Request the full publication (FREE)

Anticipating Market Shifts in an Era of Systemic Transformation

As the world accelerates toward climate neutrality, the electricity system stands at the centre of the energy transition. Meeting global climate targets will require not only a massive electrification of end-use sectors but also a complete transformation in how electricity is produced, financed, and traded.

This systemic shift brings profound implications:

- Generation is evolving from baseload-centric models to more dynamic, peak-responsive operations—particularly for gas and coal assets.

- Low- and zero-marginal-cost technologies like wind and solar are becoming dominant, shifting value creation from operational performance to capital-intensive deployment.

- Infrastructure must adapt, with grid expansion, flexibility solutions (demand response, storage), and decentralised generation playing critical roles.

In liberalised markets like Europe, where electricity prices serve as a key signal for investment and remuneration, these shifts raise an essential question:

How will power price dynamics evolve—and what does this mean for the future of revenue models across the value chain?

This is where Power Price Projections come in: designed to bring clarity, precision, and strategic insight into an increasingly complex and volatile market landscape.

Behind the ongoing transformation of the power sector lies a dramatic realignment in where, how, and why investments are flowing.

Renewables are accelerating faster than ever. Thermal capacity is showing signs of structural decline. Nuclear’s trajectory remains complex and long-term. Meanwhile, electricity grids are under mounting pressure to modernise, expand, and adapt—bringing rising costs and growing debate on who should pay, and how.

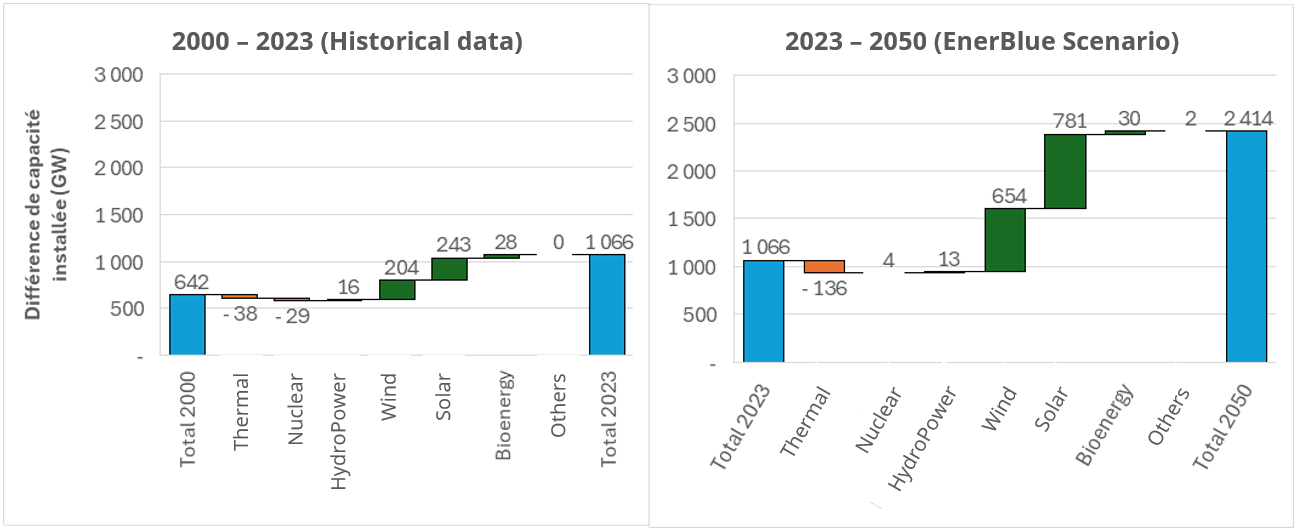

Trends in installed power generation capacity in the EU27 (GW)

Source: Scenarios EnerFuture, Enerdata analysis

Yet these trends are only part of the picture.

Across Europe, the balance between energy generation, infrastructure needs, and flexibility solutions is becoming more intricate—and more politically charged. The electricity bill of tomorrow won’t just reflect spot market prices. It will also embed infrastructure costs, regulatory adjustments, and new models of consumer participation.

How this paradigm unfolds—both in terms of market design and remuneration mechanisms—will shape investment signals for decades to come?

The structure of electricity markets in Europe has entered a new and more volatile phase. While prices were relatively stable before 2021, the energy crisis marked a turning point. Since late 2022, a new paradigm has emerged—marked by growing volatility, price cannibalisation, and a surge in negative price events.

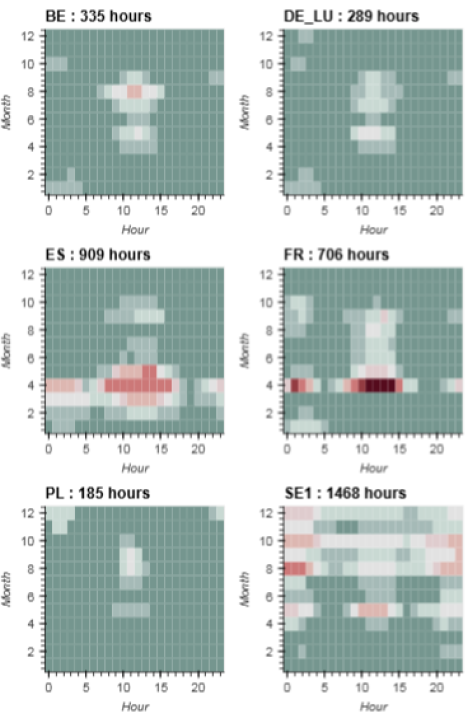

Overview of negative prices in 2024 in a selection of European countries – week days

Source: Source: ENTSOE, Enerdata analysis

Negative pricing is no longer an occasional anomaly. In 2024, it became a systemic feature across multiple European markets, driven largely by high penetration of renewables—especially solar and wind.

These price dynamics are increasingly visible:

- Hourly, during mid-day solar peaks;

- Weekly, especially over low demand weekends;

- And seasonally, in spring and early summer when renewable output remains high while heating and cooling demands are minimal.

What does this mean for market players?

Even projects supported by subsidies like Feed-in Tariffs or Contracts for Difference are feeling the ripple effects. As capture rates for PV fall and PPAs begin to include non-remuneration clauses, developers and investors are now navigating a far more complex risk landscape.

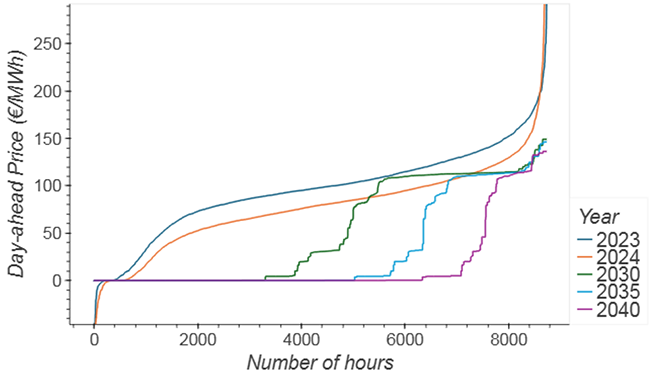

Yearly monotonic price trends (historical and forecasted) in Germany (DE-LU bidding zone) Enerdata exploratory scenario, average climatic conditions

2023/2024: historical data.

Reading example: In 2030, spot prices should be negative or null during 3200 out of 8760 hours (37% of the year).

Source: 2030/2040: Enerdata, Power Price Projections (based on EnerFuture’s EnerBlue scenario)

Spot prices are the main benchmark for market analysis—but interpreting their long-term evolution requires deeper context. While negative price hours can be partly managed through contract mechanisms, the rise in low- or zero-price hours is set to continue, shaped by the pace of renewables expansion and electrification of demand.

Crucially, spot prices do not reflect actual supply costs or system value. Their trajectory depends on key assumptions around CO₂ pricing, fuel market trends, and demand growth—all of which vary widely across scenarios.

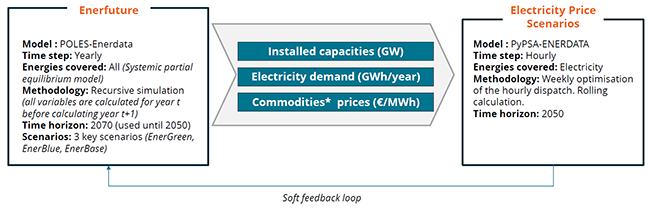

Enerdata PyPsa Model

Download the presentation to get key insights on market trends, grid impacts, and future costs in Europe’s evolving electricity landscape.