Request the full presentation (FREE)

The largest power generation companies are considerably impacting the climate due to their major share of CO2 emissions. Developing renewable energy sources is a key lever to mitigate their impact.

Chinese Generation Companies (GenCos) are the largest in the world, holding 39% of China’s total capacity in 2023 and achieving over 80 GW of renewable installations, surpassing the combined capacities of the EU27 and the US. However, increasing renewables alone will not suffice to meet the Paris Agreement targets without reducing thermal asset development.

Meanwhile, European GenCos have focused on low-carbon strategies since the 2010s, implementing coal phase-out measures and significantly increasing solar and wind capacities. They face challenges with profitability and emissions due to declining nuclear capacity and reduced capacity factors of thermal installations.

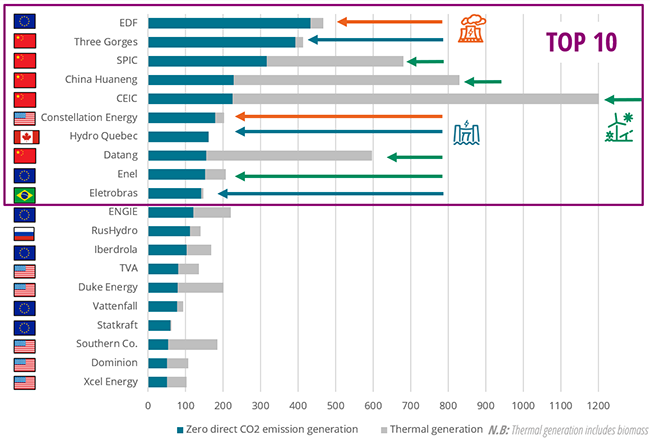

World ranking of zero direct CO2 emissions producers in 2023 (TWh)

Source: Power Plant Tracker, Enerdata

In the global rankings of installed capacity among companies involved in carbon-free thermal power generation, Chinese companies dominate the four out of the top five positions. Among the world’s top ten companies, there is a diverse mix of power generation types. While nuclear and hydropower contribute notably to this capacity, the majority of the companies in these rankings primarily operate wind and solar power facilities.

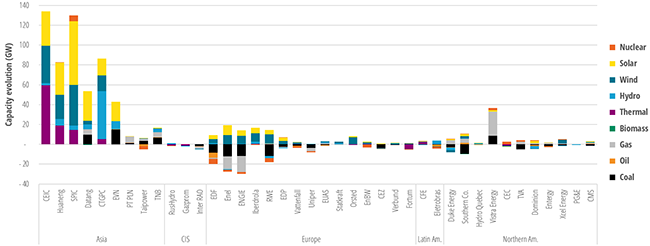

Evolution of installed capacity per energy source between 2015 and 2023

Source: Power Plant Tracker, Enerdata

To analyse the evolution of installed power generation capacity from 2015 to 2023, two key regional trends stand out: the expansion in Asia and the gradual decommissioning in North America and Europe.

In Asia, companies have notably scaled up their generation capacities to meet rapidly increasing demand. This expansion has been marked by a stronger emphasis on renewable energy assets, such as solar and wind, over thermal (fossil fuel-based) assets.

In contrast, North American and European companies show a pronounced trend of decommissioning thermal assets, especially coal and older gas-fired power plants. This decommissioning can occur due to the End-of-Life of the assets or to Policy-Driven Phase-Outs.

Another noticeable tendency is that solar and wind energies dominate in Asia, have a significant presence in Europe, but are very mere in North America due to these projects not being developed by large GenCos but rather by other private well distributed entities.

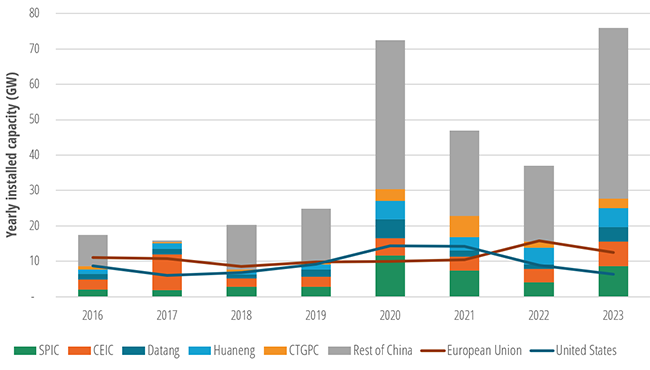

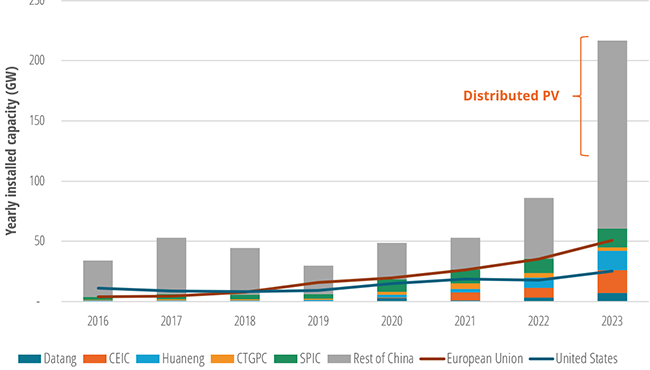

Additional wind capacities since 2016 (GW) - Additional solar capacities since 2016 (GW)

|

|

Source: Power Plant Tracker and Global Energy & CO2 Data, Enerdata

China’s current installed wind capacity appears to be underperforming in reaching the Paris Agreement objectives. Indeed, to fulfil these objectives, China must install an additional 85 GW per year from 2023 to 2030 and 110 GW per year from 2030 to 2050 (source: EnerFuture, Enerdata).

In 2023, China installed over +217 GW/y of solar power, representing 60% of newly installed global capacities. This installed solar capacity is contributing significantly to fulfilling the Paris Agreement objectives. The solar capacities installed by GenCos represent only 28% (+61 GW) of the total capacities in 2023 (vs. 42% during the 2020-2022 period).

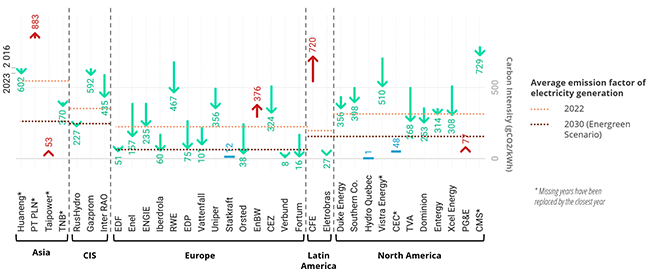

Evolution of the Carbon Intensity of GenCos 2016-2023

Source: Power Plant Tracker and EnerFuture, Enerdata

GenCos around the world are decreasing their carbon intensity, but a few exceptions remain among the major GenCos.