A growing technology to face the European energy crisis

Get this executive brief in pdf format

More than ever, Europe needs to reduce the energy consumption of its buildings and its dependency on fossil fuels (e.g., gas, fuel oil…). More and more stringent regulations for new buildings (e.g., RE2020 in France, Buildings Energy Act in Germany…) and existing ones, combined with rising gas prices (enhanced by the current crisis) leave two key heating options: biomass and heat pumps.

Moreover, the need for cooling has never been so high (indeed, 2022 is probably the coolest summer of the coming years). Despite many advantages, biomass cannot be used everywhere. Heat pumps are the only option that can answer both of those needs (heating and cooling) and are expected to become the main heating and cooling source in new buildings.

While air-based ones are the most used heat pump systems (83% of the EU sales in 20211) thanks to their (relatively) low price and easiness of installation, they have flaws (efficiency, local neighbourhoods heating, visual impact) that hinder their growth.

Geothermal heat pumps are an efficient alternative to air ones and conventional solutions

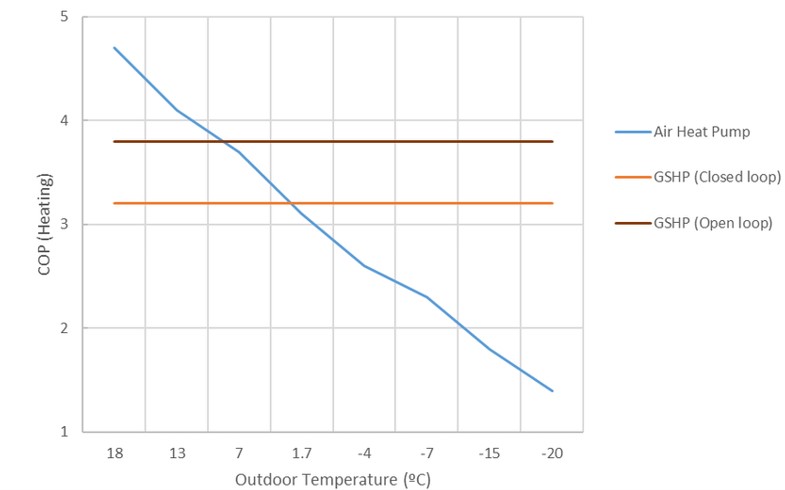

Geothermal heat pumps offer even higher efficiency by using the thermal energy contained in the ground (water or earth) as an inter-seasonal or daily buffer (See Figure 1). Heating with a geothermal heat pump at depths of less than 500 meters and with ground temperature under 100 °C is classified as shallow geothermal energy2.

Figure 1: Heat pumps technology efficiency comparison

Source: Ramos-Escudero et al., 2020

This energy is not the most well-known solution for decarbonisation in Europe (except in a few countries, such as Sweden), despite its many qualities. With COP3s up to 5, geothermal energy can provide energy savings of up to 70% compared to a conventional heating or cooling solution.

Available geothermal heat pumps technologies

Two main types are being used:

The geothermal energy on aquifers works by injection and later re-production of hot water in aquifers. The aquifers can be both unconsolidated sand units, porous rocks like sandstones or limestone, or e.g., fractured rock formations. The main advantage is that it does not require a large drilling area, but on the contrary, you need to have an aquifer below your building.

The geothermal energy on pipes or brine water heat pump which the natural heat capacity store in a large volume of underground soil or rock to store thermal energy. The principle of this technology is to heat up the subsurface and cool it down again by circulating fluids in plastic u-tube pipes. Its tubes can be installed in different ways. They can be subdivided into 3 main categories

- Boreholes

The principle is to install in several closely spaced so-called closed loop boreholes or Borehole Heat Exchangers (BHE) and complete with a sealing grout. The distance between the boreholes is typically in the range of 2-5 m and the depth is normally limited to boreholes of approx. 20-200 m. Its systems are therefore mainly used in collective housing, the tertiary sector, and public buildings.

- Horizontal

Similar concept, but the tubes are distributed horizontally at a depth between 40 cm and 1 meter. It is less expensive to install than boreholes because of lower drilling costs. But they require larger areas. It is therefore mainly used in individual houses.

- Other innovative systems like geothermal baskets or walls are less common and use a mix of the physical properties of both borehole and horizontal geothermal energy.

Other technologies are available, such as PTES or MTES. But these solutions are not well-developed and are specific to certain geographical characteristics.

Geothermal heat pumps can be a cheaper alternative to air/air heat pumps

Among those geothermal possibilities, the least-cost technology choice heavily depends on local parameters (e.g., available land, geology, local climate…). For instance, drilling costs for boreholes can vary by a factor of 1 to 10 depending on the soil4.

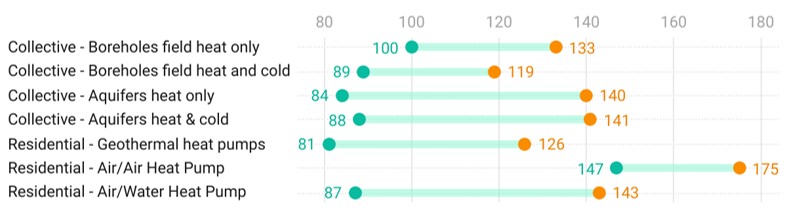

Those solutions often offer a lower LCOE, but always for a higher CAPEX (compared to air heat pumps or gas installations). Installation costs can be up to 3 times higher than a classic gas solution, while the LCOE for a surface geothermal project varied (in 2019) 81 to from 141 €/MWh (see graph below).

Figure 2: LCOE range of surface geothermal projects in France

Source: ADEME, 2019, Chart by Enerdata

Collective geothermal projects have known a strong recent development

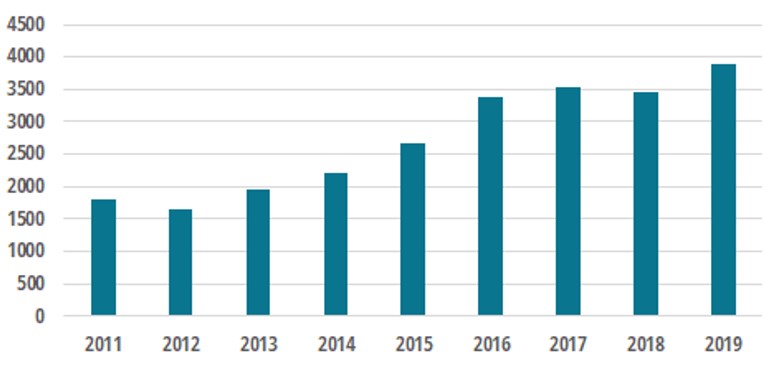

Indeed, the market of these technologies is in strong growth. Geothermal heat pump sales reached record growth levels of 73% in France, 59% in Austria, 35% in Belgium, and 10% in Germany.

Figure 4: Annual sales of renewable heat pumps in thousands in EU 28

Source: Odyssee Database, Enerdata

In terms of overall geothermal heat pumps capacity installed, the market is dominated by Germany and Sweden which represent half the installed geothermal heat pumps in Europe, and nearly half the annual sales. Indeed, approximately 240,000 and 230,000 geothermal heat pumps were sold in 2021 in Germany and Sweden, respectively. Those sales mostly concern residential and tertiary customers.

We can also note, that more and more of these sales are for collective buildings. In 2021, in Europe 14, new geothermal district heating and cooling systems were commissioned. France and the Netherlands commissioned 3 each. The remaining new capacity was in Germany, Finland, Poland, and Switzerland. Notably, the first geothermal district cooling project was commissioned in Finland. (Source: EGEC market report 2021)

The high installation costs of collective geothermal projects and the lack of awareness of most people are the main obstacles to their development. For instance, very little emphasis is placed on the ability of geothermal systems to adapt their operation to buildings’ energy needs changes. These changes can be due to climate change or renovations.

Mature players are being challenged by innovative newcomers

Different kinds of companies are involved in geothermal projects from drilling companies for boreholes systems (Rototec in Finland or DrillHeat in France) to EPC (ENGIE or Sweco) to heat pump manufacturers (Viessmann or NIBE). Some of those companies have activities in several European countries, however, the vast majority of them are small and mid-size national players. It is also noticeable that Nordic countries (Norway, Finland, and Sweden) host the most mature players.

Some of them have developed innovative solutions to help the development of this market such as ADVEN, Energy machines, Accenta, or Geosophy. They have in common to be present all along the value chain of geothermal projects and to offer energy services. They are also using digital solutions to optimise their cost. But those companies also have their own particularities:

- Accenta (FR) for instance is based on an ESCO model and claims to provide decarbonisation systems for buildings (also sales biomass and air/air HP solutions).

- Energy machines (DK) provides integrated systems that combine heating, cooling, ventilation, and solar & wind power.

- Geosophy (FR) has developed an automated solution to carry out pre-feasibility studies quickly and efficiently.

KEY TAKEAWAYS: Surface geothermal energy is a part of the solution to many of our current problems

As we have seen, surface geothermal energy has many advantages, but is not applicable all the time. Its specificity (local conditions, high CAPEX) makes it relevant for designated projects, in particular for new constructions or complete renovations. In order to optimise these projects, different technologies are available, such as geothermal energy on aquifers or geothermal energy on pipes.

These technologies are currently more developed in countries like Sweden and Germany. Their development is expected to continue, carried by the strong development of air heat-pump, but at a slower pace. Projects are currently multiplying all over Europe and will continue to do so in the coming years.

Notes:

- EHPA, Heat Pump in Figures: 2021 EU Market, https://www.ehpa.org/fileadmin/extension/news/2021_heat_pump_market_dat…

- Deep geothermal energy (which consist of extracting heat from the ground at >1000m depth) is not included in this analysis as it is mostly used for electricity production on very specific locations. 2 COP is for Coefficients of performance and is defined as the relationship between the power (kW) that is drawn out of the heat pump as cooling or heat, and the power (kW) that is supplied to the compressor.

- Coefficient of Performance: ratio of useful heating or cooling provided to work (energy) required

- Source: Enerdata interviews of drilling companies

ABOUT THE AUTHOR

Corentin BOILLET

Junior Analyst at Enerdata

Corentin is a Junior Energy Analyst within the Clean Tech team of Enerdata.

Before Enerdata, he has been working on thermal energy management and energy efficiency of a co-generation plant in the biomass industry.

Within Enerdata, Corentin has made market study about different subjects like batteries, hybrid systems, electricity grid flexibility, and geothermal energy. He holds a M.Sc. in energy management and marketing degree from Grenoble Business School (GEM), and a degree in Energy, Building and Environment Engineering from Polytech Chambéry.