See also

Market Research / Studies

Granular and exclusive insight to address the most pressing business and strategic issues.

A new pathway to decarbonising the transport sector

Get this Executive Brief in PDF format (Free)

This executive brief reviews the status of retrofitting existing heavy transportation vehicles with hydrogen technology allowing the reduction of carbon emissions to net-zero. It includes various aspects: the market dynamics, the key stakeholders and regulations, and potential support schemes.

Introduction

Growing concerns about the energy transition and the need to decarbonise the transport sector have driven the sector to adopt clean mobility solutions. Hydrogen vehicles, powered by hydrogen fuel cells and hydrogen combustion engines, are emerging as an alternative to fossil fuel combustion engines powered vehicles. Although hydrogen-powered vehicles are still in the early stages of deployment compared to the battery‑electric counterpart, their future could be promising if green hydrogen (H2) prices decline as projected. A price of €5 to €7 per kg of H2 is considered as a critical threshold1. This analysis will focus on the use cases of long-haul heavy trucks, buses, and vans as examples of the potential for hydrogen retrofitting for mobility decarbonisation.

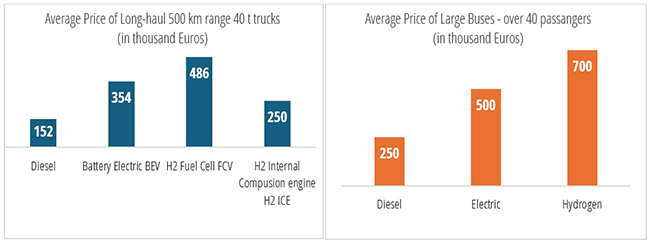

Beside the current hydrogen price which ranges from €12 to €20 per kg at the pump across Europe, the upfront cost of new hydrogen trucks and buses is a critical barrier to adoption. Hydrogen fuel cell FCV long-haul 40 tons trucks with a range of around 500 km are 3 times more expensive (see Figure 1 below) than diesel counterparts and around 50% more expensive than Battery Electric Vehicles (BEV) ones. Similarly, hydrogen buses are about 40% more expensive than electric buses and around 3 times more expensive than diesel buses.

As such the evolution of retrofitting old trucks and buses could potentially be a competitive alternative to new vehicles. Additionally, retrofitting provides extra environmental and sustainability advantages. It extends the service life of the existing fleet, reducing both waste and carbon emissions from the manufacturing of new vehicles. From an energy transition perspective, it is an efficient solution to quickly converting the large fleet of polluting diesel vehicles, which would take decades to completely replace with new clean vehicles at the end of their service life.

Figure 1 - Average price of Medium & Heavy-Duty Vehicles per propulsion energy

Sources: International Council for Clean Transportation with Enerdata analysis

While retrofitted vehicles incorporate the same powertrain and supportive components such as controls, safety, and tanks which are subjected to the same market prices, they benefit from using the same vehicle body and accessories, substantially reducing the overall cost. Additionally, in many European countries retrofitted vehicles are eligible for subsidies and bonuses for clean vehicles (see Table 1 - Hydrogen retrofit support schemes over a sample of countries/regions).

Relevance of the Retrofitting – need and opportunity

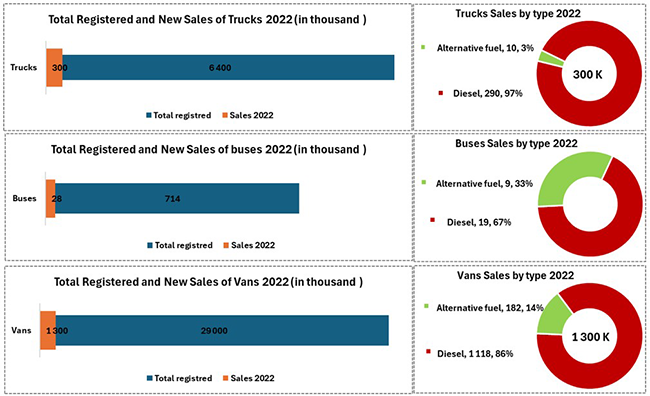

Taking the case of Europe sheds light on the potential of retrofitting as a plausible and economic solution. The current registered fleets of trucks (6.4 million), buses (714 thousand) and vans (29 million)2, that are predominantly fossil-fuels powered, are extremely large and would take decades to replace at the current rate of sales of new vehicles. Additionally, the percentage of sales of new trucks, buses and vans powered by alternative fuels only represents a small fraction of total sales (see Figure 2 below) this could hardly make a dent in the transformation of this important sector. Worldwide, trucks and buses are responsible for more than 35% of direct CO2 emissions from road transport despite representing only 8% of the fleet number3. As such, retrofitting stands out as an eligible candidate to decarbonisation of the road transport sector with clear economic, technical and environmental advantages4.

Figure 2 - Total Registered and Sales of Trucks, Buses, and Vans by type in Europe as of 2022

Source: The European Automobile Manufacturers’ Association ACEA (Trucks, Buses & Vans)

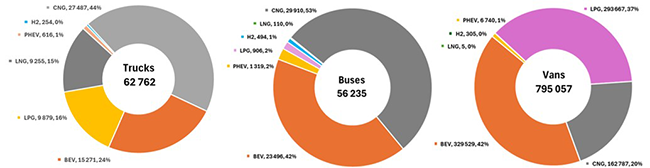

Currently in the Europe, the total number of registered alternative fuels powered trucks, buses and vans stands at 62 thousand, 56 thousand, and 795 thousand respectively. Hydrogen powered vehicles of the 3 categories represent 1% or less of the total registered vehicles (see Figure 3 below). Hydrogen vehicles are clearly far from large scale deployment and would continue to suffer the “egg and chicken” dilemma, unless initiatives such as retrofit as incentivised.

Figure 3 - Total number of registered Alternative fuel Trucks and Buses

in Continental Europe as of Q1 2024

Source: European Alternative Fuels Observatory

Market Dynamics & Technology providers

Legacy established manufacturers like Mercedes, Volvo, Scania, and Iveco and others were joined by a wave of new entrants like Nikola, Hyzen, BYD offering new hydrogen buses and trucks. Many startups and innovative companies offer tailored solutions to retrofit buses, trucks or vans with hydrogen powertrain, whether it is a fuel cell + battery or internal combustion engine. France is one of the countries with a vibrant retrofitting market. Several innovative companies and startup emerged capitalising on the market opportunity, public support and interest, especially from local authorities, to convert existing fleet to hydrogen powered vehicles2. The following list provides a snapshot of key innovative companies that dominate the retrofit market and mostly developed their own in-house technologies:

ULEMCo – The UK

ULEMCo has developed a unique hydrogen dual-fuel approach called H2ICED®, which allows hydrogen to be mixed with diesel in conventional engines, displacing 30-70% of diesel consumption. They are collaborating with Oxfordshire County Council for fleet conversion where a contract was signed as part of a £10 million plan to renew their operational fleet5,6.

Clean Logistics - Germany

The medium-sized joint venture Clean Logistics was founded in 2019 by the investment company Höpen, Hary Logistics and Proton Motors to advance alternative drives for the logistics industry7. They convert diesel trucks, especially DAF XF 106 and Mercedes Actros MP4 tractor-trailers with over 100 retrofitted trucks till date and claims an extraordinary pipeline of 6 000 vehicles by 2027 (see next chapter on this company’s situation).

Quantron – USA/Germany

Quantron offer Q-Retrofit services, where they convert diesel vehicles ranging from 3.5 up to 49 tonnes, as well as medium and large buses. Under agreement with Ford Otosan, they retrofit Ford F-Max trucks with fuel cell powertrains. Quantron offers a "Quantron‑as‑a‑Service" platform in Europe, providing zero-emission transport solutions on a per‑kilometre basis8.

Arcola Energy – The UK

Now acquired by Ballard, they specialise in integrating hydrogen fuel cell technology into heavy-duty vehicles and other transport applications like Buses and Trucks. They convert fleets of buses and refuse vehicles to run on hydrogen power at their Enfield site. They have Retrofitted buses for Optare, Wrightbus, Arrival, and others. They introduced the A‑Drive platform, a scalable production-ready FC powertrain for heavy‑duty vehicles9.

GreenGT - Switzerland

GreenGT began working on retrofitting since 2015 with the design of a prototype vehicle, the Renault Trucks Maxity, for the French post office. The company was established through a collaboration between Symbio and Renault Trucks. In 2021, heavy vehicle development contracts were signed with 2 mass retail entities: Carrefour in France (44 tons trucks) and Migros in Switzerland (40 tons trucks).

GCK Mobility - France

GCK specialises in converting a wide range of heavy vehicles, including road vehicles (coaches, buses, vans, trucks), off-road equipment and marine yachts. They have partnered with Keolis to trial the conversion of a diesel coach (IVECO Crossway) to hydrogen. In February 2024, they reached 2 major milestones: they won a significant contract with Auvergne-Rhône-Alpes region for the hydrogen retrofit of 50 coaches10, and they received road homologation in France for their retrofitted vehicles11.

Hyliko - France

Hyliko rent or lease both new and retrofitted H2 vehicles. Among their offerings is the Renault Trucks T chassis with a hydrogen fuel cell electric powertrain, developed by the same group’s sister company, GreenGT. Hyliko target to operate 3,500 heavy trucks by 203012, both new and retrofitted. As of October 2024, Hyliko operate 3 retrofitted trucks for material transportation.

SAFRA - France

Safra developed the H2-PACK® retrofit kit, which converts diesel coaches into hydrogen-electric powertrains. The kit includes a 350 kW DANA electric motor, a 100 kW Plastic Omnium fuel cell, and 6 hydrogen tanks storing 35 kg of hydrogen. In April 2024, the company started the deployment of 2 out of 15 intercity coaches (Mercedes Intouro) for the Occitanie region in France, the 13 remaining ones are to be delivered by end of 202413.

SYMBIO - France

Symbio is a joint venture between Faurecia and Michelin. It designs, produces, and markets fuel cell systems for light and commercial vehicles, buses and trucks. Its hydrogen vehicles travelled more than three million kilometres. It targets production of 200,000 StackPacks Fuel Cell systems per year in 2030 (NB: at least one per vehicle, depending on power needs)14.

EHM ICE H2 Motor – France

This startup of around 20 people, created in May 2022, propose a large Hydrogen Internal Combustion Engine (ICE) of 300 HP targeting buses and trucks. As of October 2024, the engine is still in development and testing, it hasn’t reached yet certification stage. Industry insiders estimate that H2 ICE engine won’t be on the market until 2027 or 2028. Among others, they target deployment in retrofitted trucks, buses and potentially marine applications. The expected price ranges from €100k to €150k according to economics of the potential demand and manufacturing.

Market Evolution

Since 2017, several experimental projects have been developed, often led by integrators, prototype manufacturers or retrofit players with quite limited production capacities. These early players include ESORO, PVI, VDL, E-Trucks, Gaussin or GreenGT for example. They provided significant R&D effort paving the way for technology commercialisation. A specific business case is the French Chéreau, specialised in the manufacture of chassis dedicated to refrigerated trailers (holds 23% of the European market). It has developed a complete solution for powering refrigerated semi-trailers with H2, for the refrigeration solution, a market also targeted by Bosch 14.

Innovative companies are formulating partnerships across the hydrogen mobility value chain. Several of these partnerships are targeting converting diesel vehicles to hydrogen propulsion, including start-ups, as seen in previous section. But established manufacturers such as Scania are also exploring hydrogen applications, with projects like the FresH2 initiative testing fuel cell-powered refrigeration units for trailers 14.

In Europe, there are several publicly funded projects like H2Engine and H2Haul that support technical development and deployment of hydrogen FC powertrain and ICE targeting retrofitting existing fleets. Industrial coalitions like Coalition Rétrofit H2 in France and partnerships also exist. Aside from these pilot projects, the market demand side is potentially concentrated around local authorities, industrials and other captive fleets where the number of vehicles operated by a single entity is large and could benefit from on-site refuelling infrastructure along with the economies of scale. Additionally, local authorities can leverage grants and favourable financing from national authorities and the European commission to cover the higher cost of these hydrogen vehicles. It's worth mentioning the existence of wide range of new hydrogen buses and trucks transactions supported by grants like initiatives in France, Germany and Switzerland. These initiatives should be expanded to include hydrogen retrofitted vehicles.

The road is not always rosy

The French startup E-Néo was a pioneer in hydrogen retrofit, converting diesel trucks to hydrogen. It was recognised by the French Ministry of Transport working on various hydrogen retrofit projects, including converting trucks and even a tractor to hydrogen. But the company declared bankruptcy in 2024, and its founder announced cease of operations stating funding problems and challenges with homologations and component supplies. Later on, the Vensys Group announced the acquisition of the company assets and continuation of its retrofitting business15,16.

There are also difficulties on the German site, the stock listed company Clean Logistics SE was out cash late 2022, funders left the company, and it was declared insolvent in February 202317, leaving 70 employees out of a job. Quantron also faced problems and was declared insolvent in October 202418.

On the demand side, there are clients, like the Montpellier metropolis, that dropped their plans to purchase (new) hydrogen buses citing high cost of operation and favoured eventually electric buses19.

This demonstrates that the retrofit activity demands long-term efforts and the associated cash to live up to first homologations and orders. It is also faced with the difficulties of the hydrogen mobility today. Still, several companies remain in the game and keep on pushing this alternative to brand new vehicles.

Support schemes and Regulations

Support schemes

Subsidies have played a critical role in triggering the electric car market and are expected to be equally important for the retrofit market. Most European countries, provide subsidies for scrapping an old fossil vehicle and purchasing of a new low-emission one. Bonuses – for electric cars - reached up to €12,000 in France and Romania, €9,000 in Germany, and €6,000 in Poland. Based on avoided carbon emissions, our analysis suggests that e-retrofitted vehicles could be entitled to an additional €1,500 subsidy in France and €2,700 in Germany relative to standard EVs. If it proves to be a viable solution at scale, a possible scenario will involve a gradual shift of additional subsidies from old car scrapping and new EV purchase to e-retrofit20.

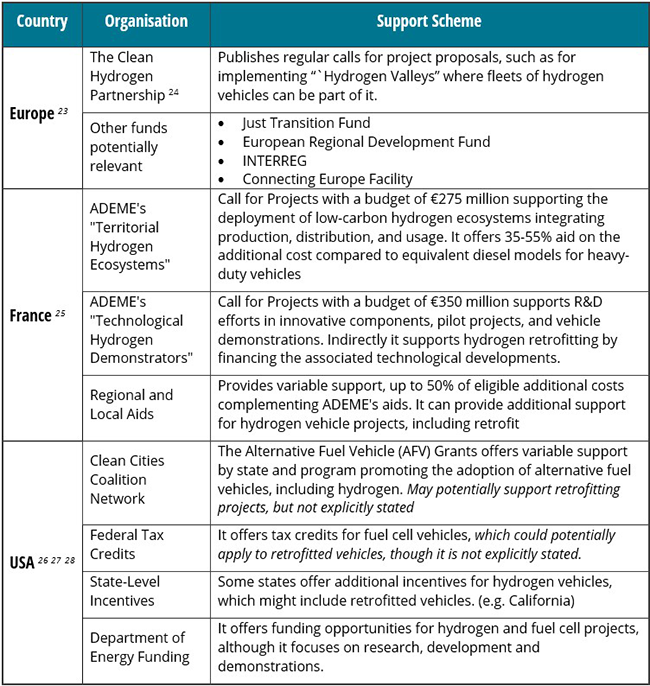

At European Union level, apart from local schemes, there are several support schemes for the hydrogen sector in general that could be applicable to retrofitting. However, they focus more on infrastructure and technological development rather than direct support for vehicle retrofitting. As European Member State, France has several generous support mechanisms that triggered a vibrant ecosystem along the whole value chain and encouraged many startups and innovations in this domain. These schemes range from innovation, technology to ecological grants that complement one another. However, retrofitted vehicles currently face limitations in accessing some of these aids, highlighting a potential area for policy improvement to support the hydrogen retrofitting industry. There could be also 2 potential mechanisms that are not currently applicable to retrofit (but could be in the future): Super-Depreciation21 & Ecological Bonus22.

The USA disposes several support mechanisms that are or could be extended to retrofit. These mechanisms range from grants, innovation funds to tax credits and differ from state to another.

In China, retrofitted vehicles are not eligible for federal, nor regional subsidies of hydrogen powered vehicles. While Europe enjoys vibrant retrofitting market, in China we couldn’t identify any buses or trucks retrofitting projects nor initiatives. Based on feedback from key Chinese market players, federal and state subsidies are only available for the purchase of new vehicles while retrofitted vehicles are not eligible for these support schemes. As such, operators of fleets don’t see an economic advantage for retrofitting their vehicles. Europe, on the contrary, offers innovation and deployment subsides to retrofitting as outlined in previous sections.

Table 1: Hydrogen retrofit support schemes over a sample of countries/regions

Source: Enerdata

Hydrogen retrofit vs. regulations

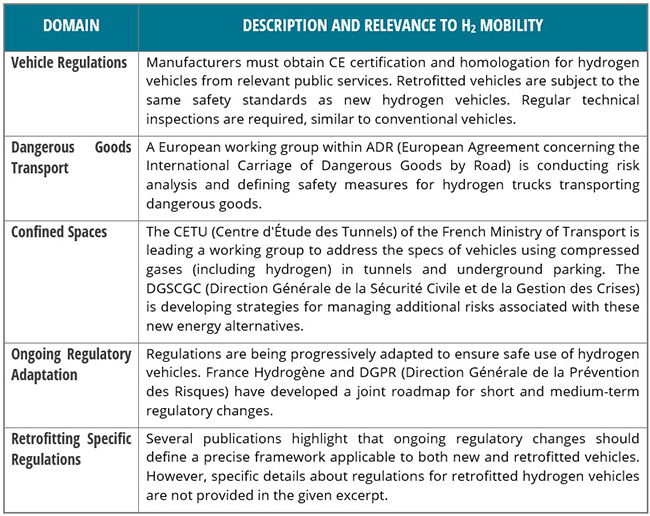

Vehicles, as an industrial commodity are subjected to a wide range of regulations and certification standards to ensure quality, security and safe operation. These eventually lead to the full vehicle homologation., i.e. the official authorization, approval or validation process that confirms the conformity of a product, service, or act to specific standards or norms.

Hydrogen retrofitted vehicles must obtain CE certifications, in addition to complying with rules of “dangerous goods transport” given that hydrogen poses some safety hazards if not properly treated. There is ongoing research on adapting regulations and integrating relevant modifications to address the specificities of hydrogen vehicles. Retrofitted hydrogen vehicles are not specifically set apart in existing regulations; however, this may be a transitional stage until they are clearly defined by competent authorities. The following Table 2 summarises the general regulations applicable to hydrogen mobility; it is important to underline that country or regional specificities might exist. The International Transport Forum has compiled the existing technical regulations and standards for clean trucks and buses29. The EU has issued directives and modified old ones tackling the carbon emissions of transport and promoting clean energy road transport vehicles30,31.

Table 2 - some applicable regulations and certification to hydrogen mobility & retrofit

Source: France Hydrogen

Conclusion

Hydrogen-powered commercial vehicles, including trucks, buses, and vans, currently lag behind their electric counterparts in terms of sales and adoption. While battery electric vehicles (BEVs) benefit from a more mature technology and established infrastructure, hydrogen fuel cell electric vehicles (FCEVs) offer significant advantages that have yet to be fully realised, particularly for heavy-duty and long-distance applications. The hydrogen retrofit market is almost non-existent outside Europe. Many European countries have extended subsidy eligibility to hydrogen retrofit and encouraged local authorities to retrofit their fleets. While many countries offer subsidies specific to hydrogen mobility or under a broader clean mobility umbrella, retrofit has not been specifically stipulated as an eligible applicant. China, which holds a record 90% of the world’s zero-emission buses and trucks, doesn’t include retrofit in its various subsidies’ schemes; only new vehicles are eligible to subsidies.

Despite the slow growth in 2023, major global fuel cell manufacturers such as Ballard, SHPT, REFIRE, and EKPO have made substantial investments in expanding their production capacity. However, current sales represent only a fraction of this capacity, leading to underutilized assets and financial losses.

Retrofitting existing vehicles with hydrogen fuel cell technology is environmentally friendly and practical pathway to accelerate hydrogen mobility adoption. To overcome regulatory challenges, certification issues, and secure funding for retrofitting projects, collaboration between technology suppliers, policymakers, and fleet operators is crucial. Clean mobility subsidy schemes and green financing programs must clearly identify hydrogen retrofit as an eligible mobility decarbonization pathway.

On the manufacturing front, there is a pressing need for partnerships between powertrain developers, established automotive manufacturers and innovative startups. While startups may lack the industrial infrastructure to handle large-scale retrofitting, traditional automotive companies can leverage their existing resources to incorporate innovative hydrogen technologies and retrofit their vehicles on a broader scale.

By addressing these challenges and fostering collaboration across the industry, the hydrogen mobility sector can capitalize on its potential advantages and accelerate adoption, particularly in the heavy-duty and long-haul transportation segments.

KEY TAKEAWAYS

- Hydrogen-powered commercial vehicles lag Battery Electric Vehicles (BEV) in sales and adoption, which have more mature technology and infrastructure

- Fuel-Cell EV (FCEV) has untapped potential, especially for heavy-duty and long-distance use.

- The hydrogen retrofit market is mainly happening in Europe, where some countries have extended subsidies to retrofits.

- Retrofitting vehicles with hydrogen fuel cells is environmentally friendly but faces regulatory and funding challenges.

- Collaboration between technology suppliers, policymakers, and fleet operators is essential to overcome these challenges.

- Clean mobility subsidies and green financing need to include hydrogen retrofits as eligible pathways.

Notes:

- Feedback gathered by Enerdata from a logistics company which piloted hydrogen truck deployment.

- The European Automobile Manufacturers’ Association ACEA (Trucks, Buses & Vans)

- Trucks & buses - IEA

- E-retrofit_report.pdf (te-cdn.ams3.digitaloceanspaces.com)

- ULEMCo – Hydrogen Extended Range Powertrain (HyER Power) - Advanced Propulsion Centre (apcuk.co.uk)

- ULEMCo awarded contract for fleet Hydrogen Conversion - The Procurement Partnership (tppl.co.uk)

- Clean Logistics Hydrogen Truck (bayern-innovativ.de)

- Quantron AG: 360° zero emission product & solution ecosystem

- Arcola Energy introduces production-ready hydrogen fuel cell powertrain - (essmag.co.uk)

- gck.co - actualite-green-corp-konnection/une-premiere-en-europe-gck-decroche-un-marche-de-50-autocars-retrofites-pour-la-region-auvergne-rhone-alpes (in french)

- gck.co - news-homologation

- Pour Hyliko, l'hydrogène c'est maintenant (journaldupoidslourd.com)

- safra.fr-frances-first-fleet-of-hydrogen-powered-buses-retrofitted

- France-Hydrogene-Mobilite_Livre-blanc-Camion-H2_web-final.pdf

- Retrofit : e-Neo jette l'éponge (in French)

- Rétrofit hydrogène : e-Neo est de retour (in French)

- kreiszeitung-wochenblatt - wirtschaft-clean-logistics-se-insolvent-70-arbeitsplaetze-in-gefahr_a273480 (in German)

- quantron.netp - content-uploads/2024/11/EN-QUANTRON-explores-opportunities-to-successfully-continue-business-operations

- French city drops order for 51 hydrogen buses

- E-retrofit_report.pdf

- A 40-60% exceptional deduction rate applicable to zero and low-emission vehicles over 3.5 tons Gross Vehicle Weight Rating (GVWR), not currently applicable to retrofit but could be in the future.

- Offers a €50,000 aid for the purchase of clean heavy-duty vehicles, not currently applicable for retrofit but could be in the future.

- JIVE Best Practice Report 3 / JIVE 2 Best Practice Report 2

- clean-hydrogen.europa.eu - apply-funding_en

- France-Hydrogene-Mobilite_Livre-blanc-Camion-H2_web-final.pdf

- afdc.energy.gov - laws/10513

- cleanvehiclerebate.org - en

- energy.gov-eere-fuelcells-hydrogen-and-fuel-cell-technologies-office

- regulations-standards-clean-trucks-buses_0.pdf (itf-oecd.org)

- Reducing CO₂ emissions from heavy-duty vehicles - European Commission (europa.eu)

- Clean Vehicles Directive - European Commission (europa.eu)