Request the Full Publication (FREE)

Green hydrogen is one of the key concrete solutions for decarbonisation in the energy transition. As a clean energy vector, it reveals new perspectives of development across various sectors.

After gaining traction and becoming the focal point of numerous new policies and technological advancements the momentum of green H2 has stabilised and a more nuanced perspective has emerged.

This report has been co-created by Enerdata and ClimateWorks Foundation. It dives deep into how green hydrogen is facilitating the energy transition. It reviews the main aspects of green H2, including production, geopolitics, technologies, demand, and energy storage capabilities.

Key takeaways

- Production: At the moment, the most popular hydrogen production methods are fossil fuel-derived hydrogen from coal gasification and steam methane reforming. Currently, technically mature electrolyser technologies for hydrogen production include alkaline and PEM (Proton Exchange Membrane), and have reached the mass production stage

- Transportation: Technically mature methods for hydrogen transport include hydrogen transmission pipelines, shipping and trucks. On the other hand, repurposing existing natural gas pipelines for hydrogen transport offers the benefit of utilising already established infrastructure.

- Energy storage: Hydrogen possess a significant potential as an energy storage solution especially for storing renewable energy that is released over a long duration. However, efficiency losses in hydrogen production and reconversion need to be taken into consideration.

- Geopolitics: The supply of raw materials needed to produce hydrogen happen to be dominated by a small group of countries. This situation poses geopolitical risks and vulnerabilities, requiring strategic actions to secure reliable supplies.

- Ammonia challenge: Ammonia plays an important role in a country’s agriculture and is produced using hydrogen as a key input. But this production process is especially susceptible to high gas prices and hence to geopolitical tensions and energy crisis that might arise. Meanwhile, there are other challenges that are associated with integrating renewable hydrogen into ammonia production because of already existing infrastructures.

FOCUS ON GREEN H2 REGULATORY FRAMEWORKS

Greenhouse gas emissions related to hydrogen production vary significantly from one production route to another. In the case of hydrogen production through electrolysis, these emissions depend on the carbon intensity of the electricity used in the process.

Countries typically aim to reduce carbon emissions associated with hydrogen end-uses by establishing regulatory frameworks that include criteria for determining which hydrogen production cases can be categorised as “renewable,” “low carbon,” or “clean” hydrogen. Regarding hydrogen demand, the European Union and the United States are currently the only regions incentivising clean or renewable hydrogen production through tax credits or integrating renewable hydrogen into national fuel consumption policies.

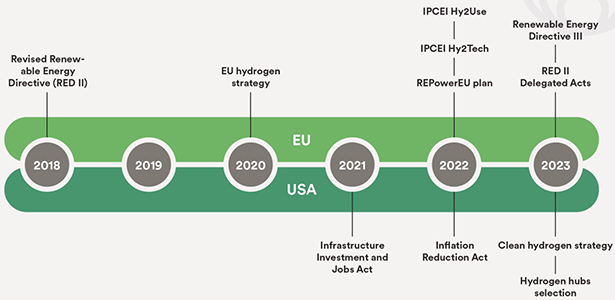

Overview of public policies for the hydrogen sector in the EU and the US

Source: Enerdata

EU REGULATORY FRAMEWORKS

In February 2023, the European Union adopted two delegated acts required under the Renewable Energy Directive II. These acts focus on defining the conditions under which hydrogen and hydrogen-based fuels can be considered as renewable - Renewable Fuels of Non-Biological Origin (RFNBO) within the EU terminology. Three criteria are used to assess whether hydrogen is renewable: additionality, temporal correlation, and geographical correlation.

Criteria for assessing whether hydrogen is renewable in the EU regulatory framework

Source: commission delegated regulation (EU) 2023 Delegated regulation on Union methodology for RFNBOs

These criteria are designed to guarantee that hydrogen produced through electrolysis utilises renewable electricity. The Renewable Energy Directive III, published in October 2023, defines a target of at least 42% RFNBO usage by 2030 in industry within EU Member States.

US REGULATORY FRAMEWORKS

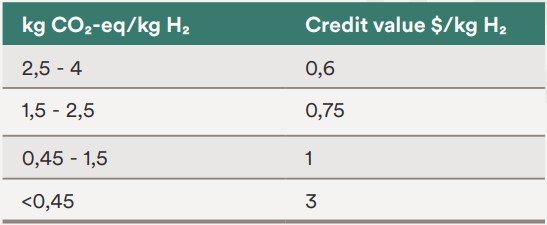

The US Inflation Reduction Act (IRA), enacted in August 2022, introduces a new tax credit applicable to “qualified clean hydrogen”. It proposes a 10-year tax credit offering up to $3.00 per kilogram of hydrogen produced at a specific facility. The credit amount depends on the level of life cycle emissions and staff wages.

Level of life cycle emissions determines amount of tax credit

Source: Enerdata, based on Inflation Reduction Act

Following this act, numerous companies, including European players have decided to enter the US hydrogen market. However, the US Treasury Department has yet to establish criteria for the calculation of emissions intensity for electrolysis-based hydrogen under the clean hydrogen production tax credit. No specific date has been announced for a final draft.