More market integration, less public support: when the latest competitive auctions in renewables drive the prices lower to foster the energy transition

Get this executive brief in pdf format

Renewable electricity development has boomed over the past decade as the results of rapid industry maturity progress and government support intervention. This brief analyses renewables support mechanisms with a look at their evolution and effectiveness, and whether renewable power generation can hold its own against fossil fuels without them.

Introduction

The climate emergency is pushing most governments to enhance their national ambitions to lead the energy transition and decarbonisation of their economies. The development of electric capacities and production from renewable energy sources (RES) in the national power generation mix is one the core pillars for climate mitigation.

- In the European Union (EU), as part of their integrated national energy and climate plan for the period 2021-2030 (NECP), each Member State set long-term objectives to develop the RES capacities and reach the EU’s 2030 energy and climate targets. For instance:

- France aims to double the installed RES capacities by 2028 compared to 2017, with an installed capacity of 101 to 113 GW by 2028.

- Germany targets 200 GW of installed RES capacities by 2030 to see RES account for 65% of electric power consumed in Germany by 2030.

- In its “Energy Supply and Consumption Revolution Strategy (2016-2030)”, China released an objective of more than 50% of non-fossil power generation in total power generation by 2030.

- In the USA, the State of California will develop 25 GW new RES capacities to reach the target of reducing greenhouse gas emissions to 46 Mt by 2030, 56% below 1990 levels.

Over the last decade, more than 2,180 GW new cumulated electric capacities were installed worldwide, of which 1,250 GW were from renewable energy sources (including hydro), i.e. 57% of the new installed capacities (Enerdata Global Energy & CO2 Data; 2010-2019). New RES power capacities accounted for 75% of all capacity additions in 2019, a 6% increase (+172 GW) compared to 2018’s new RES capacities. Solar kept leading the RES capacity growth with +97 GW (57%), followed by wind with +60 GW (35%). Total RES growth was nearly triple the fossil fuel growth, continuing the dominance of renewables in power expansion since 2012.

Asia is leading the RES capacity expansion with 92 GW additions in 2019 to reach 1,130 GW installed RES capacities. China alone stands for 30% of the total RES capacities in the world, with 60 GW new capacities and 770 GW total installed capacities in 2019. Europe and North America follow with respectively 24% and 14% of the global RES share (Enerdata Global Energy & CO2 Data).

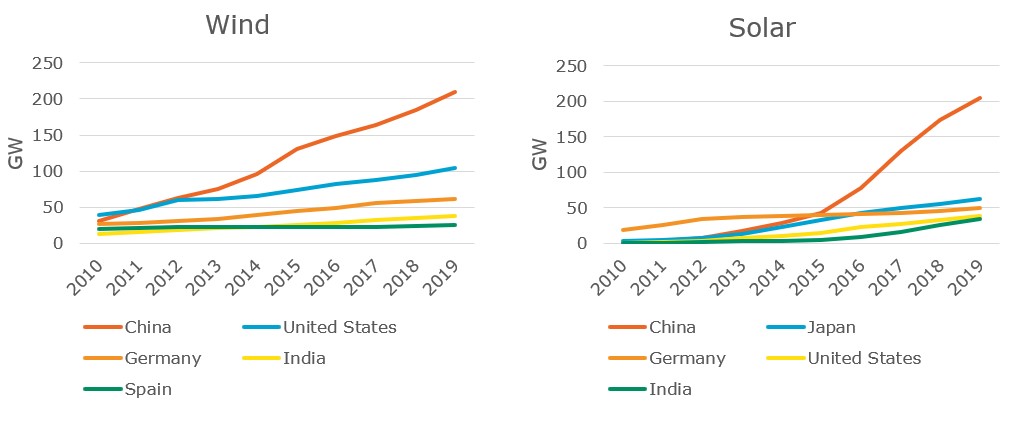

Figure 1: Growth in installed electric capacities from solar PV and wind for the top 5 countries

Source: Enerdata, Global Energy & CO2 Data

As illustrated above, China contributed the most to wind and solar PV technology development over the past decade, with an average annual growth of 21% for solar and 73% for wind. The USA takes second place in wind with 104 GW installed capacities in 2019, while the second rank is attributed to Japan for solar PV with 62 GW installed capacities. India accelerated the growth pace in solar PV technology over the past three years with +50% and had 34 GW installed capacities in 2019.

Because of insufficient technology and market maturity, the recent penetration of renewables in the power generation mix does not owe its success to free energy market alone but rather to support interventions from national power policies. As a strategic issue for addressing both climate change and industrial leadership, states have financially supported RES technologies since the early 2000s to offset their negative profitability levels at their early stage of development.

A look back at RES public support schemes and related forms of financial support instruments

The USA and Germany pioneered the use of RES support policies in 1978 and 1990, respectively. Denmark may be considered as one the most advanced countries in the design of public support schemes. Today, most developed and emerging countries have set out public support schemes which take different forms depending on the RES technologies, dedicated national budget levels and market maturity. Public support can be allocated through direct upfront investment grants, promotional loans, or in the form of tax credits and exemptions. However, direct support to the electricity prices is the most common mechanism used by the countries as it gives a predictable regulatory framework that reduces the market risk for investors.

Price-based support schemes are distinguished according to two main design components:

Market exposure

This means the exposure of public support to wholesale electricity market prices and their volatility. RES power generators will be granted with a feed-in-tariff (or FiT) when the national energy regulator/authority agree to offer them long-term (typically 15-20 years) purchase agreements for the sale of RES electricity at a pre-determined fixed price, irrespective of the market variations. FiTs levels are usually based on RES generation costs (e.g. LCOE approach) and may be timely adjusted during the purchase agreement term. Alternatively, policy designers may connect the price-based public supports towards more market integration thanks to so-called feed-in-premiums (or FiP) granted to RES generators on top of the electricity market price. Therefore, FiP are dependent on market prices and may be fixed or variable (aka. sliding) with or without cap and floor prices adapting to market prices variations and so limiting price volatility risks for RES plant generators and subsidised windfall profits at the same time.

Support allocation mechanisms

They either follow administrative procedures set by the national energy regulator (e.g. registration lists) or competitive bidding procedures where RES generators compete through auctions to set price levels of the FiT or FiP and control the allocated RES volumes. In RES auctions, the competitive price building mechanism implies a high cost-effectiveness of the system, so long as sufficient competition was created with demand for support higher than the auctioned volume. Most RES auctions are reverse auctions where a simple or multiple item(s) of a product (i.e. RES power) are sold by several competitors to a sole buyer. To guarantee a high realisation rate of RES projects, the design of auctions often includes pre-qualification criteria (e.g. permits, etc.) for participants to meet and penalties in case of delays or project failings.

The implementation of generous RES support schemes at the end of the 2000’s and early 2010’s have driven down the cost of solar and wind technologies and projects, which has, in turn, favoured a deeper market integration and has enabled the large deployment of feed-in-premiums allocated by auctions procedures. Indeed, if administratively based feed-in-tariffs are highly effective to support the development, they are not market-oriented and may unduly distort price competition between project developers and thus reduce RES cost effectiveness. With solar and wind technologies becoming more and more mature, FiT-based policies are gradually being supplemented or replaced by sliding feed-in premiums and RES auctions. This in line with the European Commission Guidelines on State aid for environmental protection and energy 2014-2020 advocating in favour of market-based instruments. Today, FiTs and FiPs often coexist where FiPs are granted to large-scale RES projects as output of auctions, whereas administrative FiTs are offered to small RES projects, which cannot access the wholesale electricity markets.

Next to price-based support schemes, a few EU Member States (e.g. Belgium, Sweden) and trading partners (e.g. the USA at State level) used or are using another RES support policy instrument : the RES quotas obligations based on tradeable green certificates (i.e. TGC). It is a volume-based support scheme with a RES target expressed in RES-share in final electricity consumption or in volume of produced electricity. Market participants (e.g. power producers, suppliers, or grid operators) are statutorily required to buy and clear green electricity certificates. The number of green certificates to buy corresponds to the RES quota obligations multiplied by the volume of electricity supplied annually to the final consumers. Selling the green certificates constitute a complementary source of revenues for RES generators in addition to wholesale market price of the final energy sold. Green certificates are market-driven and enable a competitive price determination through the interplay of demand and supply for TGCs. But they fully expose the RES generators to market price volatility. Besides, to ensure a demand for TGCs, a penalty mechanism is set out when participants do not meet the legally annual required number of certificates. The recent substitution of the RES quotas systems in the UK, Italy and Poland with price-based support mechanisms suggests a trend side-lining the green certificates in Europe.

Figure 2: Schematic illustration of main RES support schemes and their relation to electricity market price

Source: Banja M., Jégard M., Monforti-Ferrario F., Dallemand J.-F., Taylor N., Motola V., Sikkema R., Renewables in the EU: the support framework towards a single energy market - EU countries reporting under Article 22(1) b, e and f of Renewable Energy Directive, EUR 29100 EN, Publication Office of the European Union, Luxembourg, 2017

Eventually, as RES technologies are increasingly gaining market competitiveness, RES developers can shift from public support schemes to private market instruments like Power Purchase Agreements (PPAs). Negotiated between a power producer and a power consuming company (“Corporate PPA”) or a power trader (“Merchant PPA”), PPAs are long-term bilateral agreements notably defining the quantity of electricity to be supplied, the purchase prices and potential penalties for non-compliance. PPAs are tailored made and enable to secure new capacities funding for RES project developers and long-term price visibility for power consumers. The USA is still the first market for corporate renewable PPAs, where US technology companies (i.e. GAFA) are leading the rankings. RES-based PPAs are an increasingly popular tool for large companies which are committed to reduce their greenhouse gases emissions.

RES auctions globally drive the prices down, but careful attention should be paid to assess their effectiveness

RES auctions are becoming a central tool for RES policymakers and project developers: from 6 organising countries in 2005 to more than 100 in 2020. Past awarded bid prices show a downward trend.

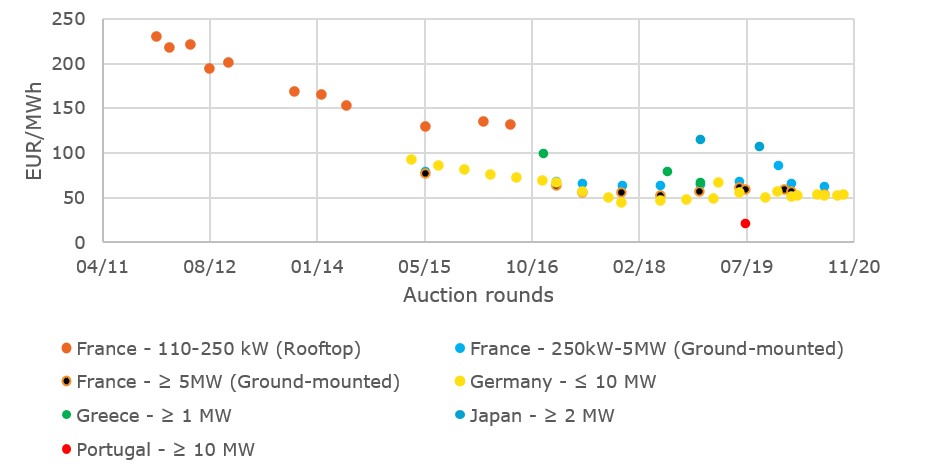

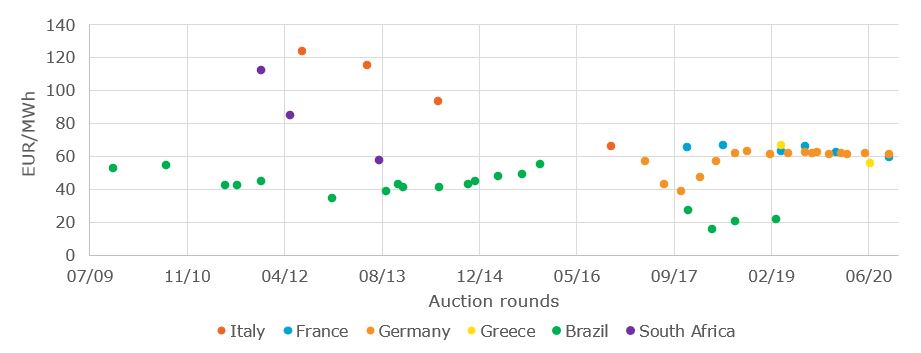

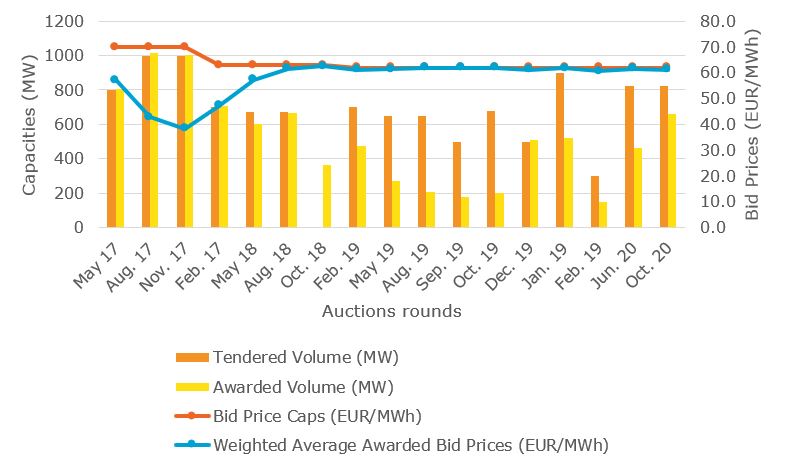

In 2017-2018, an estimated 111 GW of utility-scale renewable electricity (RES) was auctioned or announced. Solar PV and onshore wind stood for more than one-half and one-third of the total volume, respectively. In 2005, only six countries organised RES auctions against more than 100 in 2020. Thus, tendering procedures have become a must-have for States willing to secure their future electricity production from RES and participate in technology maturity development and cost competitiveness. Indeed, as illustrated in the graph below, the solar PV average bid prices significantly decreased from 2010 (figure 3). For wind onshore, the trend is also downwards (figure 4), but very recent auctions results in Germany showed that a low level of competition could stop driving down the awarded bid prices, fixing them near the bid caps (figure 5).

Nevertheless, the results prove the role played by the competitive nature of auctions to push RES technology prices and costs downwards over the past decade. A consensus is rising among policymakers to consider RES auctions as an efficient tool for the design of RES technology support policies as they help to determine the fair market prices of renewables. They also enable to avoid public-funded windfall profits for RES developers.

Figure 3: Weighted average awarded bid prices for solar PV for selected EU countries, 2010-2020

Source: Enerdata, RES Auctions Monitor 2020

Figure 4: Weighted average awarded bid prices for onshore wind for selected EU countries, 2010-2020

Source: Enerdata, RES Auctions Monitor 2020

Figure 5: Weighted average awarded bid prices for onshore wind for Germany, 2017-2020 and capacity tendered/awarded

Source: Enerdata, RES Auctions Monitor 2020

New record-breaking lowest price in recent solar PV auction in Portugal

Portugal recently hit the headlines in the booming renewable energy market of which medium term growth outlooks do not seem to be affected by the health crisis linked to the covid-19 outbreak. End of August 2020, the Portuguese government announced the results of the Portugal’s second solar PV auction with record-breaking low prices of €11.14/MWh (US$13.12/MWh). 670 MW was awarded to Hanwha QCELLS, Iberdrola, Enel, and Tag Energy, with most bids including solar and battery storage. The lowest bid record comes short after the previous one of US$13.50/MWh set in April 2020 by the Al Dhafra project in Abu Dhabi (United Arab Emirates) that already stood 25% lower than the lowest bid in the Portugal’s first solar PV auction held in August 2019, set at €14.76/MWh (US$15.95/MWh), already a record at that time.

"Subsidy-free” prices from recent RES auctions may raise concerns on RES project effective implementation

As seen in the previous sections, different public support mechanisms coexist to keep fostering RES investors and developers to gain RES market shares with relatively young technologies. But recent auctions years have experimented the emergence of “subsidy-free” or “zero-premium” winning projects, meaning the lowest awarded bid price was set at €0/MWh. As a case in point, in December 2017, the Dutch government awarded Chinook C.V, a limited partnership and a subsidiary company of Nuon/Vattenfall with the permit to construct and operate the offshore wind farm at Sites I and II of the Hollandse Kust (zuid) Wind Farm Zone thanks to a zero-premium bid. The new wind park should be ready in 2022, which will make it the first in the world to be constructed without subsidy (excluding grid connection cost that will be borne by the Dutch State and not by the project developer).

If the near “subsidy-free” trend in past auctions may be a signal for reaching RES technology maturity, it has not clearly been proved yet and the risk of possible strategic underbidding behaviour by auction participants does exist. Based on the latest RES auctions results, a very recent study from the Electrical Engineering Department of the Polytechnic University of Catalonia (July 2020)1computed the profitability metrics (i.e. projects’ Net Present Value - NPV and Internal Rate of Return - IRR) and performed sensitivity analysis to conclude that only very specific scenarios enable economically viable projects. Focusing on the Danish 2019 onshore wind and solar PV auctions, the sensitivity analysis showed that to reach the NPV break-even in the onshore wind case:

- either the weighted average cost of capital (WACC) must decrease by 59%

- or the investment cost by 37%

- or the average market price must increase by 3.6%/year

The PV case is unprofitable whatever the WACC may be, and either the investment cost must decrease by 60% or the average market price must increase by 6.8%/year for the NPV to break-even.

RES auction bids are a useful proxy for estimates of actual RES technology costs and revenues, but time and critical distance are still needed to properly assess their effectiveness.

From the profitability analysis above, we may wonder whether the design elements and the competitive pressure imposed by the auctions distorts expected revenues away from the actual costs of the RES projects. It might be the case if the auctions are perceived as “option to build” that can be realised only if projects are profitable2 or if auction participants bid below cost to prevent new entrants from competing and thus gaining market for long-term profits accepting initial short-term loss. However, a recent article from the scientific review Nature Energy (July 2020)3 harmonised the results of 41 past recent auctions on offshore wind in five European countries: Germany, Belgium, the United Kingdom, the Netherlands, and Denmark to show that:

- Offshore wind farm costs are decreasing in a uniform manner across Europe, having recently dropped below the €50/MWh threshold, standing with the lower end of the LCOEs estimates of fossil fuel generators4.

- In spite of significant differences in auction design, the expected harmonised lifetime revenues of wind parks are even across countries. Policymakers have therefore designed auctions that give a fair view of the actual costs of developing offshore wind parks, and that the specific auction design is not particularly influential on the outcome.

As RES auctions are still an emerging tool, time and further experience in RES auction design are needed to properly assess their success in terms of effectiveness and profitability.

Key Take-Aways

- Increase in installed capacity in renewable electricity (RES) goes with technology maturity development and government support (e.g. subsidy schemes)

- RES auctions are market-based instruments used more and more by policymakers to design the RES support schemes.

- Successive recent auctions held keep breaking records in low bid prices, especially for solar PV technology.

- Various forms of public-funded remunerations coexist to subsidy the development of RES projects and achieve national RES capacity targets.

- The latest outcomes of RES auctions, notably in offshore wind opened a new era of “subsidy-free” projects.

- Low winning bid levels on the latest RES auction results cast doubts on the effective realisation of future RES projects as profitability may be reached only in specific scenarios.

- Strategic underbidding may be led by auction bidders to gain long-term market shares at the expense of short-term loss and thus leading distorting RES projects’ expected revenues from actual costs.

- The convergence and homogeneity of bid results in the past offshore wind auctions in Europe prove that policymakers give a fair view of the actual costs of developing projects, and that the specific auction design is not particularly influential on the outcome.

Notes:

1. Helena Martín, Sergio Coronas, Àlex Alonso, Jordi de la Hoz and José Matas, Renewable Energy Auction Prices: Near Subsidy-Free? Polytechnic University of Catalonia, Spain, 2020

2. Felix Müsgens, Iegor Riepin, Is Offshore already competitive? Analyzing German Offshore Wind Auctions, Institute of Electrical and Electronics Engineers, IEEE, Germany, 2018

3. Malte Jansen, Iain Staffell, Lena Kitzing, Sylvain Quoilin, Edwin Wiggelinkhuizen, Bernard Bulder, Iegor Riepin and Felix Müsgens, Offshore wind competitiveness in mature markets without subsidy, Nature Energy, 2020

4. Lazard’s Levelized Cost of Storage Analysis—v.12.0. Lazard, 2018.