A comparison of the nuclear sectors in the USA, Russia and China

Get this executive brief in pdf format

This Brief analyses the geopolitical strategies of China, the United States and Russia in civil nuclear power. To this end, the approaches of the three countries will be compared for three main pillars of the sector: uranium extraction, fuel manufacture and reactors exports. The interdependent relationships between these three segments will also be highlighted.

Introduction

Studies on the geopolitics of nuclear energy are far less numerous than for other energies, especially hydrocarbons. Existing research often focuses on proliferation issues, while other forms of political uses of civil nuclear power have mainly stayed in the shadows.

Using the same mode of reasoning for nuclear energy as for oil and gas has also introduced another bias: as uranium is perceived to be better distributed globally than hydrocarbons and its energy density makes it easy to store, nuclear power has been falsely perceived as a less risky form of energy. Power plants however do not use raw uranium, but rather a highly transformed version thereof, and its fabrication has its own specific issues. Moreover, the resource-focused approach neglects the importance of the reactors themselves in the geopolitical characteristics of nuclear power.

The security challenges of civil nuclear power have been highlighted by the transformations that the sector is currently undergoing. In June 2020, 413 commercial reactors were in operation in 31 countries, producing 10.15% of the world's electricity. Europe and North America remain the leading producers of nuclear electricity, but the most dynamic markets are in Asia, Africa, South America and the Middle East. Russia and China have shown a growing involvement in civil nuclear power, with national companies (Rosatom in Russia, and CNNC, SPIC and CGN in China) receiving financial support from their respective governments both for their domestic and international markets.

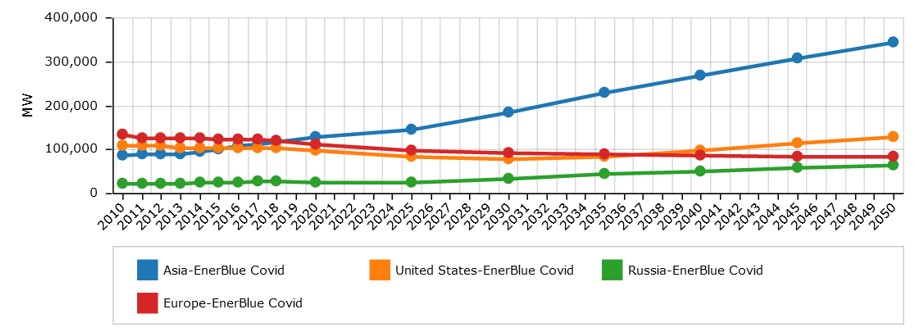

Figure 1: Nuclear electric capacity forecast (MW)

Source: Enerdata EnerFuture

There are two kinds of countries with respect to civil nuclear power:

- Those already equipped and reinforcing their reactor fleet, like China, India, the United States or the United Kingdom.

- New entrants to the club, such as Bangladesh, Turkey and the United Arab Emirates, and countries that have expressed the ambition to do so.

As only a few countries and companies are exporting nuclear technology, it raises the possibility for the new entrants of a coercive use of fuel supply or of a foreign control of power plants. There are also interrogations about the emergence of hybrid forms of energy dependency and a growing competition in the supply market. At the same time, the deployment of reactors in hitherto non-nuclearised countries will have major geopolitical consequences.

The organisation of the Chinese, Russian and US nuclear industry.

Russia, China and the United States have radically different nuclear industries, linked to their historical development, geopolitical strategies, power rivalries and specific internal processes. Each industry structure is a fundamental component of their projection capacity abroad.

Russia's industrial sector is vertically structured around Rosatom, which controls the entire civil nuclear value chain, from uranium mining to waste management through fuel production and the construction, sale and operation of reactors. This vertical integration is one of Russia's major assets in the export of nuclear technology. Rosatom is a single point of contact and provides an integrated offer to countries seeking to develop nuclear energy.

The Chinese nuclear industry is organised around three major groups: the China National Nuclear Corporation (CNNC), the China General Nuclear Power Corporation (CGN) and the State Power Investment Corporation (SPIC), which control the entire value chain of the sector. Despite the efforts of the government to avoid a cannibalisation of Chinese interests internationally, the three entities frequently find themselves competing in the same markets. However, CNNC has taken the ascendancy over its rivals by offering a one-stop-shop for civil nuclear energy to the foreign buyers, based on the Rosatom model.

While the United States remains by far the most nuclearised country in the world, the US industrial fabric has contracted sharply since the Three Mile Island power plant accident in 1979. Of the four reactor manufacturers that the country had in the 1970s, only Westinghouse still has a conventional (light water) reactor in its catalogue. The financial difficulties of nuclear power plant operators, penalised by market economy conditions and Washington's rules on the export of nuclear goods and services, have led to a structural decline of the industry on the world market. In fact, no reactor currently under construction internationally comes from the USA, while Russian and Chinese manufacturers are multiplying export contracts.

Outlook: the new uranium routes

Securing uranium convoys

The possible opening of new mines, particularly in Africa, calls for the standardisation of convoy security practices, particularly for landlocked deposits. Uranium is a high-density ore, and thus volumes are quite low compared to oil or gas. Moreover, its transport does not rely on fixed infrastructures such as pipelines. However, the distance between mines and fuel production plants in Europe, North America, China and Russia requires long-distance travel for which there is currently no standardised approach. In the case of deposits located in landlocked countries, the uranium is conditioned in 200-litre steel drums in containers placed on lorries and/or trains and then transferred to ships, with safety requirement which differ a lot from country to country (and even within countries). Transit countries have their own regulations, which can further complicate uranium transportation.

Strategic transit points to watch out for

Some transit points will be taking on strategic importance in the future due to the reconfiguration of the geography of uranium production and consumption as well as the intensification of these exchanges, namely:

- In Southern Africa, Walvis Bay in Namibia, which is facing serious challenges in terms of saturation of logistical capacities and road congestion. Dar-es-Salaam (Tanzania) is also considered as an alternative.

- In Russia, two cross-border entry points for Kazakh uranium imports (Lokot/Rubtovks in the Altai, Zernovaya/Zauralye in the Kurgan Oblast), and St. Petersburg for all imports from other countries. Rosatom also plans to develop eastern and southern routes via the ports of Vostochny (Sea of Japan) and Taganrog (Sea of Azov).

- For China, the Alashankou (and now Khorgos) border stations in Xinjiang (China) for Kazakh imports. For other imports there are three main ports: Shanghai, North Yangshan and Zhanjiang; and three smaller sites on the Yellow Sea (Dalian, Qingdao and Tianjin).

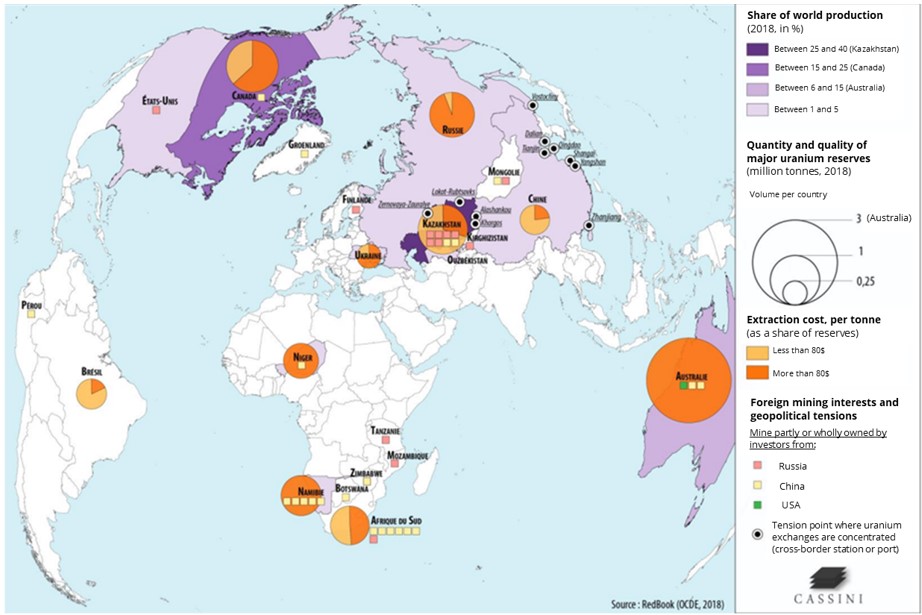

Figure 2: Uranium resources and production

Source: RedBook (OECD 2018)

Nuclear fuel production: risks to watch out for

The complexity of nuclear fuel fabrication is of growing geopolitical importance and increasingly dominated by Russia. In a market that suffers from production overcapacity, Russia has become a key player in the value chain, to the detriment of the US industry. And Rosatom largely dominates the supply of fuel assemblies for Russian technology reactors, locking up the market.

The nuclear fuel production market consists of three main segments: conversion, enrichment, and fuel assemblies. These three market segments have significant overcapacities. For example, 45% of the global capacity of conversion were idle in 2019.

Rosatom (Russia) was the world leader in nuclear fuel production in 2019, with 35% market share in the conversion segment and 36% in the enrichment segment. The existence of global overcapacities limits the risk of Russia using its position in a coercive manner. But the Russian geopolitical influence is more noticeable in the assembly segment. Indeed, Rosatom is practically the only one that can supply the fuel required by the nuclear power plants of the former USSR and there is currently no alternative for the future VVER-1200 models exported to Egypt, Turkey, Bangladesh, Belarus and Finland. In addition, since 1993, Russian industry has been developing fuel assembly for Western-manufactured nuclear power plants.

China has launched an offensive strategy to develop its production capacities for nuclear fuel. The Chinese industry was already capable of meeting the needs of its fleet of nuclear reactors in 2019. China aims to increase even more strongly its fuel production to gain international market share. At present, Chinese fuel exports remain limited due to the limited number of reactors sold abroad. But this situation could rapidly change: CNNC is already active in Pakistan and the group is positioned in Kazakhstan and Ukraine.

The US fuel production industry is in a bad position, and manufacturing capacity has been drastically reduced in recent years. The only remaining conversion plant, located in Metropolis in southern Illinois and operated by ConverDyn, has been idle since November 2017. The country was entirely dependent on the foreign conversion offer in 2019 and 75% of the services of enrichment came from abroad, mainly from Russia. The Department of Energy and the Nuclear Fuel Working Group formulated a strategy to support the sector in 2020 but its funding was partly rejected by the Democratic majority in the House of Representatives.

The export of reactors: security challenges and geopolitical strategies

As highly technological infrastructures, reactor sales are characterised by long-term relationships between the buyer and his supplier, particularly for non-nuclearised countries. In this sector also, the historical hegemony of the United States has collapsed in favour of China and Russia, whose projection abroad relies as much on using their domestic markets as a window as on the political activism of their respective governments.

The main growth drivers of the world reactor construction market are in Eurasia. As of August 2020, 54 units were under construction in 19 countries in Asia, notably in the Pacific (China, India, South Korea, Pakistan) and the Middle East (Turkey, UAE). The same applies to countries considering nuclear power for their electricity mix.

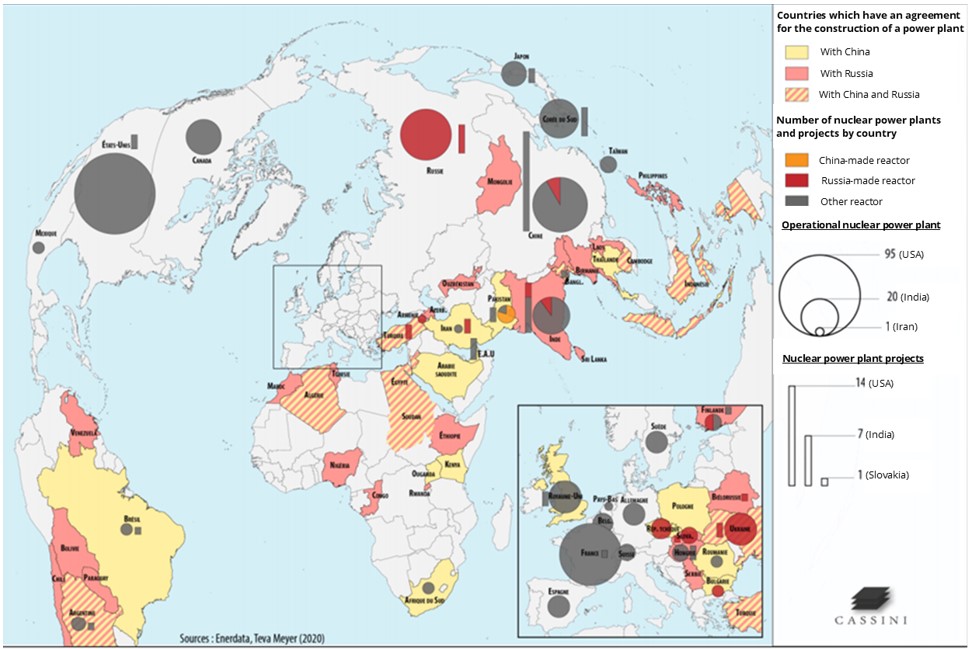

Figure 3: Russian-Chinese rivalries over the supply of nuclear power plants

Source: Enerdata, Teva Meyer (2020)

Rosatom has been the world leader in the construction of nuclear reactors for several years, with 30% market share in 2019. Rosatom was working in August 2020 on 21 reactors in 12 countries. The construction of power plants abroad enables Russia to achieve geopolitical objectives, such as the militarisation of the Astravets power plant in Belarus and the reinforcement of the Baltic countries' electrical dependence on the Russian grid.

The export of nuclear power plants is an imperative for the Chinese industry, which is penalised by the delay in China's nuclear park extension programme. CNNC and CGN have the objective of exporting reactors to 41 countries. The Hinkley Point project in the United Kingdom is crucial for Beijing to have a gateway to Europe. But tensions between Washington and Beijing collide with China's plans in countries allied with the United States. Romania for instance has preferred to cancel the Cernavoda power plant project.

The United States has lost its hegemony. The drop in public orders has led to a loss of capacity and know-how of the US industry on crucial components (steam generators, pressure vessels, pressurisers, etc.). The export activity has been penalised by the lack of vigorous nuclear diplomacy and by the constraints imposed by the federal government's non-proliferation measures.

Take-aways:

- Nuclear energy provides 10.5% of the world’s electricity, and more and more countries are using or considering it in their mix, as a decarbonated and non-intermittent source of energy. Different world regions however have very different strategies, with a reduction of capacity expected in Europe (with nuclear phase outs), while Asia’s appetite for more electricity will spur a strong nuclear growth.

- While the USA had an historic leadership in the sector, its nuclear industry has shrunk and become sluggish in comparison to Russia and China, where the domestic markets are much more dynamic, and international appetites stronger.

- Russia is the current leader in nuclear exports, both in terms of fuel production and reactor construction. China has turned inwards for a longer time as its domestic fleet sharply expanded (a still ongoing process) but is now looking to play a decisive role in the international markets.

- Uranium’s geopolitical value has long been considered less critical than for fossil fuels, but current market pressures and a growing number of reactors have led to the main players (such as Rosatom or CNNC) to diversify their supplies.

This Executive Brief stems from an analysis by Enerdata, the French Institute for International and Strategic Affairs (IRIS) and Cassini for the French Ministry of Defence (full report available in French here).

Annex A: The fundamentals of the world uranium market

The amount of uranium reserves available depends on several factors, including the cost of resource extraction. There are about 2.1 billion tonnes that can be extracted at less than 80 USD/kg, and an additional 8 billion tonnes of uranium reserves are economically exploitable at less than US$260/kg.

The world's uranium reserves are (unequally) spread over 52 countries. 78.7% of the uranium reserves exploitable at less than 80 USD/kg are located in 5 countries: Kazakhstan (30.8%), Canada (15.0%), South Africa (11.1%), Brazil (11.1%) and China (10.7%). Australia has no exploitable reserve below USD 80/kg but concentrates about 30% of the world's exploitable uranium reserves at USD 130/kg, ahead of Kazakhstan (14%) and Canada (8%).

A handful of countries in the world account for the bulk of uranium production. Kazakhstan is the world leader. Its production of 22,808 tonnes of uranium (tU) in 2019 is more than Canada's (second largest producer with 6,938 tU), Australia’s (6,613 tU), Namibia’s (5,476 tU) and Niger’s (2,983 tU) together.

Ten companies accounted for 94% of world production in 2019 with a strong domination of the Kazatomprom group (Kazakhstan). Orano (France) was the second most important world producer, ahead of Cameco (Canada), Uranium One (Russia), CNNC and CGN (China).

After a sharp rise at the end of the 2000s, uranium prices have continually depreciated following the Fukushima accident, to fall in April 2020 to 88 USD/kg on the spot market and 83.6 USD/kg for long term contracts. This has caused mines to close, limited exploration projects and increased the attractiveness of countries with low production costs. These price pressures are partly related to the existence of large inventories and to the opportunities offered by secondary supplies, such as the reprocessing of fuel.

Annex B: The fundamentals of the global nuclear fuel market

- Overview of reactor types

Fuel production varies according to the type of reactor, which can be divided into three categories:

- reactors operating with water cooling (PWR, BWR, LWGR),

- pressurised heavy water reactor (PHWR),

- gas-cooled reactors (GCR).

Fast Breeder Reactors (FBRs) are another category but only three units were in operation in 2020. It is also possible to divide the park between Russian and Western models.

- Manufacture stages

PHWRs have a fuel fabrication line requiring the few operations. Yellowcake (nickname for the uranium concentrate produced at the mine exit) is packaged in uranium dioxide or trioxide powder and directly assembled into fuel without mandatory prior enrichment. Seven countries are in a position to achieve this operation: Canada (which has two sites), China, India, Pakistan, South Korea, Romania and Argentina (each with a single site).

The process is more complex for other types of reactors and consists of three main stages.

- Yellowcake must be converted into uranium hexafluoride (UF6). Only Five countries are in a position to carry out this stage: China (two plants), France, Canada, the United States and Russia (one plant).

- UF6 is enriched to increase the content of uranium 235. In spite of a less centralised spatial distribution, with sites in 13 countries, this market is concentrates around three players: Orano (France), Rosatom (Russia) and CNNC (China).

- UF6 is transformed into uranium dioxide powder (UF2) then compressed into pellets and grouped into assemblies. The exact architecture depends on both the type of reactor and its origin and manufacturer. A total of 21 factories in 13 countries could achieve this milestone by 2019.

- A segmented market with overcapacity

Power plant operators do not always buy the assembled fuel, but order uranium, conversion, enrichment and fabrication services separately.

In 2020, the uranium conversion market was in over-capacity, using only 55% of its means of production. The same is true for enrichment, with a use rate of its production capacity of only 86%. Statistics on the volume fuel assemblies are more difficult to establish but also indicate a market in overcapacity.

Annex C: the fundamentals of the world nuclear reactor market

- An expanding nuclear power plant park

As of August 2020, there were 413 commercial reactors in operation in 31 countries around the world, to which are added 26 units that have been shut down for more than a year pending a potential recovery, including 24 in Japan. In August 2020, 54 units were under construction in 19 countries.

- A growth with many unknowns

The future development of the park depends on several unknowns. First, since the average age of operating reactors is 30 years, the question is whether these units will be extended, stopped or replaced. Secondly, while some 20 countries have expressed their wish to use nuclear power, the level of implementation of these projects differs greatly. The IAEA's projections envisage two scenarios, the first of which assumes a decrease in the global production capacity to 350 GW(e) until 2050, with the second projecting an increase to 874 GW(e).

- A market increasingly oriented towards Eurasia

The eastward shift of the market is increasing. Western reactor suppliers are being replaced by Russian, Chinese, South Korean and Indian engineers delivering 80% of the units under construction. And almost all the planned units are found in Asia (China, India, South Korea, Pakistan) or the Middle East (Turkey, UAE). The same is true for countries considering nuclear power.

- A highly variable share of nuclear power in electricity generation

Globally, nuclear power accounted for only 10.15% of electricity generation. However, there are significant differences between France, where nuclear power generated more than 70% of electricity in the country in 2019, and Brazil, where the share of nuclear power amounted to only 2.7% of the total. The United States remained by far the largest producer of nuclear electricity in absolute value, with a 2019 production twice as high as that of France.

Annex D: geopolitical issues in the management of spent nuclear fuel

The proliferation risks associated with the management of spent nuclear fuel are well known. Their reprocessing in a "closed" cycle, as opposed to the "open" cycle where the waste is directly stored, allows the production of plutonium, which can be mobilised for military programmes. However, the downstream end of the fuel cycle includes other issues specific to the geopolitics of civil nuclear power.

Firstly, Rosatom uses supply-backed spent fuel return agreements as a selling point for non-nuclearised countries for which the construction of the infrastructure needed to manage them would be economically and socially costly. This clause has already been introduced in export contracts in Astravets (Belarus), Rooppur (Bangladesh) and Akkuyu (Turkey), for which Rosatom has undertaken to take back spent fuel for reprocessing and storage in Russia. The Russian law so far only allows temporary imports of waste before it is disposed of. However, it will need to be modified to meet these commitments.

Secondly, fuel reprocessing represents a crucial step in the "Three-step strategy" adopted in 2005 by Beijing. The objective is to transform China's nuclear fleet in three stages, first using pressurised water reactors consuming uranium until the 2020s using, then ensuring a transition until 2050 towards fast breeder reactors consuming plutonium produced by reprocessing the fuel used in the previous stage, before deploying fusion reactors when the technology will be available. China is currently experimenting with prototypes of breeder reactors, but its nuclear industry is not yet ready for the transition.