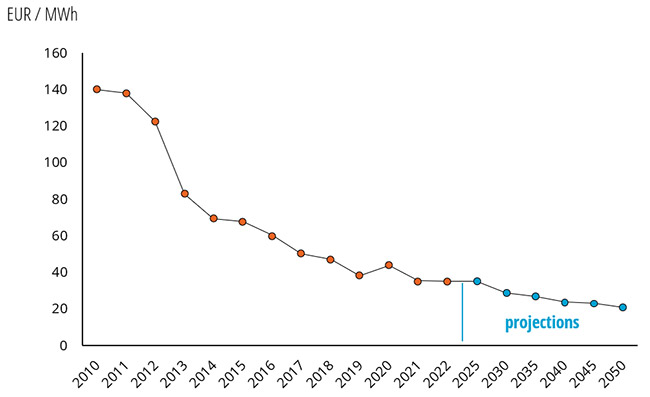

Figure 2: LCOE of utility-scale solar PV in Europe

Source: Enerdata, Power Plant Tracker

The PV technology has long achieved competitive price levels on the European continent and the LCOE of land-based power plants has fallen dramatically over the years (Fig.2). Even though rooftop solar generally has a higher LCOE than ground-based utility-scale plants, the trend has also been downward, especially for large C&I set-ups.

In terms of the division between utility-scale (land-based) and rooftop installations, rooftop panels have long dominated the European market in terms of both the number of installations and the total capacity added. Between 2020 and 2024, approximately 60% of new capacity was installed on roofs, even though the cost per unit of capacity was higher than for land-based set-ups.

Current landscape and future potential of the rooftop solar market in selected EU countries

While ground-mounted solar provides the advantage of allowing easier and faster deployment, some EU countries have expressed an ambition to prioritise rooftop PV installations and to restrict their use on land, in order to limit competition with agriculture and prevent land artificialisation. The rationale for such a policy is supported by several factors; among which is the fact that estimated rooftop PV potential is often highly significant (in the Netherlands, PV on buildings represents a potential of 143 GW, compared to a total identified potential 173 GW). In addition, locating panels3 i.e. on the roofs of residential and industrial buildings) reduces the need for costly upgrades to transmission and distribution grids, which can take several years in some countries. Furthermore, self-consumption of power produced on the roof can reduce taxes for end users, adding to the economic benefits of avoiding grid fees. However, achieving high self-consumption rates may incur additional costs, such as purchasing stationary batteries or adapting power usage to match the production profile. Some countries that have experienced strong solar PV deployment in previous years now appear to be reaching a saturation point where increasing grid congestion is hindering the development of new projects.

Situation in Netherlands

A striking example in Europe are the Netherlands4, where it can take up to 10 years to connect new projects to the grid. In this country, the advantages of rooftop setups have led to significant growth in rooftop PV, both on residential buildings with relatively low power levels (under 15 kWp) and on large commercial or industrial buildings with output capacities of several hundred kW with the largest such installations in the country reaching tens of MW5. However, after years of explosive growth, the Dutch solar market has stagnated in 2024, with the total installations in the country falling from almost 5 GW in 2022 and 2023 to less than 3.5 GW added in 20246. Residential rooftop installations in particular have halved, from 2.4 GW in 2023 to just over 1 GW in 2024. By contrast, although commercial PV installations have also decreased, the reduction has been limited (from 2.6 GW in 2020 to approximately 2.4 GW in 2024). The decrease in the residential market has been attributed by several experts to the approaching end of the net-metering scheme in January 2027, which has introduced uncertainty in the market.

Although the decrease in the installation rate of commercial and industrial (C&I) rooftop PV systems is less marked, observers anticipate that the market could also undergo a structural change. Indeed, while we demonstrate in this article that the rooftop resource is far from saturated, a closer look reveals that a significant proportion of rooftops cannot be fitted with standard PV panels. One reason for this is that the roof structure cannot support the additional weight of the PV modules. Innovative solutions such as lightweight PV modules are being investigated to address these structural limitations and create a “Blue Ocean”7 opportunity. Such roofs could represent around one third of C&I rooftop potential in the country and therefore represent new growth opportunities for developers.

Situation in Spain

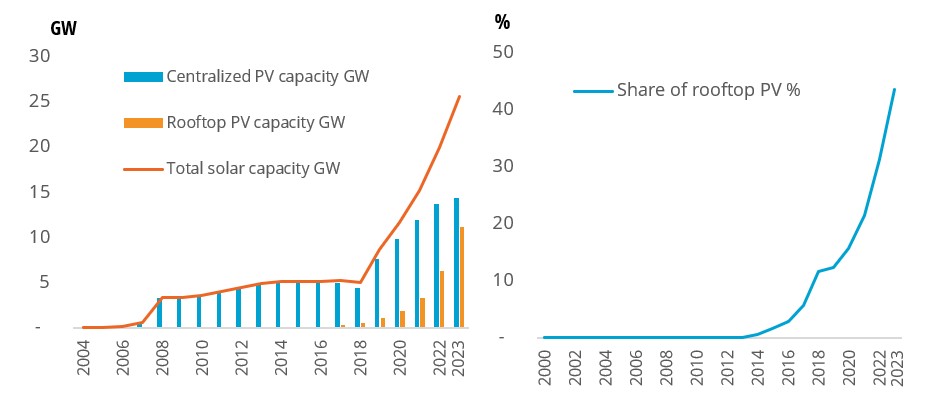

In Spain, rooftop solar installations are very dynamic, even though they slowed down in 2023 and 2024 compared to the very sustained pace experienced in the previous years. Of the 6 GW of solar PV installed in 2024, about 20% (1.18 GW) was rooftop solar, with installations on industrial buildings accounting for the majority (674 MW), followed by residential (275 MW) and commercial roofs (207 MW). This comes after 1.7 GW of self-consumption PV capacity installed in 2023 and 7.5 GW overall (including ground-mounted)8 led to grid congestion issues and a long connection queue. New rooftop installations usually sell surplus power to the grid under a net-billing remuneration scheme, resulting in very low returns at current electricity prices observed in the Iberian Peninsula. Even if the rapid development of stationary batteries and the greater flexibility of industrial and domestic power demand will progressively help to alleviate those problems, the pace of installations may not skyrocket in the foreseeable future for those reasons. For the coming years, the Spanish government has announced ambitious plans to develop solar PV as described in its 2023 NECP update. Specifically, the target is to install 76 GW of PV in the country by 2030, of which 19 GW will be dedicated to self-consumption9.

Figure 3: Evolution of solar PV capacity in Spain (left) and share of rooftop in cumulated capacity (right)

Source: EnerFuture

In the middle term (2030), the JRC has calculated for Spain a potential of rooftop solar self-consumption reaching 43.7 GW, with a production potential of 61.2 TWh per annum — equivalent to over 20% of Spain’s current electricity consumption.

Situation in France

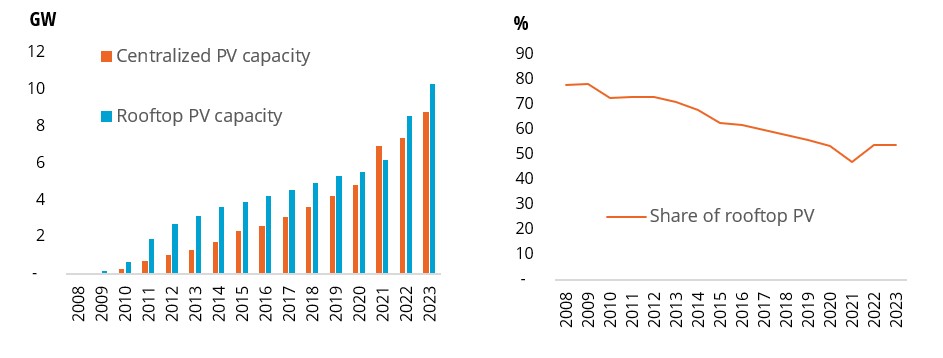

In the case of France, the most ambitious scenarios for solar PV plan an annual PV production of 150 TWh (Négawatt 2022) to 250 TWh/year (N1 and M23 scenarios of RTE), which would require in the order of magnitude 100 to 200 GW installed capacity, considering the current average production ratio of 1 300 kWh/kWp/year10. While it is relatively in line with the current ambitions of the government (100 GW by 2050), it is interesting to note that at least half of this production – if not the majority - could be supplied by rooftop solar installations. Studies have shown that that even with strict economic criteria (selecting only rooftop surfaces that would allow power generation below 0.15 €/kWh), around 125 TWh could be produced on French rooftops (compared to approximately 14 TWh generated by the 13.5 GW of rooftop PV in 2024). This estimate is nonetheless conservative, as other studies have much higher estimates, going up to 400 TWh per year of rooftop PV potential in France11. As can be seen in Fig. 4, the growth of solar PV was mainly driven by rooftop solar 15 years ago, but land-based centralised power plants picked up and the situation is more balanced today, with roughly an equal share of rooftop and land-based solar in France. The third PPE (Programmation Pluriannuelle de l’Energie), currently in its final consultation phase, aims for 57% of new solar PV capacity to be installed on roofs12. More specifically, 41% of new capacity is expected to come from small and medium-sized rooftop systems, while 16% is projected to come from large-scale rooftop installations on industrial, logistics, and commercial buildings.

Figure 4: Evolution of solar PV capacity in France (left) and share of rooftop in cumulated capacity (right)

Source: EnerFuture

From net-metering to net-billing: Economic implications for rooftop solar

At the beginning of the deployment of solar photovoltaic power in Europe, many countries used net-metering remuneration schemes for the excess power that was injected into the public electricity distribution grids. The rationale of this scheme is that when the net use of power consumption and power production (with solar PV) is positive, the meter counts the difference, which is sourced from the grid and will have to be paid by the customer. At the contrary, when the net use of power is negative, that is to say that the consumption is below what is produced behind the meter by solar panels, the difference (surplus) is injected into the grid, and the meter goes in reverse (it therefore “erases” previous consumption). Such a way to remunerate power injection into the grid is particularly advantageous for producers that can in a way use the grid as a kind of storage system, able to absorb excess production in the middle of the day and to give it back during less shiny hours. Nevertheless, in most European countries, with the massification of solar PV prosumers (i.e. consumers that also produce part of their electricity with rooftop PV) in the very last years, the amount of surplus solar power injected into the grid during shiny hours has started to be disadvantageous for distribution grid operators (DSOs), since the injection into the grid does not respond to the market signals (electricity SPOT price). Therefore, in a country with a lot of prosumers remunerated by a feed-in-tariff via a net-metering scheme, those prosumers tend to be overpaid at the expense of the DSO13.

One solution to this problem that has been adopted by several European countries is the net-billing remuneration scheme, in which the prosumers that inject surplus power into the electricity grid are remunerated with the market value of that energy, that is the SPOT market price. The idea is to align the interests of prosumers with those of grid operators and the wider community, by buying the surplus electricity at the SPOT power price, in order to give an incentive to either store or use the electricity produced by rooftop PV in the middle of the day and therefore maximize the self-consumption rate. One of the downsides of the net-billing scheme is that, without adaptation of consumption behavior on the prosumer side, the rentability of the PV installation will drastically decline. This could therefore slow the pace of rooftop PV rollout in the markets that have not yet a wide-spread adoption of stationary batteries or those where the use of power is not yet flexible (such as the countries with low adoption rates of electric heating and EVs). On the long-term, the net-billing remuneration scheme nevertheless appears to be a sine qua non condition for a generalization of rooftop solar that does not imperil the stability of the low-voltage grids and provides the right incentives to the economic agents.

The future role of rooftop solar in a decarbonised Europe

While the pace of solar PV deployment has experienced an explosive growth over the last two decades, recently boosted by the energy crisis following the Russian war of aggression against Ukraine, signs of saturation have appeared on several markets in the EU. The growth of rooftop solar PV installations has slowed significantly in the countries that were the most dynamic in 2022 and 2023, sometimes even declined in 2024. Nonetheless, since there are effective ways to circumvent the factors that are blocking the further penetration of solar PV in the most saturated electricity grids (with stationary storage and demand-side flexibility likely being the most impactful ones), the question arises to understand what share of the electricity supply could ultimately be provided by solar PV and particularly by rooftop solar, in the EU?

After having met approximately 11% of power consumption in the EU, total PV capacity (including ground-based) is set to reach approximately 14% of supply in 202514. At the end of 2024, building-integrated solar — the vast majority of which is rooftop — accounted for roughly two-thirds of cumulative capacity, totaling 220 GW15. Moreover, although land-based solar seems to be gaining traction, new installations in 2024 still consisted of 60% rooftop systems. Combining this data, it is likely that, by 2025, rooftop solar will supply close to 8% of total electricity consumption in the European Union — despite typically having a lower capacity factor than ground-mounted PV — and is on a strong upward trajectory. At the EU level, the potential of rooftop solar PV also appears to have tremendous long-term potential. As such, the Joint Research Center (JRC) has estimated the long-term potential for rooftop solar in the EU at 1.1 TW under conservative assumptions which, at today’s level of electricity consumption in the EU could cover about 40% of demand (considering an average production factor of 1 kWh/kWp/year). Even with a near doubling of electricity consumption in the EU to 5,000 TWh over the next 25 years — driven by the electrification of sectors such as heating, transport, and industry — rooftop solar PV could still supply more than 20% of total power demand. Other studies even estimate the technical potential of rooftop PV in the EU to reach 2,700 TWh of production by mid-century, which corresponds to the total electricity demand as of 2025. These findings tend to indicate that the limiting factor of the roll-out of solar PV is less the availability of roof space across the European Union16, and more our capacity to manage grid limitations and the intermittency of solar power — challenges for which effective technical solutions are now being deployed at scale.

To continue growing, the European rooftop solar market will need to adapt to an evolving context, particularly within the commercial and industrial (C&I) segment. Initially, rooftop solar developers targeted large, flat C&I roofs — the “low-hanging fruit” for sizable rooftop PV installations. However, this market is now showing increasing signs of saturation and intense competition in some countries. The next frontier of rooftop solar could be the estimated 30-40% of C&I buildings with weak load carrying capacity, which remained unequipped in the recent years, due to the heavy weight of traditional ballasted solar panels. Innovative solutions, such as lightweight solar modules appear to be a way to conquer those vast surfaces of roofs. Even though such roofs are more challenging to equip, they represent a lot of new opportunities for market players willing to adapt — and may prove decisive in leading this transition.

KEY TAKEAWAYS

- Solar PV has experienced explosive growth in the EU over the last 20 years.

- The majority of cumulated PV capacity in the EU is rooftop-based.

- Rooftop solar markets are becoming increasingly saturated in several EU countries due to technical and economical constraints.

- Sustaining rooftop solar growth requires adapted remuneration schemes as well as technical innovations (batteries and flexibility of consumption).

- If current constraints are addressed, rooftop PV has a strong potential to continue significant growth and approach its technical potential in the coming years.

Notes:

- Ember, Electricity Data Explorer, 2025.

- Solar Power Europe, EU market outlook for solar power, 2025.

- IEA, Electricity 2025, 2025

- Taiyangnews, Netherlands Discussing Space For Solar PV, 2023.

- IEA, Grid congestion is posing challenges for energy security and transitions, 2025.

- 18 MW for the site of Heylen Energy in Venlo, 25 MW for a site developed by Sunrock in Rotterdam.

- DNE research, Nationaal Solar Trendrapport, 2025.

- Blue Ocean Strategy - Wikipedia

- UNEF, Annual report, 2024.

- Ministerio para la Transición Ecológica y el Reto Demográfico, HOJA DE RUTA DEL AUTOCONSUMO, 2021.

- CNRS, Le solaire photovoltaïque en France : réalité, potentiel et défis, 2025.

- Ademe, Mix électrique 100% renouvelable ? Analyses et optimisations, 2016.

- Ministère de l’Aménagement du Territoire et de la Décentralisation.

- Sustainable Energy Technologies and Assessments, Transitioning from net-metering to net-billing: A model-based analysis for Poland, 2024.

- IEA, Snapshot of global PV markets 2025, 2025.

- Europe-on, SolarPower Europe Report | Flexible buildings, resilient grids, 2025.

- Applied Energy, Modelling the building-related photovoltaic power production potential in the light of the EU's Solar Rooftop Initiative, 2024.