See also

What would be the sectoral average costs to go from a baseline to a climate constraint scenario?

Get this Executive Brief in PDF format (Free)

Climate objectives and reduction of GHG emissions require significant changes in our energy systems, such as the reduction of energy consumption, the decarbonisation of energy supply, the deployment of clean technologies, etc. These profound changes in the way we consume and produce energy have massive impacts in terms of investments and energy system costs.

This analysis builds upon Enerdata’s EnerFuture scenarios to provide quantitative insights into the expected trends in energy system costs in the context of different climate ambition levels. The aim of this article is to present quantified marginal costs to abate GHG emissions, starting from a trend/baseline scenario and leading to a given ambitious scenario in terms of its climate change impact limitation.

EnerFuture scenarios

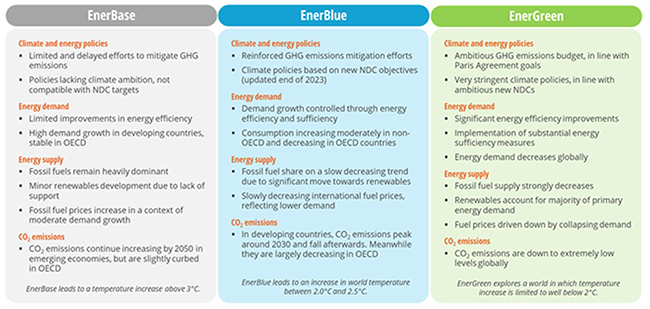

This analysis is based on our 3 energy-climate scenarios, annually updated and derived from our EnerFuture information service. These represent contrasted, plausible futures for energy systems:

- The EnerBase scenario is a Business-As-Usual trajectory, corresponding to the continuation of historical trends with limited climate ambition.

- The EnerBlue scenario accounts for stated policies and announced objectives from countries, and notably NDCs.

- The EnerGreen scenario is compatible with a temperature increase of well below 2°C, therefore aligned with the Paris agreement goals.

Figure 1 below gives a more comprehensive definition of the EnerFuture scenarios.

Figure 1: Definition of the 3 EnerFuture scenarios

Source: Enerdata - EnerFuture

As expected, the stronger efforts towards mitigation of greenhouse gas emissions in the EnerBlue and EnerGreen scenarios, compared to the EnerBase reference, imply additional abatement costs in the energy systems.

These costs are different depending on the sector, the country, and the time horizon considered. Enerdata produces and uses Marginal Abatement Costs Curves (MACCs) to quantify the abatement costs associated with emission reductions in any sector and country.

Marginal Abatements Cost Curves

In this approach, MACCs are produced for each country, for 20 emitting sectors and 6 greenhouse gases from energy and industrial activities (CO2, CH4, N2O, SF6, HFCs, and PFCs). MAC curves are produced for specific target years – in the context of this analysis: 2030, 2040 and 2050 – allowing to calculate yearly mitigation costs from today to 2050. Yearly costs between those years are estimated using interpolations.

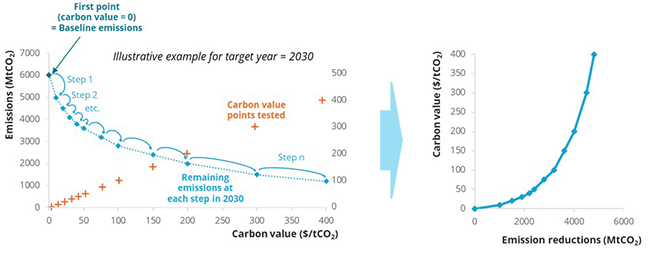

To build these sets of MACCs, the POLES-Enerdata mode1 simulates at a given year the impact of a given carbon price signal on the level of GHG emissions. The introduction of a carbon value in the model, also called carbon shadow price, impacts fossil fuel prices depending on their CO2 emissions, hence affecting the competitiveness of the different fuels in the energy system, both in final consumption sectors and in the transformation sector. The carbon value also impacts the evolution of the sectoral useful energy demand, depending on its carbon content, hence enabling to capture effects of energy efficiency on top of fuel switching. As a consequence, the system becomes less carbon intensive as the carbon price increases. Starting from a baseline which is a “zero carbon price” situation, abatements are quantified for a given target year, for each sector and country. Conducting a sensitivity analysis with multiple carbon price levels allows to recursively build a complete curve, as illustrated in figure 2.

Figure 2 – Methodology for the derivation of Marginal Abatement Cost Curves from the POLES model for a specific region

Source: Enerdata - MACCs

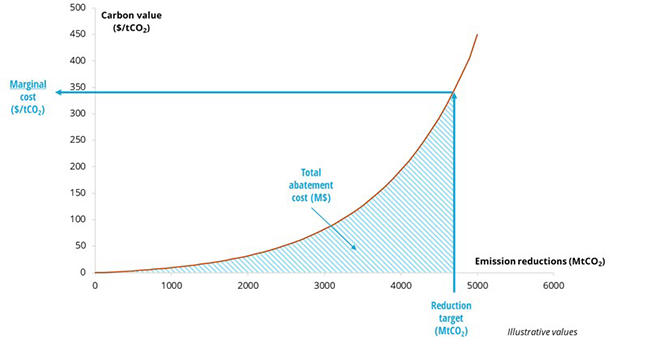

For a specific region, the marginal abatement cost for CO2 emissions corresponds to the unit cost of the latest action to be undertaken in order to comply with a given reduction target, as represented in figure 3. The total abatement cost, i.e. the total cost needed to reach the overall reduction target, is calculated as the area under the MAC curve up to this target point.

Figure 3 – From MACCs from POLES-Enerdata to marginal and total abatement costs

Source: Enerdata - MACCs

In this executive brief, we assess the average sectoral abatement cost for selected regions to transition from the EnerBase scenario (baseline scenario used for this MACCs analysis) to the EnerBlue and EnerGreen scenarios, respectively.

Cases study and results

This analysis focuses first on the European Union, complemented by country-specific results for Czechia, along with an example of a Southern country with specific results for Indonesia.

The European Union landscape

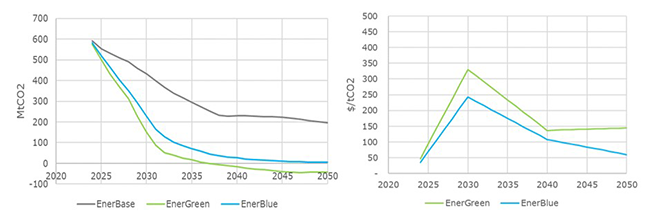

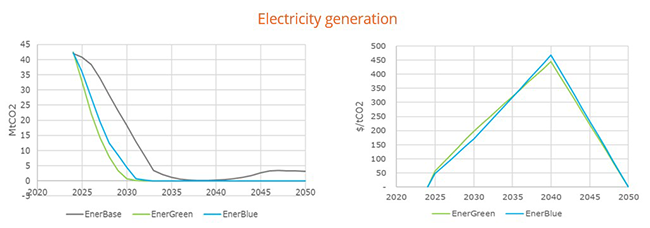

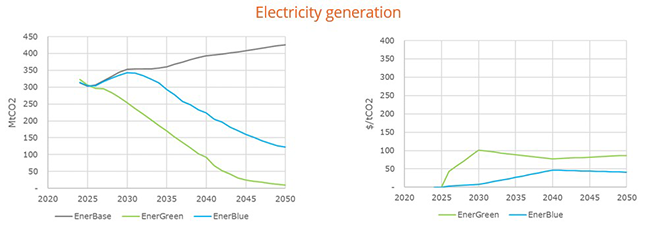

Figure 4 (left) shows the CO2 emissions from electricity generation in the 3 scenarios considered. As expected, emissions are lower in EnerBlue and even lower in EnerGreen compared to EnerBase. A set of MACCs has been built starting from EnerBase, to derive the yearly average abatement costs required (right of the figure) to reach the emission levels of EnerBlue and EnerGreen, respectively.

Figure 4 – Emissions and average abatement cost for electricity generation in the EU

Source: Enerdata - MACCs

It is worth noticing that the average abatement cost reaches a peak in 2030, corresponding to ambitious objectives in emissions reduction for electricity generation in both EnerBlue and even more in EnerGreen by 2030. This peak of average abatement cost reflects a strong need for abatements to be achieved in a constrained short-term period, with notably massive investments to be realised in renewable energy sector. After this, marginal costs decrease until 2050, but still remaining positive to reach additional abatements in the sector, while the initial investments done by 2030 pay off in the longer run.

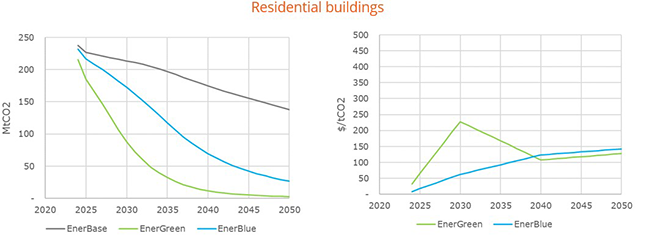

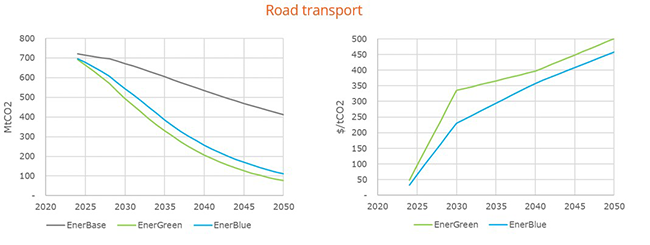

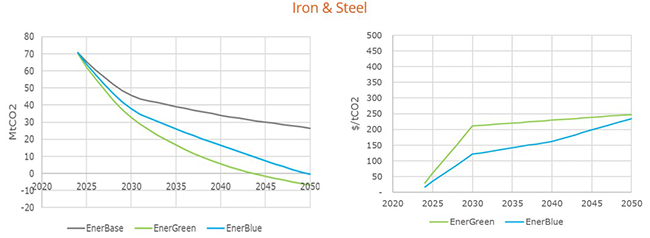

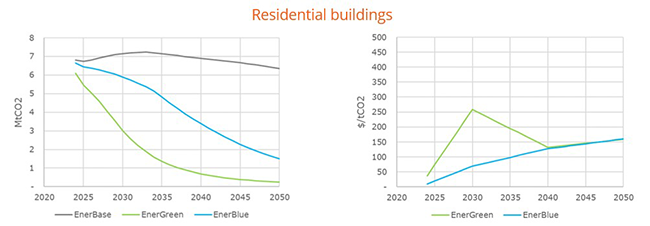

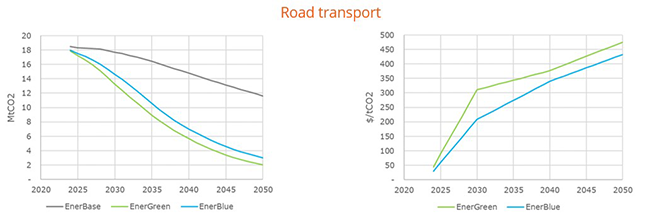

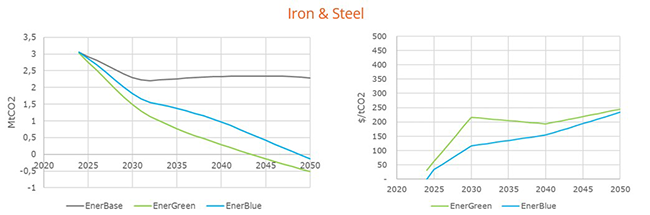

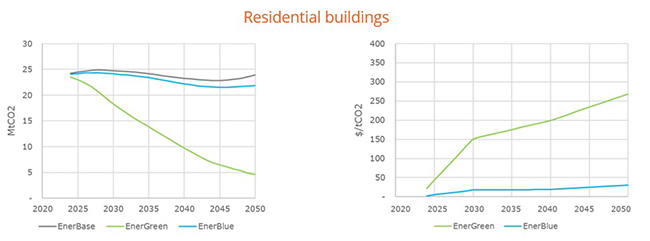

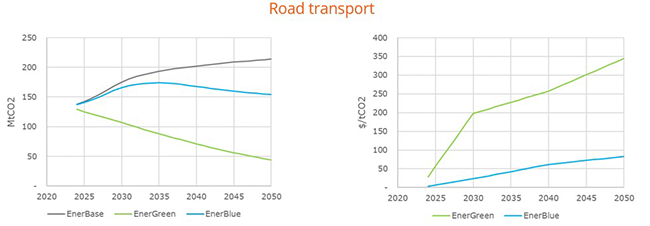

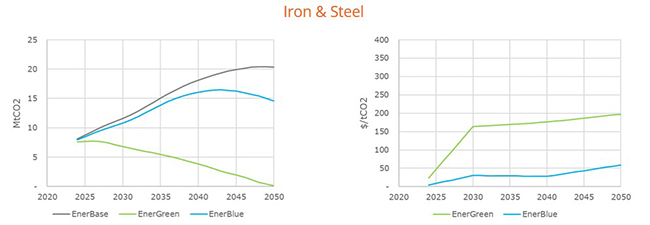

Figure 5 shows similar graphs for residential buildings, the road transport sector, and the iron and steel industry.

Figure 5 – Emissions and average abatement costs for residential buildings, the road transport sector and the iron & steel industry in the EU

Source: Enerdata - MACCs

In those sectors, the shape of the curves are relatively different. In residential buildings, transitioning from EnerBase to EnerBlue requires a more linear additional cost over years in all sectors represented, even if the level of cost is very different. On the other hand, the transition from EnerBase to EnerGreen requires a high investment in the short term, and then a lower cost than for EnerBlue because some efforts are already done (e.g. energy efficiency improvements and a faster diffusion of heats pumps) and the targets for later years would end up being less costly per unit of CO2 removed.

The road transport sector and the iron & steel industry show an average abatement cost trajectory which is comparable to the EnerBase à EnerBlue pathway, with a slightly higher cost due to more ambitious sectoral emission reduction targets.

- Country example: Czechia

To put the EU analysis into a national perspective, Figure 6 shows the same graphs for Czechia with sectoral emissions on the left and average abatement cost trajectories on the right.

Figure 6 – Czechia example: emissions and average abatement cost for electricity generation, residential buildings, the road transport sector and the iron & steel industry

Source: Enerdata - MACCs

While Czechia follows similar trends as those observed at EU level, some differences are noticeable. Specifically in the power generation sector, the average abatement cost trajectories show a peak occurring later than in the EU: in Czechia, the EnerBase scenario already accounts for a deep decarbonisation of the power supply, due to the ambitious coal phase-out planned by 2033. Hence, emission reductions after this year, and in particular around 2040, correspond to particularly costly measures allowing to reach near-zero emissions in the sector.

- Different trends in a South-East Asian country: Indonesia

The same graphs and analysis are displayed in figure 7 for another region of the world: Indonesia.

Figure 7 – Indonesia example: emissions and average abatement cost for electricity generation, residential buildings, the road transport sector and the iron & steel industry

Source: Enerdata - MACCs

For Indonesia, the EnerBlue scenario is significantly less ambitious than the EnerGreen scenario, in contrast to the EU and its Member-states. In this context, the average marginal cost between EnerBase and EnerBlue is significantly lower than for European economies.

However, reaching a well below 2°C world also requires relatively high abatement costs in developing countries, which are necessary to decarbonise all sectors, as illustrated by the abatement volumes required and the associated costs for a transition from EnerBase to EnerGreen.

Conclusion

The present analysis explores the underlying abatement costs of three contrasted energy-climate scenarios. Our findings show that abatements required to transition to a NDC scenario or to a below 2°C-compatible scenario can significantly differ depending on the region, sector, and time horizon considered.

The global POLES-Enerdata model allows to produce MACCs for more than 50 individual countries in the world and 20 sectors, offering a large potential to assess abatement costs of the energy transition in a large set of contexts and geographical areas.

Key takeaways

- Marginal Abatement Costs Curves allow to quantify the average abatement cost required to reach a climate ambitious scenario, per sector and per country.

- In Northern countries, costs tend to peak around 2030 in the electricity generation sector, due to the large short-term efforts required.

- In contrast, other sectors such as road transport and the iron and steel industry have mostly an increasing average reduction cost over time, in all regions.

- Additional research and analysis can be performed with the underlying POLES-Enerdata model, e.g. to dive deeper into decarbonisation costs in a given country, sector, and for various time horizons.

Notes:

1This is an energy-economy-environment model of the global energy system, covering 66 countries and regions, with dedicating modelling of the individual end-use sectors, energy supply, prices and GHG emissions. The POLES model has been initially developed by IEPE (Institute for Economics and Energy Policy), now GAEL lab (Grenoble Applied Economics Lab)