The potential of a booming renewable technology

Get this executive brief in pdf format

Thirty years after the commissioning of the first ever built bottom-fixed offshore wind park by the Danish company Ørsted in 1991 (5 MW)1, offshore wind projects have now flourished across the globe. Mature economies accessing North Sea and Baltic Sea such as Denmark, the United Kingdom, Germany, the Netherlands, and Belgium pioneered the market with pilot projects. Nowadays, while climate emergency imposes governments to boost their energy-climate policy ambitions, offshore wind is featured in numerous national renewable development plans as a reliable RES technology.

The COVID-19 outbreak may have delayed some RES auction schedules or the commissioning date of new offshore wind parks, but dynamics are there and remain robust. Lastly, on the policy front, Spain endorsed its Roadmap for the Development of Offshore Wind and Marine Energy in December 20212. The plan includes the objective to reach between 1 GW to 3 GW of floating offshore wind capacity by 2030. In January 2022, as part of its enhanced objective of 80% of renewables in its energy mix by 2030, Germany targets 30 GW of offshore wind capacities by 2030 and at least 70 GW by 20453. The USA plans at least 7 offshore wind auctions by 20254, while the UK has just opened its 4th Allocation Round – Contract for Difference (CfD) scheme (December 2021) reserving a £200m Pot 3 budget to offshore wind5. Finally, on January 17th, 2022, Crown Estate Scotland awarded 17 offshore wind projects out of a total of 74 applications for its Scottish offshore wind leasing round, ScotWind leasing. The total leasing contracts cover 24.8 GW new capacities of which 60% will be erected on floating technology6.

Thus, we can logically wonder on what key success factors are built the current market dynamics and what the long-term prospects are. In particular, what role do the auction mechanisms and public support schemes play in the offshore wind technology development?

State of the offshore wind market: a momentum lastly driven by China, previously by northern Europe

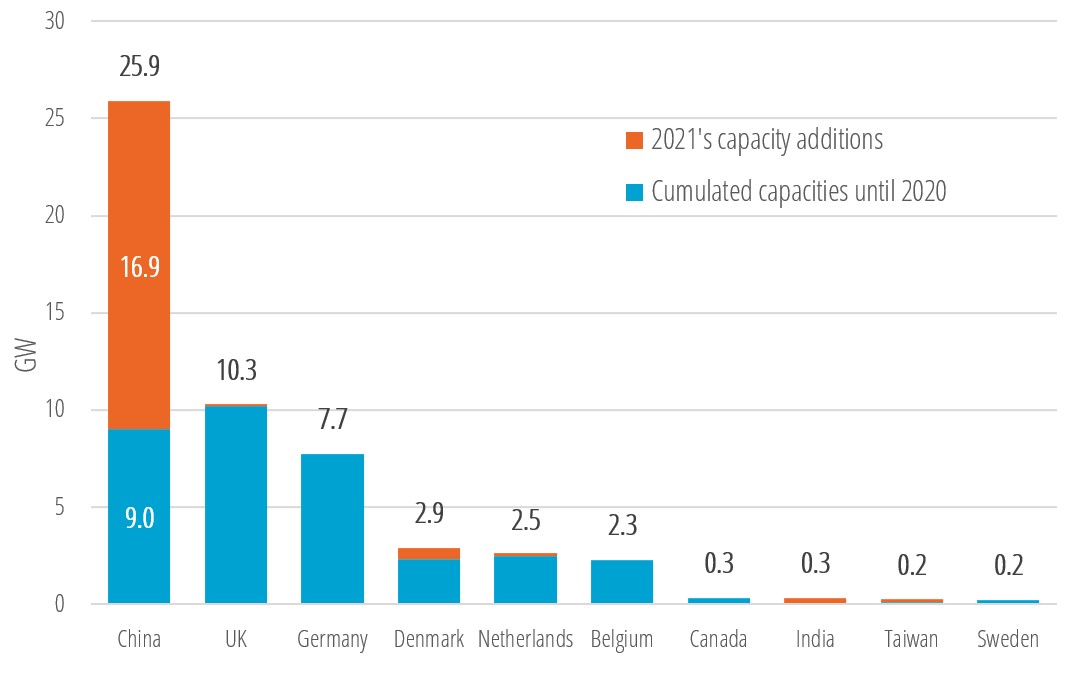

As of end 2021, the top ten countries in terms of installed offshore wind capacities (cf. figure 1) demonstrates a clear domination of China. Indeed, the country recorded a historical volume of new installed capacity in 2021, reaching 16.9 GW. This capacity is higher than that of European countries combined since 2016 (15 GW). At the end of 2021, offshore wind capacity in China (25.9 GW) almost reached that of Europe (26.2 GW). Behind the giant Asian country, the European market is led by the UK that registered a steady growth with annual addition of 880 MW on average since 2010 and by Germany (+750 MW/year on average) (cf. figure 2). The US is not even in the top ten countries with only 40 MW installed. Although the sleeping giant is about to wake up: projects representing 16 GW are currently under development.

Figure 1: Installed offshore wind electricity capacity (MW) – Top Ten in 2021

Source: Enerdata, Power Plant Tracker (PPT)

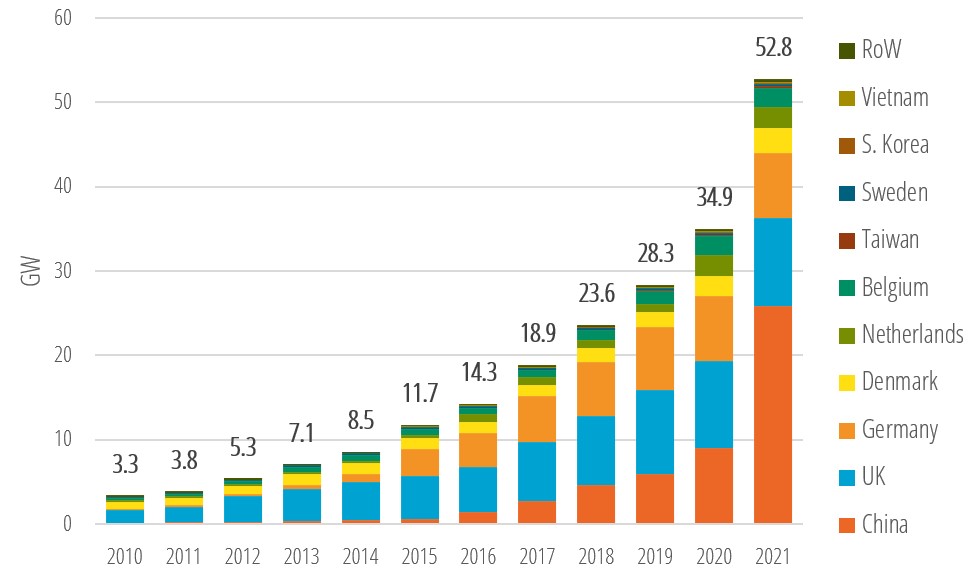

Figure 2: Cumulated offshore wind capacity (GW) by country, 2010-2021

Source: Enerdata, Power Plant Tracker (PPT), Global Energy and CO2 Data

Today, if offshore wind remains reserved for a few countries with sea access, landlocked countries can have their role to play too as shown by the recent cooperation between Luxembourg and Denmark to build the first offshore wind island project7. Taking a regional perspective, offshore wind market dynamics is currently driven by northern Europe, Asia and the USA.

As a pioneer, northern Europe benefits from coordinated countries backed by European policy support, such as the 2020 EU Strategy on Offshore Renewable Energy. The European Commission proposes to reach 60 GW offshore wind capacities by 2030 and up to 300 GW by 20508. The EU can also count on leader countries such as Denmark at the forefront of offshore power technologies. The Danish Energy Agency is developing Energy Islands in the North Sea and in Bornholm in the Baltic Sea; they will serve as an infrastructure hub to connect offshore wind parks and power systems in the region around the two seas9.

At the end of 2021, only 42 MW of offshore wind capacity were operational in the USA, despite a wind-rich potential along the US East Coast and Pacific Coast. Nevertheless, 16 GW are already in various phases of development and the US Department of Energy reported 35 GW of offshore wind projects in the longer-term pipeline in its 2021 market report10.

Asia - and China as a leading country - display high ambitions as well. At the end of 2020, 400 wind companies signed the Beijing Declaration and committed to the installation of more than 50 GW per year of new wind capacities (onshore and offshore) from 2021 to 2025 and more than 60 GW annually from 2026 onwards11. The Global Wind Energy Council (GWEC) estimates a total 52 GW offshore wind capacity to be grid-connected from 2019 to 203012. At smaller scale, other Asian countries have nothing to envy as offshore wind projects are popping up. For instance, many projects are developed in Taiwan (target of 15 GW by 2035) and in Vietnam, including projects proposed by foreign developers and investors, such as Ørsted with a recent 3.9 GW project in Hai Phong13, Copenhagen Infrastructure Partners (CIP) with the 3.5 GW La Gan project in Vietnam14 or Iberdrola’s plans to develop three offshore wind projects (6 GW) in Taiwan.

The key success factors behind the offshore wind market development trends

Stars are currently being lined up on the global offshore wind market between:

- A fast-evolving and increasingly competitive technology (i.e., high load factors, with continuously decreasing LCOEs),

- Ever more ambitious national RES development plans, proven public support schemes (i.e., feed-in-tariffs and feed-in-premiums),

- A streamlining industrial supply chain, the rise of O&G actors up-skilling to offshore wind activities, and

- A growing appetite from commercial banks and institutional investors.

Offshore wind is a capital-intensive RES technology that emerged thanks to pilot projects initially subsidized by public funds. Offshore wind projects are now supported through nationally tailored auction mechanisms, introducing market competition rules in the public support schemes, and selecting the best competitive offer15.

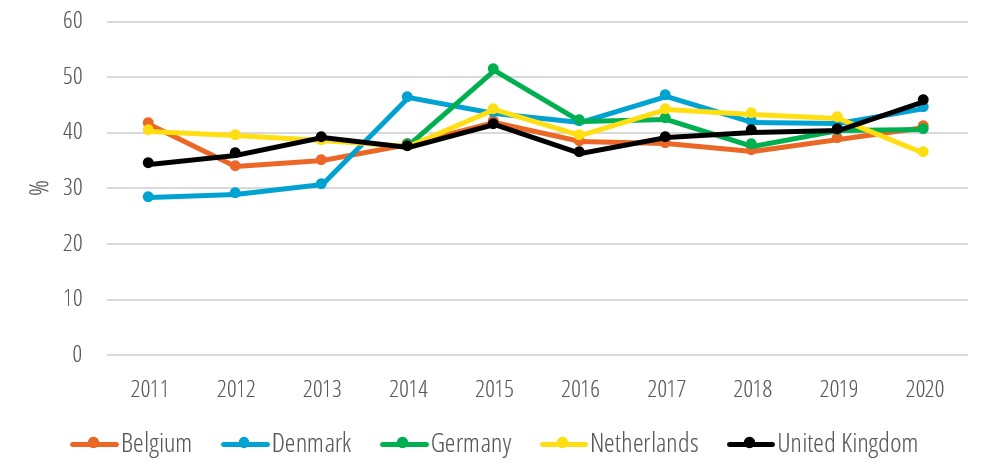

Over the years, offshore wind technology significantly gained competitiveness, notably thanks to improved load factors (i.e., larger and optimised turbines, less curtailment periods). For instance, Danish wind parks reported an average load factor about 40% over 2011-2020 (cf. figure 3).

Figure 3: Average annual load factors for offshore wind parks in selected countries (%), 2012-2020

Source: Enerdata, Global Energy and CO2 Data

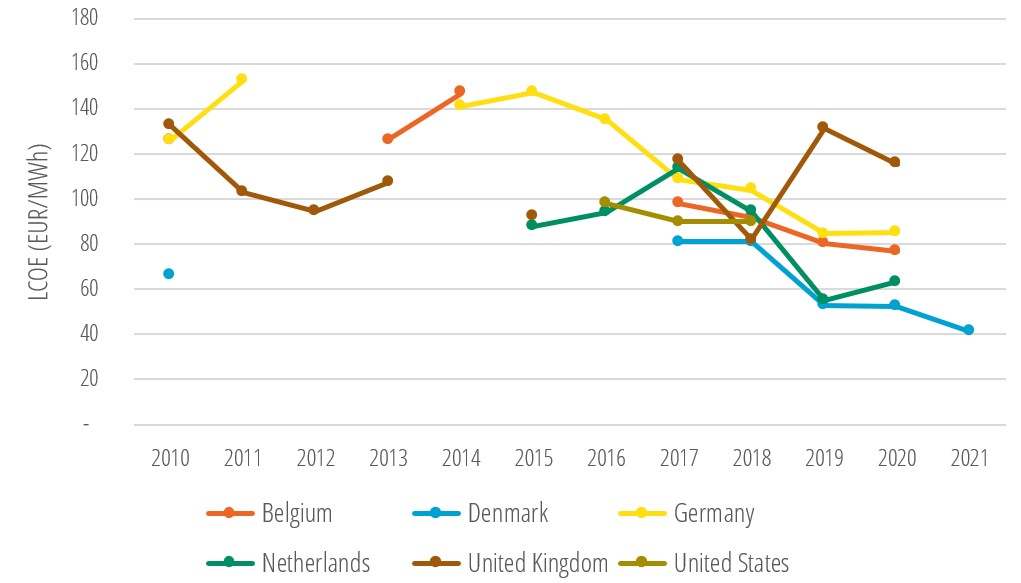

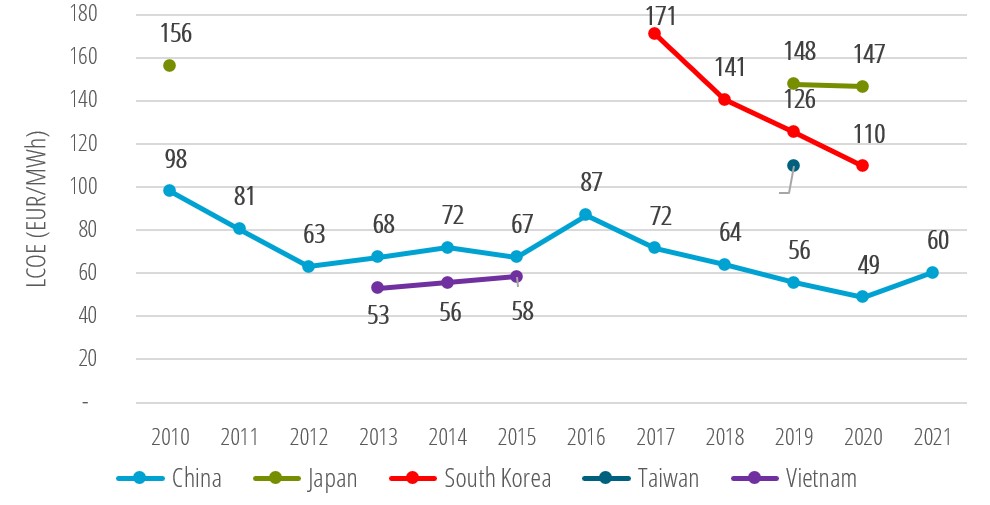

Thus, from the technology cost perspective, good load factors enabled to have historical LCOEs significantly converging downwards. The offshore wind LCOEs are already competitive in European mature markets, such as Germany and the Netherlands with zero-subsidy projects.

Figure 4: Historical offshore Wind LCOEs (EUR) over the 2010-2021 period for Europe and the US, WACC 5%

Figure 5: Historical offshore wind LCOEs (EUR) over the 2010-2021 period for Asia, WACC 5%

Undoubtedly, the decrease in LCOEs facilitates access to capital and contributes to enhanced financing terms. Indeed, as the technology requires a lot of upfront capital (foundation, turbine, installation, transmission, and cabling), capital access and underlying weighted average capital cost (WACC) are a key component to consider. Today, more and more investors are looking for greening their investment strategy and thus entering the offshore wind market with confidence enabling to drive capital costs down. For instance, green bond financing with underlying offshore wind assets is very successful with investors16.

Besides, the supply chain is being consolidated in a context where utilities worldwide are transitioning from brown to greener power. Offshore wind technology is thus a suitable asset class for O&G actors with significant financial resources to leverage their in-house technical expertise and gain access to large-scale projects. For instance, in January 2021, the New York State Energy Research and Development Authority (NYSERDA) selected the partnership between Equinor and BP as the winner of the state’s second offshore wind auction to develop the 1 260 MW Empire Wind 2 and the 1 230 MW Beacon Wind 1 offshore wind projects17. Very recently, Crown Estate Scotland awarded 17 projects for its ScotWind Leasing round, totalling 24.8 GW new capacities, including BP Alternative Energy Investment (2.9 GW), Shell New Energies (2 GW) and TotalEnergies (2 GW)18. Synergies can be created between O&G actors and offshore wind developers to manage far off the coast and offshore projects in deep sea.

Nevertheless, offshore wind market is far from being easily accessible as the barriers to entry are high. Offshore wind projects almost exclusively start at a large-scale level requiring significant financial backup (funding pool). As decision makers, local public authorities set the legal and administrative framework with eligibility criteria to select the project developers. Thus, project applicants shall show their financial solvency, technical expertise with proven track record, and obtain all due administrative authorizations. The eligibility assessment process can easily take months, even years. In France, the first ever offshore wind 480 MW project in Saint Nazaire was awarded in 2012 but is expected to be operational by the end of 2022 after suffering multiple delays due to authorisation periods and recourses19. All these factors may deter smaller RES players to enter the market for the benefit of incumbent actors with established industrial supply chain.

Focus: The role of the RES auctions in northern Europe in the deployment of offshore wind

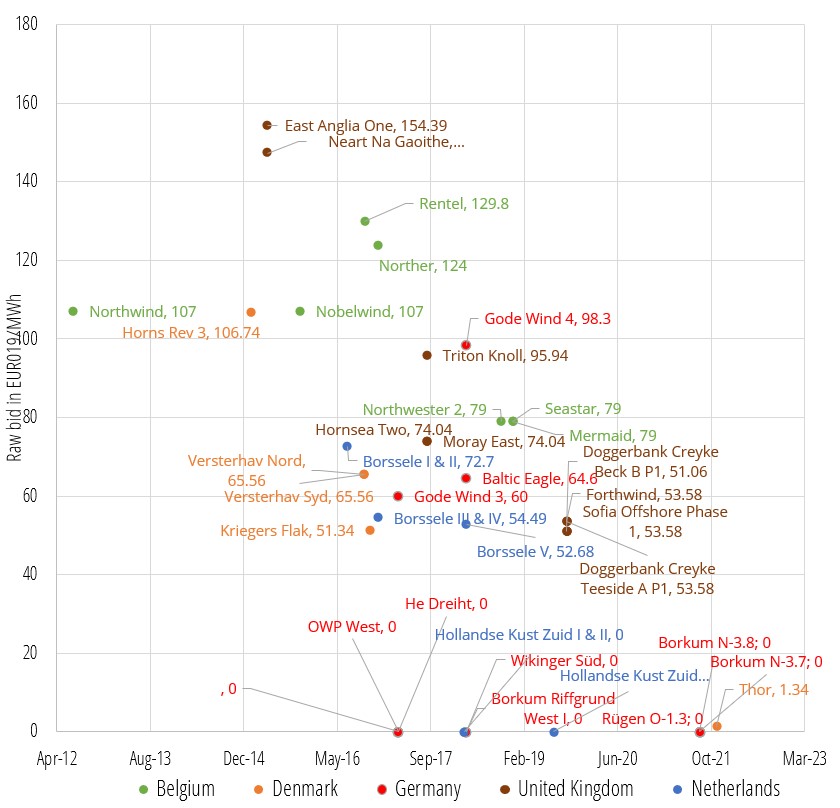

RES auctions or tendering procedures are an increasingly popular tool used by public authorities (e.g., energy regulators and/or Ministries of Energy) to attract and select the most suitable RES project developers. Structured with or without price-based public support schemes (e.g., feed-in-tariffs, feed-in-premiums, investments grants, etc.), the auctions enable to introduce market competition within a transparent regulated framework set by the auctioneer. In this manner, auctions participants are prompted to align their bidding offer with the market, driving prices down and avoiding undue windfall profits from the public authorities to the RES auction winner(s).

Figure 6: Historical auction results (EUR/MWh) over the 2012-2021 period for northern Europe

Source: Malte Jansen, Iain Staffell, Lena Kitzing, Sylvain Quoilin, Edwin Wiggelinkhuizen, Bernard Bulder, Iegor Riepin, Felix Müsgens (2020). Offshore wind competitiveness. Updated by Enerdata (2021)

First European offshore wind projects needed policy support to attract developers and investors offsetting high-risk premiums by securing long-term contracts with public subsidy schemes. The UK was particularly imaginative with the design of Contracts for Differences or CfDs. Participants bid for a strike price, which will determine the level of subsidies granted by the public authorities to the auction winner(s). If the wholesale electricity price is below the strike price, the public authorities offset the delta to the winner(s). On the contrary, if the electricity price is above the strike price, the RES developer(s) shall pay for the delta to the public authorities. This double-siding mechanism enables to reduce price volatility and optimise public subsidies20.

The other European countries have implemented other types of auction-based public support schemes (e.g., on-sided feed-in-premiums, etc.) different from the UK’s CfD framework, from which emerged “subsidy-free” results, notably in the Netherlands and Germany (cf. figure 5). Indeed, in September 2021, as part of its new so-called “central model”, the German Bundesnetzagentur awarded two projects in North and Baltic Seas (i.e., N-3.7, 225 MW and O-1.3, 300 MW) to RWE Renewables Offshore Development and one project in North Sea (i.e. N-3.8, 433 MW) to EDF Offshore Nordsee totalling 958 MW21. Not only they proposed a 0 EUR/MWh premium, but as other competitors also submitted subsidy-free offers, they were awarded by lottery. As well, the Danish Energy Agency had to draw lots in December 2021 to award the 1 GW Thor offshore wind project after several bids offered the maximum capacity and minimum price (0.01 EUR/MWh) for the project.

In December 2019, the Dutch Ministry of Economic Affairs and Climate Policy awarded Chinook CV, a subsidiary of Nuon/Vattenfall to build and operate the Hollandse Kust (zuid) Wind Farm Zone Sites I and II (350 MW) at a zero premium rate too22.

Latest European “zero-premium” offers undeniably show the attractivity of the offshore wind technology, its increasing competitiveness along with the success of regulated RES auction procedures. Nevertheless, they are not totally subsidy-free as the transmission costs will be socialised, i.e., borne by the Transmission System Operator (TSO): TenneT in the Netherlands) and in the end by the public community (e.g., Germany).

Eventually, a recent study released in Nature Energy Academic Journal23 harmonised the expected revenues in recent offshore wind projects awarded via auctions for the five northern European countries (the UK, the Netherlands, Belgium, Germany, and Denmark). Solving the structural differences in the national auction design, the study comes to the conclusions that offshore wind parks can be commercially competitive in mature markets. Indeed, between 2015 and 2019, the price paid for offshore wind power across northern Europe decreased by 12%/year to reach an average price of €51/MWh in 2019. Besides, despite significant auction design features, the countries received comparably low bids.

Mid and long-terms prospects

In 2019, the Imperial College London and the IEA conducted a thorough geospatial analysis to map the speed and quality of wind along hundreds of thousands of kilometres of coastline worldwide24. Thus, an untapped development potential of 120,000 GW / 420,000 TWh was estimated, i.e. 790 x the annual electricity consumption of France, or 54 x the Chinese consumption.

The impact of the COVID-19 sanitary crisis on offshore wind capacity development remains limited, as almost 7 GW new capacities should have been added in 2021, notably thank to the rush from RES developers to benefit from the Chinese feed-in-tariff system finishing by end-202125. Then, according to the latest GWEC’s global offshore wind report, mid to long terms development prospects are very promising with an estimated Compound Annual Growth Rate (CAGR) of new annual capacities of 29% from 2020 to 2025, and of nearly 13%/year from 2025 to 2030.

Likewise, the IRENA’s Future of Wind (2019)26 report plans an average 11.5% growth in global installed capacities from 23 GW in 2018 to 228 GW in 2030 and about 1,000 GW in 2050. Offshore wind capacities would amount to 17% of total installed capacities in 2050 (6,044 GW). Definitely, the centre of offshore wind centre of gravity would shift towards Asia, including China, India, Vietnam, Taiwan, Philippines, Indonesia, South Korea and Japan.

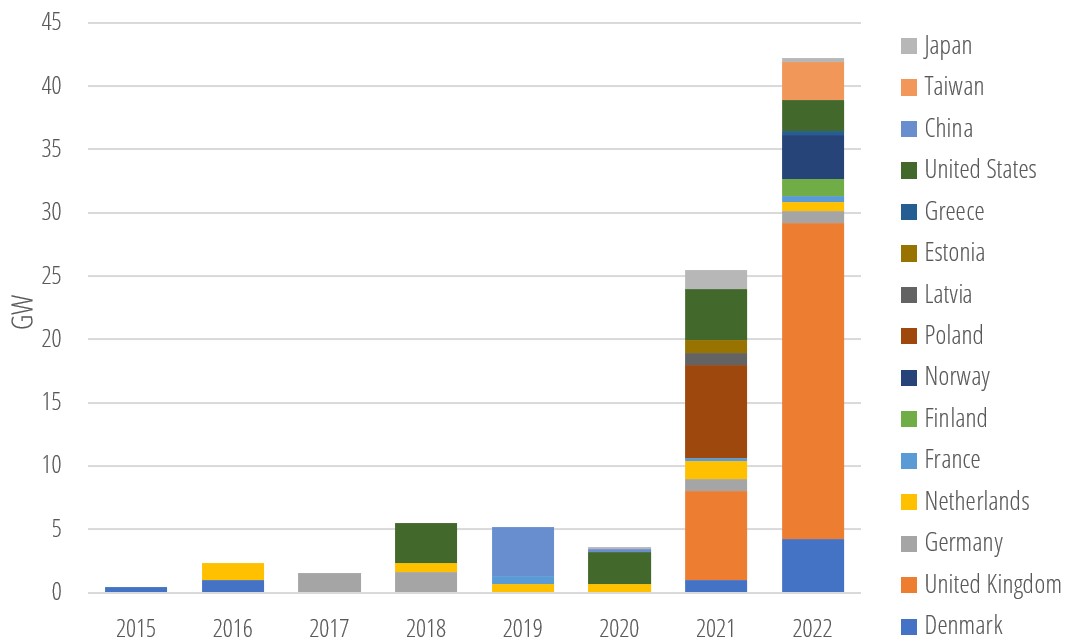

If we look at the positive prospects, solid trends are emerging. The RES auction calendar for the next years is heavy (cf. Enerdata’s Global RES Auction Monitor). Indeed, in addition to the huge offshore zone allocated by the UK in Scotland in January 2022 (25 GW) , at least 17 GW are already announced to be auctioned in 2022. Several countries will open their first auction round such as Finland (Korsnäs project), Norway (Sørlige Nordsjø II and Utsira Nord projects) and Greece. Additional auctions will probably be announced in 2022 for the next years, thus increasing the current 33 GW already planned between 2023 and 2028.

Figure 7: Concluded and planned auctioned offshore wind volume since 2015 (GW)

Source: Enerdata Power Plant Tracker, module Global RES Auction Monitor

This large project pipeline gives clear visibility for RES developers, which work on their LCOEs to drive them down thanks to enhanced financing terms (WACCs) and positive technological learning curves. The growth in turbine size combined with improved data-driven O&M enable to increase capacity factors and thus reduce LCOEs. According to the IRENA’s Future of Wind report, the average annual capacity factor is expected to progress globally from 38% in 2010 and 43% in 2018 to 43-60% in 2050. Overall, the LCOE would fall from a 50 to 90 USD2018/MWh range in 2030, to a 30 to 50 USD2018/MWh range in 2050. LCOEs are to be viewed with caution as many variables are considered in the LCOE calculation with a certain level of uncertainty.

Besides, new energy storage solutions may unlock the potential of offshore wind. Combining battery solutions with offshore wind parks (Wind+BESS) should secure grid stability and provide better power flexibility. Several RES developers are exploring this lead27 along with Wind-to-Hydrogen solutions as the new technological frontier. Indeed, hydrogen (H2) can be a decarbonised energy vector when produced by electrolysis from green electricity sources. Offshore wind could complement very well with H2 electrolysis. RES developers are currently working on pilot projects, next to existing wind parks such as offshore hydrogenation platform, e.g. the 10 GW NortH2 project led by a consortium of Shell and Groningen Seaports in the Netherlands28.

Eventually, floating offshore wind is carving out a recognised place in the offshore wind market. This promising technology may leapfrog technical difficulties in deep sea (e.g. in Japan or France). Large industrial actors such as Equinor have been investing in this technology and keep innovating with Power-to-X projects integrating floating wind platforms (cf. the world’s first commercial floating offshore wind project in 2017, the HyWind project in Scotland)29. In April 2021, a study released by the Lawrence Berkeley National Laboratory (Berkeley Lab) in Nature Energy came up with the results that offshore floating wind LCOE can drop by 40% (up to 49% for fixed bottom offshore wind)30.

Offshore wind will still face major challenges to overcome. They will remain complex projects that require lots of financial and technical resources. As the easily accessible offshore zones are selected first, technological learning curves shall compensate the induced costs to build offshore wind platforms further from the seashore and grids. We can count on the technological know-hows and financial resources of O&G transitioning to RES offshore projects, but to which speed of deployment? We can legitimately wonder what types of actors will lead the offshore wind market. The current trend favours large incumbent actors (i.e. Ørsted, Vestas, etc.), which have technical expertise, integrated supply chain and financial back-up to fulfil public auction eligibility criteria, possibly at the expense of emerging actors. Any new entrants face high market barriers and public auctions, even designed with public support schemes can be a hindrance (market concentration).

In any case, public authorities have a key responsibility to ensure the fair and efficient offshore wind development aligning the interests of all stakeholders.

Key take aways:

- COVID-19 outbreak has not held back the momentum on offshore wind technology. Projects are popping up around the world, notably in Europe, Asia, and North America.

- The technology’s key success factors rely on an alignment of stars between ambitious national renewable energy development plans, technology cost reduction and fast learning curves, improved financing access, and proven track-record of first operational wind parks facilitated by public auction procedures.

- The public RES auctions are an increasingly popular selection tool that enables to attract RES developers with market-based public support schemes (e.g. feed-in-premiums, etc.). “Zero-premium” bids have been awarded in recent offshore wind auctions, with high competition level between RES developers driving prices and costs ever lower.

- Mid- to long-term development prospects are very promising. In the short run, the project pipeline is already booming.

- Offshore wind LCOE is expected to continue plummeting in all regions, while technological innovations offer interesting horizons to address needs for grid stability and flexibility (Wind-to-X, Wind + BESS). Floating offshore wind is a promising technology that could be favoured by O&G actors and public authorities.

- Obstacles remain high and shall be overcome, starting with a non-compressible level of technical complexity with offshore projects in challenging environments.

Notes:

- Cf. Ørsted’s white paper

- Cf. Spanish Government press release

- Cf. Press release by the Federal Ministry for Economic Affairs and Climate Action

- Cf. US DOI’s press release

- Cf. UK CFD 4 documentation

- Cf. Press release by Crown Estate Scotland

- Cf. Press release on the Luxembourg and Denmark Cooperation on the offshore windmill island

- Cf. EU Offshore Renewable Energy Strategy

- Cf. DEA’s Energy Islands

- Cf. US DOE, 2021 Offshore Wind Technologies Market Report

- Cf. Beijing Declaration

- Cf. GWEC Analysis

- Cf. Vietnam Plus’ article

- Cf. Dedicated La Gan Project’s website

- Enerdata’s RES auction Monitor database

- Cf. Ørsted’s press release

- Cf. Equinor’s press release

- Cf. Crown Estate Scotland’s Press release

- Cf. RTE SDDR Chapter 6, 2019

- Cf. BEIS’ Policy Paper

- Cf. Bundesnetzagentur, 21 September 2021, press release

- CF. RVO, 14 December 2019, press release

- Cf. Nature Energy, 27 July 2020

- Cf. Offshore wind Outlook report, IEA, Imperial College, 2019

- Cf. GWEC’s analysis

- Cf. IRENA, Future of Wind Report, 2019

- Cf. Reuters: How energy storage is unlocking the power of offshore wind

- Cf. NortH2 project

- Cf. Hywind project

- Cf. Nature Energy, April 2021