Achieving EU climate ambitions amidst the current market and political turmoil.

Get this Executive Brief in PDF format (Free)

In early July 2025, the European Commission (EC) proposed an amendment to the EU Climate Law, setting a new EU climate target of a 90% reduction in net greenhouse gas emissions by 2040, compared to 1990 levels. The EC proposal emphasised that all current and future net-zero energy technologies – such as renewables, nuclear, geothermal, hydro energy, CCS, CCU and carbon removals – will be necessary to achieve the 2040 target, alongside energy efficiency following the “energy efficiency first” principle. Furthermore, the Commission is considering including a role for “high-quality” international credits under Article 6 of the Paris Agreement for a maximum of 3% of emissions reduction from 2036 -meaning a minimum of 87% reduction compared to 1990 achieved domestically in the EU.

The new proposal builds on the EU's existing legally binding goal of reducing net GHG emissions by at least 55% by 2030, with a view to reaching a decarbonised European economy by 2050. In 2023, net GHG emissions were already 37% below 1990 levels, and the EC’s assessment of Member States’ NECPs published in May 2025, shows that the EU is on-track to reduce GHG emissions by around 54% by 2030, provided Member States fully implement existing and planned national measures and EU policies.

However, recent months have been marked by political and economic developments that raise questions about the EU’s ability to meet its commitments. After outlining these uncertainties, we will focus on the EU’s response to stay on-track.

2024 - A green economy slowdown?

The year 2024 was marked by a slowdown in the development of key decarbonisation solutions, suggesting that the market reality may not be fully aligned with the EU’s ambitions, and raising questions about the credibility of certain targets and plans. As presented below, notable indicators of this trend include the uptake of EVs and the sales of heat pump, both of which slowed in 2024.

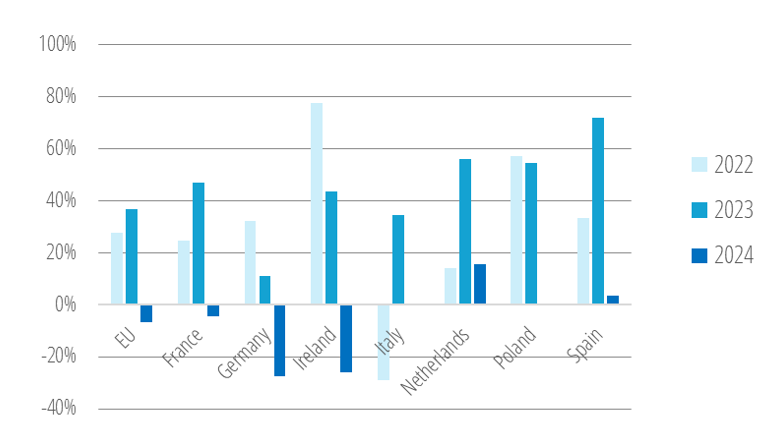

Electric vehicles (EVs) are one of the key levers expected for EU decarbonisation. Supported by increasing decarbonisation of the power mix, their development is crucial to achieving the goal of zero emissions from new cars and vans by 2035. The graph below illustrates the annual growth in EV sales over the last three years across the EU and several Member States.

EV sales fell by 6% in 2024 in the EU, compared to a strong increase in 2022 (+28%) and 2023 (+37%). All Member States recorded a slowdown in 2024 compared to 2023, but the impact may differ. Germany, which accounted for one third of EU EV sales in 2023, is the main country were EV sales fell in 2024, with a 27% decrease, i.e. almost 150,000 fewer vehicles sold. The second locomotive in the EU EV sales – France, with about 20% of the EU market – saw a 6% decrease in 2024 after an almost 50% increase in 2023.

In other countries, such as Italy or Poland, EV sales remained constant in 2024, while they saw a 16% growth in the Netherlands. Nevertheless, this is far below 2023 levels, when sales had progressed by about 35% to 55% in these countries.

This picture results from many factors. Shifts in national EV policies, e.g. reduction or ending of dedicated subsidies, have reduced the incentive for consumers to buy EVs. Germany, notably, ended EV purchase subsidies in the end of 2023. In addition, a part of consumers is still concerned about the reliability of EVs, notably EV range and charging infrastructure, and sometimes preferred to choose hybrid vehicles. The purchasing power of consumers has also declined, partly due to the rise in energy prices in recent years.

Figure 1: EV sales, annual growth

Source: Enerdata - EnerFuture, Granular Energy Demand Forecast module

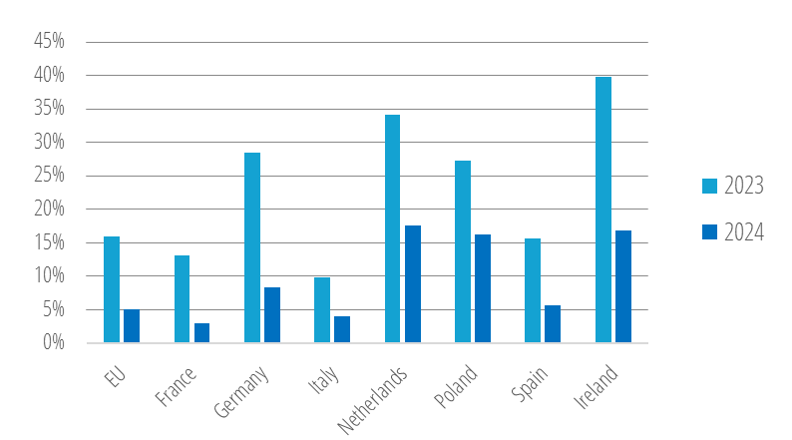

Furthermore, the uptake of heat pumps is also a key indicator for monitoring decarbonisation trends. By replacing old boilers, typically fuelled by fossil gas, heat pumps reduce household CO2 emissions and deliver significant energy efficiency gains, resulting in lower energy consumption for the same level of service.

In 2024, the number of heat pumps installed in households increased by only 5% in the EU, while it was 18%/year on average over 2021-2023. This trend was observed across all Member States. At the EU level, around 10% of dwellings were equipped with heat pumps in 2024, but this masks significant regional disparities: some Member States, such as France and Italy, lead the market, with approximately 15% of their dwellings equipped, while other countries, including Germany and Poland, do not exceed 5%.

The heat pump industry is facing several challenges. Supply chain issues slowed installations, notably due to labour shortages. In addition, even if a heat pump is often profitable compared to a traditional gas boiler over its entire life cycle, households face high upfront costs that they cannot always manage.

Figure 2: Penetration of heat pumps in households, annual growth

Source: Enerdata, Granular Energy Demand Forecast

Overall, 2024 saw a slowdown on some key decarbonisation markets, with a weaker than expected development of green technologies. This leaves one wondering about their ability to rebound in 2025 and beyond to remain on-track with the EU objectives. However, the market dimension is not the only area raising uncertainties.

A new balance of power in the European Parliament

The 2040 Climate Target proposal has to be submitted to the European Parliament and the Council for discussion and adoption. The vote is initially planned for 18th of September.

Yet, the process could take much longer than expected. Indeed, on 8th of July, the far-right Patriots for Europe group assumed control of the negotiations on the 2040 climate target. The Patriots won the “rapporteurship” in a complex system of attribution. It is the first time that pro-European centrist groups have failed to prevent far-right forces from accessing important files. This means the Patriots will be in charge of defending their own stance in upcoming negotiations and, most importantly, controlling the timeline, potentially delaying the talks. The Patriots are openly opposed to the Commission’s proposal, which could lead, more than to a simple delay in the adoption, to a downward adjustment of the target ambition during the trilogue negotiations required for the proposal’s adoption. In addition, some Member States, such as Hungary and Czechia, publicly criticise the EU’s climate ambitions. Italy, under Meloni, defends an 80 to 85% target for 2040. France, under Macron, agrees on the 90% objective but highlights the necessity of having only a 2035 – not 2040 – target for the next COP.

The Commission still hopes the 2040 target will be approved before the COP 30, planned in November in Brazil. It appears, however, uncertain given the current divisions in the Parliament.

Looking towards 2040: what path will achieve the -90% target?

The recent market trends and political events show that significant additional efforts from all economic actors will be required immediately in order to reach the 90% reduction in GHG emissions target.

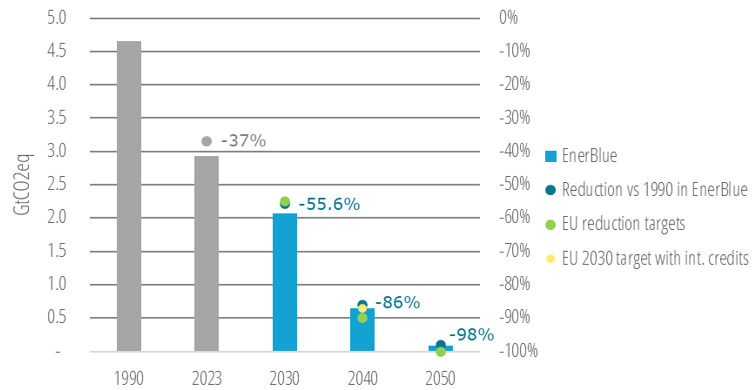

Enerdata’s EnerBlue scenario draws a path to 2050 assuming that the main energy and climate commitments are achieved in the EU. As shown in the graph below, this scenario is well aligned with the EU’s successive GHG emission reduction targets. Therefore, it illustrates a possible path towards achieving the proposed 2040 target.

Figure 3: EnerBlue’s compliance with EU objectives

Source: Enerdata, EnerFuture, Granular Energy Demand Forecast module

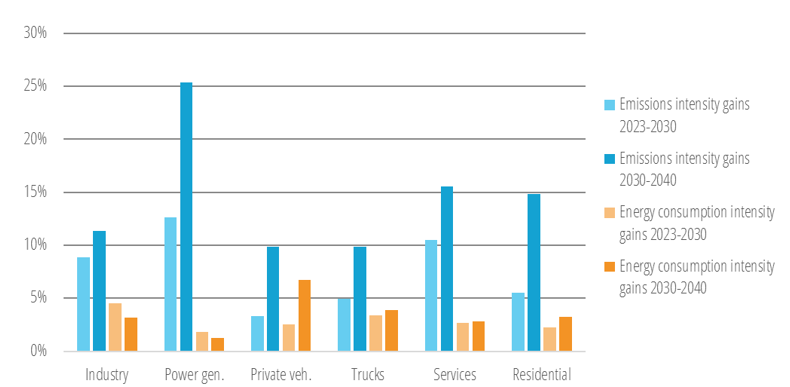

Diving into EnerBlue therefore allows an assessment of the effort required in each sector to meet the EU’s energy and climate ambitions, and to evaluate the impact of a number of policy instruments that are used to support those efforts. The graph below shows both emission and energy intensities gains by sector, comparing the yearly average over 2023-2030 with 2030-2040.

Figure 4: Average emission & energy intensity gains by sector, EnerBlue, 2023-2030 vs 2030-2040

Source: Enerdata, EnerFuture, Granular Energy Demand Forecast module

All sectors are expected to keep increasing their efforts to reach both the 2030 target and the proposed 2040 one, but at different paces and using different levers.

Power generation and Industry

Power generation is already rapidly decarbonising. Achieving its 2030 targets means a decrease of about 13% per year of its carbon intensity (gCO2/kWh) between 2023 and 2030. According to EnerBlue, this rate would need to double between 2030 and 2040, thus enabling power generation to be the first fully decarbonised sector by 2040. The deployment of renewables and the modernisation and adaptation of grids will be crucial to achieve this level.

Industrial sectors would need to decrease their emissions per unit produced by about 10% per year on average over 2030-2040. This results from high energy efficiency gains in technologies used, electrification in all uses where it is possible and useful (i.e. heat pumps for low thermal processes) and process shifts to less carbonised ones (i.e. electric arc furnaces in steel production, less clinker in cement production…). This way, energy consumption could decrease by about 28% over 2030-2040 (37% over 2023-2030).

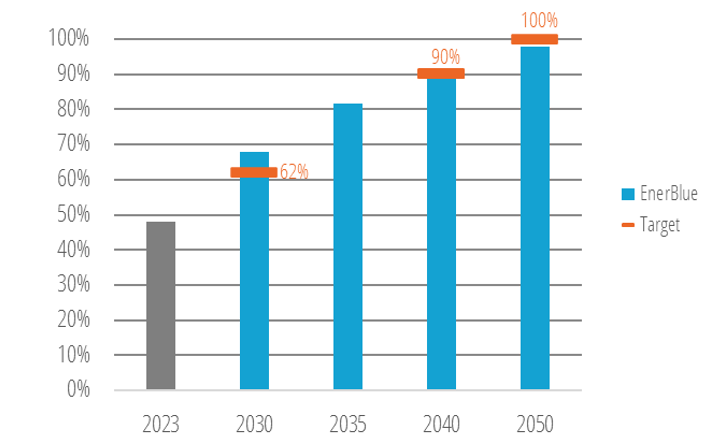

Since 2005, emission reductions in both power generation and industry have been supported by the EU Emissions Trading System (EU ETS)1. This cap-and-trade system accounts for about 40% of EU’s total GHG emissions and therefore plays an important role in helping these sectors decarbonise. As of 2023, 48% of EU ETS emissions had been abated from 2005 levels. According to EnerBlue, they could reach a 68% reduction by 2030, higher than their 62% target, thanks to current plans and policies in force. Sectors covered by the EU ETS may continue reducing emissions to reach -92% in 2040.

Figure 5: EU-ETS emissions reduction vs 2005 levels - EnerBlue

Source: Enerdata, EnerFuture, Granular Energy Demand Forecast module

Transport and Buildings

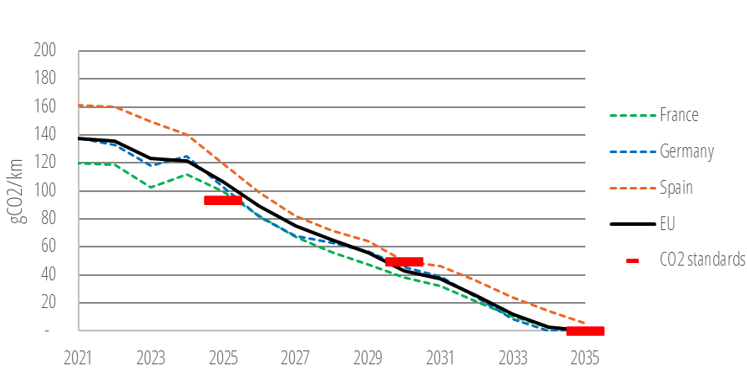

Road transport, and especially private vehicles, are expected to be a game changer for the successful achievement of the 2040 target. Annual per kilometre emission reduction of the vehicle fleet could triple between 2030 and -2040 compared to 2023-2030, partly driven by the tightening of emissions standards for new vehicles. From 2020, regular steps to reduce CO2 emissions from cars and light commercial vehicles have been set, in order to achieve 0 gCO2/km in 2035, as targeted by the EU. Heavy-duty vehicles, more challenging to decarbonise, must comply with their own objectives: -90% in 2040 compared to 2019, with intermediate targets in 2030 (-45%) and 2035 (-65%).

Figure 6: Per kilometre CO2 emissions of new cars - EnerBlue

Source: Enerdata, EnerFuture, Granular Energy Demand Forecast module

The increasing share of electric vehicles (EVs), which are much more efficient than thermal ones, will lead to significant energy efficiency gains in the sector. In addition to the phase-out of sales of emitting vehicles in 2035, other levers such as higher vehicle occupancy rates or the reduction of vehicle weight, may help to achieve the emission reduction target.

Finally, buildings could be one of the sectors with the highest required efforts to achieve the 2040 target. Per dwelling emissions are expected to be reduced by about 5% per year to comply with the 2030 target, and this rate could triple if the 2040 target is adopted. Services are already highly decarbonising their activities but could progress further over the coming decades. The EPBD’s targets are expected to play a key role in the sector’s decarbonisation, by making net-zero emission the standard for new buildings after 2030 and paving the way toward the phase-out of fossil-fuel boilers by 2040. Nevertheless, the reduction of the demand could be similar to other sectors, since efficiency gains due to heat pumps deployment and limited sufficiency could be counterbalanced by the rise of new uses: generalisation of air conditioners, data centres for A.I., new appliances, etc.

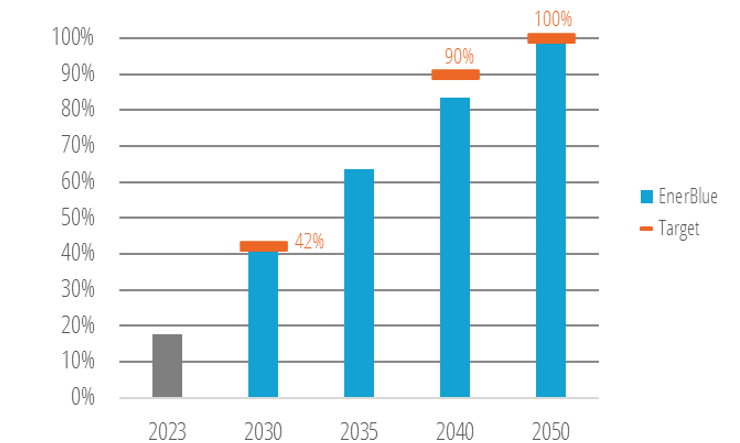

In 2027, a second ETS will become fully operational, covering CO2 emissions from buildings, road transport and small industry not already covered by the first ETS. These sectors will need to reduce their emissions by 42% by 2030 compared to 2005 levels. Currently, they stand at about 20% below 2005 levels and will require immediate and sustained efforts to reach both the 2030 and 2040 targets.

Figure 7: ETS 2 emissions reduction vs 2005 levels - EnerBlue

Source: Enerdata, EnerFuture, Granular Energy Demand Forecast module

Conclusion and Outlook

The EU continues to set out its climate and energy strategy with the European Commission proposing a target to reduce GHG emissions by 90% in 2040 (compared to 1990 levels). However, the EU’s ambitions face challenges of different kinds.

On the one hand, some signs of a slowdown in the markets for decarbonisation technologies have emerged. For example, EV sales declined in 2024, raising concerns about the 2035 end of emitting vehicle sales target. On the other hand, the 2040 Climate target, a key milestone in the EU’s policy agenda towards decarbonisation, faces political uncertainties which could delay its adoption, and even jeopardise its achievement.

Nevertheless, despite the rather negative recent signals, many tools and plans have been deployed and continue to be strengthened: the ETS (1 & 2) mechanisms, vehicle emission standards, Net-Zero Industry Act, EPBD targets, etc. These policy instruments foster decarbonisation across all sectors, hence paving the way for the EU economy as a whole to continue significantly reducing its emissions, and which may hopefully prove solid enough for the proposed 2040 to remain achievable despite the adverse economic and political context.

To conclude, monitoring the upcoming trilogue negotiations and the potential 2025 rebound of clean technology markets, will be key to understanding whether the EU can remain on-track with its ambitions.

KEY TAKEAWAYS

- New proposed target: 90% reduction in EU GHG emissions in 2040 compared to 1990 levels, with up to 3% achieved through international credits.

- Market uncertainties: EV sales fell by 6% in 2024 in the EU, while heat pump installations increased by only 5% in households.

- Political uncertainties: The new balance of power in the European Parliament could delay or prevent the adoption of the target.

- Outlook: The 2040 target remains achievable, but substantial efforts across all economic sectors will be required over the next decade.

Note:

1 The EU-ETS also covers GHG emissions from heat generation, aviation, and maritime transport since 2024.