See also

Market Research / Studies

Granular and exclusive insight to address the most pressing business and strategic issues.

The New Frontier of Road Transport Electrification

Get this executive brief in pdf format (free)

Electric trucks are still seen by many as non-viable, based on the belief that the performance and cost of batteries remain to the levels of 10 years ago. In this article, we explore how the significant reduction in the cost of lithium-ion batteries and their improved performance over the past few years are now enabling the electrification of road freight. Not only are electric medium and heavy-duty vehicles more energy-efficient and climate-friendly, but they are also becoming progressively more economically competitive, as the cost of batteries and electricity continues to decrease. In addition, climate and energy policies are – particularly in the West and China- pushing to decarbonise the road freight industry, further enhancing the sales of electric trucks. Based on those facts as well as the communications of major trucking companies and current market trends, we advocate that the transition to battery-electric trucks is more likely a question of “when” or “how fast” rather than a question of “if”.

An Increasing Level of Electrification of Road Transportation

Over the past few years, the electrification of road transport has been progressing in full swing. From a global market share of only 2.3 % in 2019 (with 2.1 million units), electric Light Duty Vehicles (LDVs), comprising BEVs (battery electric vehicles), PHEVs (plug-in hybrid vehicles) and FCEVs (fuel cell electric vehicles) are projected to represent more than 20% of newly sold cars in 2024 (around 17 million units), a more than 8-fold increase in terms of volumes and close to a 9-fold increase in terms of market share1. Among those sales, BEVs take the lion’s share, with approximately two thirds of the market, while PHEVs represent much of the remainder and FCEVs remain very confidential (even decreasing year by year). While the electrification of LDVs is set to continue, boosted by an increasing offer at prices that are progressively getting lower, as well as by strong incentives in major economies (IRA, 14th Five-Year Plan, Net Zero Industry Act, India’s PLI scheme), potentially leading to approx. 50% global market share by 2030 (IEA, 2024) for electric LDVs, the electrification of heavier vehicles, such as medium and heavy duty (MHD) vehicles (trucks, city buses and coaches), is still in its infancy.

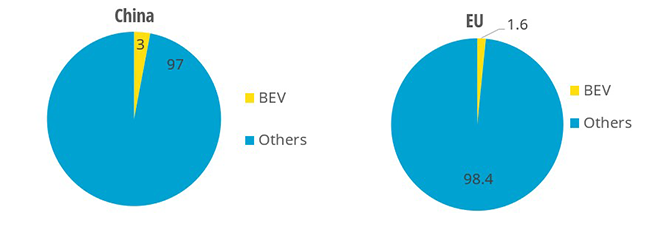

For the year 2023, global electric trucks sales increased by 35%, reaching close to 3% market share in China, with approximately 40 000 sales and above 1.5% market share in Europe, with approximately 10 000 sales. In total, global electric trucks sales amounted to 55 000 units, with only marginal volumes in the USA (less than 0.2% of local market share, although starting to grow) and in the rest of the world1.

Figure 1: Electric trucks market share (%) in China and in the EU in 2023

Source: IEA, 2024

While those levels of market share remain one order of magnitude below those of electric LDVs, dynamics are very positive, with a tripling of market share in the European Union from 2022 to 2023. Regulation will drive sustained growth in the coming years, since newly sold HDV (heavy-duty vehicles) must reduce their greenhouse gases emissions by 45%; 65% and 90% by 2030; 2035 and 2040, respectively2.

In addition to that, while the electrification of HDV was, until recently, impaired by the high cost and low availability of batteries, the situation has radically changed over the past quarters, with massive production overcapacity, mainly in China, combined by much lower cost of batteries. Conversely, compared to other heavy-duty vehicles, city buses already reach relatively high levels of electrification, accounting for more than half of new city buses in several European countries such as Belgium, Norway and Switzerland, as well as in China, while several other countries are above 25%1. Furthermore, those vehicles typically have daily travel distances that are compatible with a single overnight depot charging and can therefore be deployed before the advent of the megawatt charging standard (MCS).

Electric Trucks: Price and Competitive Advantages

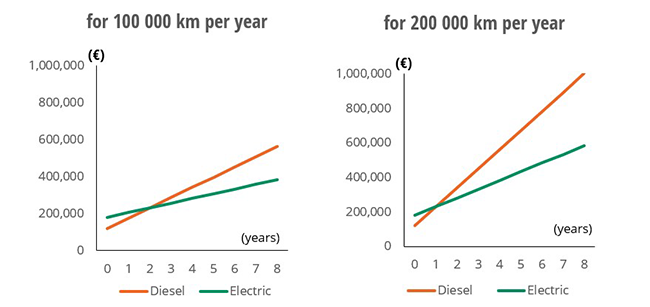

Similarly to the situation in the LDV segment, electric trucks compare themselves to traditional Diesel alternatives in terms of higher CAPEX (capital expenditure) and lower OPEX (operational expenditure) components3. The balance between the two determines which technology offers the lower TCO (total cost of ownership). Compared to diesel-powered trucks, the main reason for the higher capital expenditures for fully electric trucks is to be found in the cost of the batteries which, even if much lower than in the previous years, is still a major component in the cost of electric MHD vehicles. At the battery pack level, 2023 prices of batteries for e-buses and commercial vehicles (among which electric trucks) were at 100 USD per kWh in China. In the rest of the world, those prices were around 190 USD per kWh although decreasing very fast, with a 33% reduction from 2022 to 2023, i.e. from 285 to 190 USD per kWh4. With a hypothetical cost of 100 USD per kWh at the battery pack level (which may not be the case yet), a heavy-duty truck such as the Daimler eActros 600, with its 624 kWh of LFP batteries, would require approximately 60 000 USD of batteries, while the rest of the truck would keep approximately the same cost as for conventional diesel equipment (~ 120 000 USD). Assuming an energy cost delta of 30 cents per km in Western Europe between diesel and electric HD trucks (~25 cents per km for electric powertrains, ~55 cents per km for diesel ones), the battery price is recouped in only 200 000 kilometres, compared to a lifespan for such vehicles that is estimated to be between 1 000 000 and 2 000 000 kilometres according to various sources.

Even though the cost of financing should be considered to make more precise estimates, it appears obvious that, as the CAPEX linked to batteries is getting lower and renewable electricity is becoming more abundant, electric powertrains may progressively become a no-brainer for new MHD vehicles, when usage and infrastructure allow it. Additionally, those raw estimates do not take into account the cost of carbon linked to using a diesel vehicle burning fossil hydrocarbons, nor the cost of other negative externalities linked to diesel engines. If a consumption of 35 litres per 100 km and 2.65 kg of CO2 per litre of diesel are assumed, then over a 1 000 000 km use, a diesel heavy-duty truck would release 927 tonnes of CO2 which, even at a price of 75 euros per ton, would add close to 70 000 euros, which is more than the CAPEX linked to the battery.

Figure 2: Simplified TCO Comparison (CAPEX + Energy OPEX) for Diesel and Electric Trucks

Source: Enerdata’s Calculation, details in annex (p.12)

Even though data is still scarce on the matter, maintenance and repairs could, over time, also become much lower for electric power-trains, since those are simpler and require less operations than diesel ones. Furthermore, leading manufacturers expect their latest battery cell technologies to last well above one million miles, outlasting the lifespan of the vehicles. Even with 2023 observed prices for battery packs used in buses and commercial vehicles outside China (190 USD per kWh), the economics already start to make sense in Western Europe.

Market Players in the Electric MHD Vehicles Industry

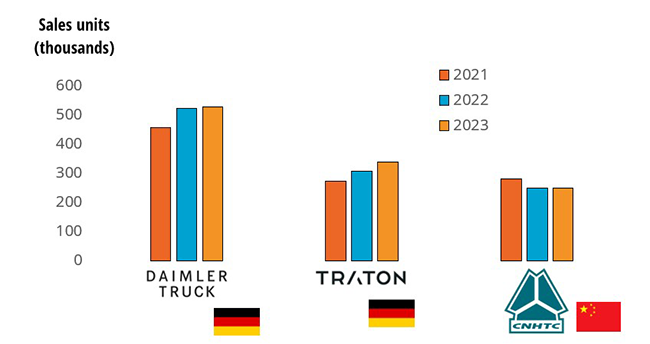

The trucking sector is a relatively consolidated industry, particularly in the Western world. Three groups dominate this sector in western countries, in terms of turnover: Daimler trucks, followed by Traton and Volvo trucks. Daimler trucks, which owns Mitsubishi/Fuso trucks, as well as US-based Freightliner, Western Star and Rizon, is the number one trucking company globally (with 540 000 units sold), as well as in the US (for class 6-8) and in Europe. Traton, 90% owned by the Volkswagen group, includes MAN and Scania for the European market, as well as Navistar for the USA. The group, which sold more than 338 000 units globally in 2023, is the second-biggest market player of the global trucking industry. First Chinese and third global truck manufacturer, Sinotrucks sold 249 000 trucks in 2022. Volvo trucks sold 144 000 trucks in 20235, among which 1977 electric trucks globally last year, and even 4,996 electric vehicles, which include buses and mining vehicles. In the trailing twelve months prior to April 2024, the group the Volvo Trucks brand reached a market share of 54% for heavy electric trucks in Europe, while its fully owned subsidiary Renault trucks reached nearly 20% (Volvo Q1 2024 earnings presentation). This resulted in the group holding a very dominant position in the segment of electric heavy-duty trucks on the old continent (combined market share of 74% on the period).

Figure 3: Global Sales Volumes of the Top 3 Truck Manufacturers - 2021, 2022, 2023

Source: Daimler Truck, Traton, Sinotrucks

In terms of megawatt charging infrastructure equipment manufacturers, as the standards are not yet finalised (except for in China), only a limited number of companies already produce those components. In Finland, Kempower introduced in 2023 its megawatt charger, with a maximum power output of 1.2 MW, which started being delivered in Q1 2024 to European customers. In Germany, ABB trialed its MW charger with a MAN truck, although the rated power was limited to 700 kW, while the prototype megawatt charger from Siemens successfully delivered a power rate of above 1 MW during its testing in April 2024. Other future suppliers of MW chargers include the Italian company Alpitronics. In North America, Tesla and ChargePoint are also developing megawatt chargers.

The Infrastructure Challenge

Depending on use cases, the necessary charging infrastructures required for the electrification of MHD vehicles can consequently vary. According to Daimler Trucks, around 60% of their customers’ long-distance journeys are less than 500 km6, which means that charging at the depot, as well as at loading and unloading sites, is sufficient in most cases. For other uses, such as international transport over long distances, an extensive fast-charging network will be necessary, especially ultra-fast charging points using the MCS. In Europe, due to the absence of such recharge infrastructure for MHD vehicles, the European Commission has adopted the AFIR (Alternative Fuel Infrastructure Regulation, Directive 2014/94/EU), setting the target of equipping major motorways of the TEN-T (trans-European network of transport) with ultra-fast charging points for MHD vehicles. Specifically, charging stations must be available every 100 km, that will have to total 1.4 MW per station by 2025 and 4.2 MW per station by 2030 (although this power can be spread over several charging points) for the core part of the TEN-T. Due to the very short amount of time remaining to reach the 2025 targets, only 15% of the network should reach the aforementioned mentioned targets by 2025, while 100% will have to comply by 2030, which is seen by industry insiders as more doable, although still challenging. The MCS of the CharIn industry association, allowing up to 3.75 MW (1 250 Volts and 3 000 Amp.) is expected to become available between 2024 and 2025 by international standards bodies such as ISO, IEC, and SAE and could become the dominant standard in Europe. In North America, it remains to be seen if this standard will dominate since Tesla is also developing its own proprietary technology. Until the MCS becomes widely available, trucks and other MHD electric vehicles can be charged up to 350 kW with the CCS standard (some trucks even feature two CCS charging ports). In China, the ChaoJi-1 standard, suitable for up to 1.2 MW, has been approved by the State Administration for Market Regulation and the National Standardisation Administration at the end of 2023, and shall become the standard in the country7.

In China, since the rate of electric trucks deployment has outpaced the development of fast charging infrastructure suitable for trucks, many customers are opting for vehicles compatible with battery swapping, which was the case for approximately half of the units sold in 2023 in the country8. Nevertheless, as battery technology improves and megawatt chargers develop, it is anticipated by some industry insiders that this solution should progressively lose market share to the benefit of more classical charging solutions.

Another alternative that has attracted interest in the past, as the cost of batteries was prohibitively high for electrifying heavy-duty transport, is the deployment of an infrastructure of overhead power cables (catenaries), which allows to benefit from the excellent operating efficiency of an electric engine without the need of capable batteries. This solution seems to have been abandoned by major trucks manufacturers as of 2024. Daimler Trucks, the global leader of the industry, who was once testing this technology, now considers that catenary trucks “are not a future-oriented solution that can be quickly implemented worldwide”9. Even though this technology is still subject to some research and development projects and could eventually find its market on very densely used motorways, no consequent orders for such trucks seem to be happening now, and the fall in battery costs combined with rising copper and aluminium prices, required for catenaries, are certainly not helping. While major market players of the industry rarely mention catenaries to electrify their products, some research projects are currently being implemented on the matter. In Europe, the country which is perceived as a leader in the development of catenary road freight is Germany, both due to its centrality in Europe, and its very dense traffic. A 5-kilometer electrified lane was built near Frankfurt in 2020, in addition to a 6-kilometer section highway in Baden-Würtemberg and another one in Schleswig-Holstein. Other neighbouring countries are also interested in the technology, such as Sweden, the UK and Denmark, but seem to be waiting for Germany to adopt a clear position before taking real commitments, while at EU level, political stakeholders have not shown a clear interest. In the coming years, it therefore remains to be seen if those experiments are considered successful and if major market players and public authorities would want to push in that direction or not.

Technological Trends

While hydrogen fuel cell trucks were once seen as the potential power-train of choice for the decarbonisation of heavy-duty vehicles, market leaders in the trucking sector, as well as some oil & gas companies, now see battery-electric propulsion taking the lion’s share, fuel-cells and hydrogen internal combustion engines being limited to rare and very intensive use cases. Behind this evolution, the collapse in battery prices, as well as the production overcapacity and the significant increase in performance (energy density, charging speed, lifespan), now allows to benefit from the advantages of direct electrification for most heavy-duty vehicles.

As is currently the case on the market of electric light duty vehicles, LFP (lithium iron phosphate) batteries also seem to be gaining traction in the electric MHD world, since they offer low cost and the possibility to scale-up more easily, due to the absence of cobalt and nickel. In addition, the possibility to fast charge such battery cells allows them to provide a long daily range if fast charging is available. Nevertheless, major trucking companies do not put all their eggs in the same basket, as most of them are also developing trucks equipped with NMC (nickel manganese cobalt) batteries in parallel, which provide longer ranges, as the class 8 Tesla Semi for instance (up to 800 km on a single charge). Additionally, trucks from the Scania brand (Traton group), would use NMC batteries locally provided by Northvolt, both companies being in Sweden.

In its 2035 market share projections for the various power trains in major markets, the International Energy Agency foresees insignificant volumes for hybrid trucks1. A reason behind those results may lie in the fact that heavy-duty trucks (as well as coaches) drive at steady speed on motorways, strongly reducing the rationale for a hybrid power-train, whose advantage is to be found in the reconversion of the kinetic energy into electricity directed to the battery when the vehicles decelerate, which can later be used to power the acceleration of the vehicle.

Prospective

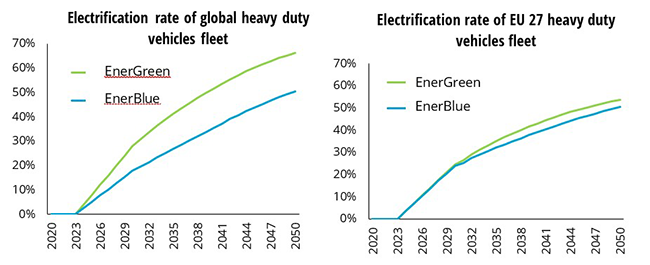

Although a consensus seems to have been reached among major market players, concerning the electrification of the industry, the long-term market share of electric MHD vehicles may not reach 100% of new sales. Daimler Trucks, sees battery-electric trucks taking around 90% of market share by the 2040’s, while other technologies (such as hydrogen) would keep some niche markets (very intensive use cases potentially being one of those).

Figure 4: Long-term projection of the share of electric vehicles in the fleet of heavy-duty vehicles in the EU27 and the world

Source: Enerdata’s calculation, based on in-house EnerGreen and EnerBlue Scenarios

Although the near-total electrification of road freight would necessarily use significant amounts of electrical power, the excellent energy efficiency of electric motors allows to reduce the final energy consumption of a truck by around two thirds (a diesel heavy duty truck burns 0.33 litres of fuel per km, equivalent to 3.3 kWh, while a battery-electric heavy-duty truck requires slightly above 1 kWh per km). The 2023 final energy consumption of trucks in the EU was 60.7 ktoe, or 707 TWh worth of fuels. The electrification of the industry would therefore require in the order of magnitude of 235 TWh of final electricity supply, at constant activity level (compared to an electricity consumption of around 2,700 TWh in 2023 and an expected consumption of around 5000 TWh by 2050 in average scenarios). Given the central importance of road freight in today’s societies, allocating 4 to 5 % of total electricity consumption could be seen as a reasonable level. Furthermore, this amount of power consumption would be much lower than with hydrogen drivetrains, due to the bypassing of the electrolysis and the oxidation steps necessary to produce and use hydrogen.

Conclusions

Not so long ago, seen as unrealistic, in the context of very expensive and scarce battery supplies, electric medium and heavy-duty vehicles not only appear feasible, but are already becoming competitive and accelerating their market share gains. While the market share of electric MHD vehicles is expected to reach 3 % in the EU in 2024 and 7% in China, the expansion is very fast, and a further doubling is anticipated for 2025, for which it is expected that the market share in China should be around 16%. Behind this impressive growth is the fact that battery costs have plummeted, and production overcapacity is accumulating due to the slowing growth of light duty electric vehicles. The much lower CAPEX for electric MHD vehicles than a few years ago, combined with high energy efficiency and falling wholesale electricity prices is allowing TCO of electric MHD vehicles to decrease progressively, which could translate into a strong economic incentive for logistics companies to switch to electric propulsion, when the infrastructure and use cases allow it. This would not only reduce emissions, but also represent a major advantage in terms of competitiveness. Even though the right products are progressively introduced to the market, from medium-duty vehicles for city delivery, to 40 tonnes, heavy-duty trucks, and prices are becoming more competitive, recharge infrastructure may represent the last missing piece of the puzzle, with a necessity to supply relatively high-power output, from a few tens of kW for overnight charging to above one MW for heavy duty fast chargers. The build out of this infrastructure requires a well anticipated and coordinated action with electricity DSOs, MHD vehicle fleet users and public authorities. If the quality of execution by all stakeholders will determine the speed at which the electrification of the trucking industry will progress, the inherent superiority of battery-electric drivetrains in terms of energy efficiency, climate, preservation of air quality, silence, comfort, as well as its ability to work with sovereign low-carbon electricity may lead to its dominance by mid-century.

KEY TAKEAWAYS

- Battery-electric trucks are becoming viable technically and economically, first in China and then in the rest of the world

- Despite a higher CAPEX than diesel trucks, electric trucks can quickly recoup their higher initial cost thanks to much lower operating costs

- Chinese trucking companies dominate the global market, due to their huge domestic market, but European companies are catching on and rapidly increasing their sales

- New megawatt charging standards are being readied in China and in the West that will allow to charge 40-tons trailers in a few minutes, but the rollout of this infrastructure is still in its infancy and will take time

- Major truck manufacturers expect battery-electric power-trains to dominate new sales by mid-century, due to their intrinsic advantages in terms of efficiency and costs.

Notes

- IEA, Global EV Outlook 2024, 2024.

- EU Commission, Reducing CO2 emissions from heavy-duty vehicles, 2024.

- NREL, Spatial and temporal analysis of the total cost of ownership for class 8 tractors and class 4 parcel delivery trucks, 2021.

- Volta Foundation, Annual battery report, 2023.

- Volvo trucks, Volvo Trucks in 2023: All-time high sales and expanded electric truck offer, 2024.

- Daimler, Roadshow presentation, 2024.

- Chademo, ChaoJi GB/T standards released: China’s next-gen ultra high-power plug officially approved, 2023.

- CNEV, Analysts expect 16 of heavy-duty trucks sold in China to be electric by 2025, 2024.

- Daimler, planned comparison with catenary trucks: Since January, the battery-electric Mercedes-Benz eActros has been driving up to 300km daily on a future catenary route, 2021.