Get this executive brief in pdf format

What is the magnitude of foreign influence in the European electricity sector? What are the strategies of large players (China, Russia and the United States)? Where have they invested, in which kind of assets? This article offers an overview and details the latest moves of key companies.

Energy policy is a historic pillar of European integration (ECSC, EURATOM). But the introduction at Community level over the last two decades of legislation aimed at improving competition between electricity sector operators through the gradual liberalisation of electricity markets and ending state or regional monopolies has in practice led to an increasing involvement of non-Community players, sometimes supported by states. Moreover, for the past ten years, the European institutions, considering themselves to have a global mission to combat climate change, have endeavoured, through their directives, to promote a global energy transition.

These effects, combined with the demand shocks resulting from the 2008 financial crisis, have significantly reduced the market capitalisation of Europe's large utilities and their investment capacity. On some days, high levels of renewable electricity production lead markets to record negative prices, particularly in Germany, to protect grid stability. This phenomenon is an inevitable consequence of the massive subsidies paid to renewable energies, which also benefit from priority access to the networks. It has strongly destabilised the economic balance of utilities. And led to the security of electricity supply in Europe becoming more and more precarious. Moreover, European institutions, especially the European Commission, long held the view that their mandate was not to create European industrial champions but to ensure consumer protection, though early European treaties aimed for the former. In mid-2019, the European Parliament finally called for protective measures to be taken, particularly in the field of energy infrastructure.

In this context, investors from outside the EU borders have been playing a growing role. In this Executive Brief, we will take a closer look at Chinese, Russian and American involvement in the European electricity sector.

The Chinese energy strategy

A transition from oil and gas to electricity

Since the mid-2000s, China has embarked on a policy of massive investment around the world, particularly in the field of energy. Out of nearly $1.8 trillion invested between 2005 and 2017, 37% has been invested in the energy sector. Initially focused on oil and gas, investments gradually shifted, starting in 2010, to production systems and power grids. China's objective, between now and the centenary of the 1949 revolution, is to reduce its geopolitical dependence on hydrocarbons, in particular with regards to the countries of the Persian Gulf, while creating a "clean" energy system free of the disadvantages associated with the use of fossils.

China's approach is now structured around the Belt and Road Initiative (BRI), which includes a specifically energy-related version: the Global Energy Interconnection Initiative (GEII). This is a "national strategy", a personal priority of President Xi Jinping, which aims to create the first global electricity grid, using a technology that China has fully mastered, UHV (Hyper High Voltage) power transmission networks, and investing in the electricity grids of more than 80 countries.

The implementation of the GEII must be carried out at two levels: substituting conventional energy sources in China by electrical energy, and gain access to external electricity resources as it will not be able to meet all of this future increase in electricity demand on its own. The rationale of the GEII requires the gradual takeover of utilities in charge of electricity networks in developed countries and a dominant position in the financing of networks and equipment in emerging countries.

GEII successes in European electricity networks

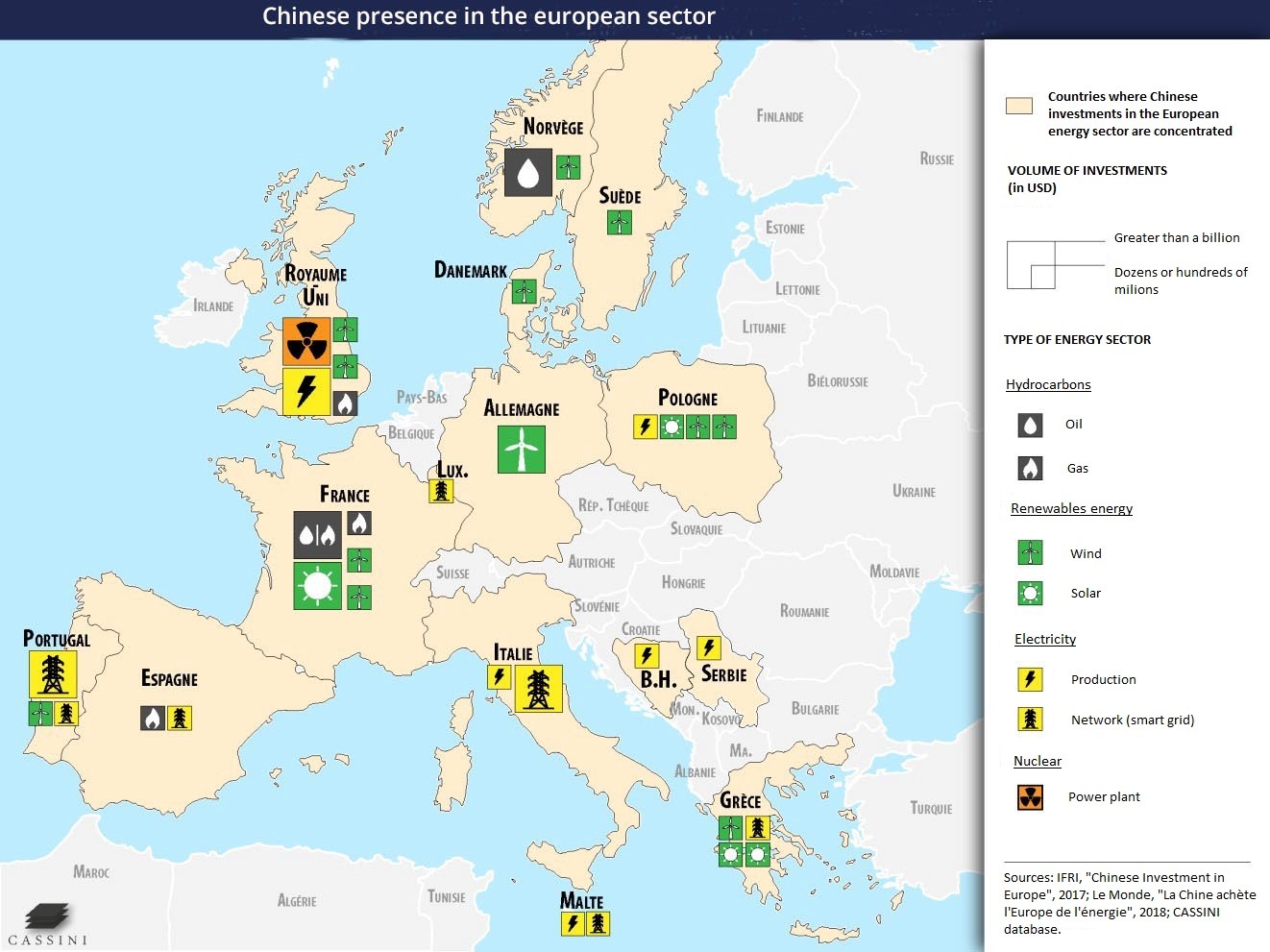

In total, between 2013 and the first quarter of 2018, Chinese electricity operators invested $123 billion in foreign power grids. Adding the financing linked to the energy sector but coming from financial institutions or other Chinese players, the total amount over the period amounts to $452 billion. Although Europe does not receive the largest share of these investments, it nevertheless ranks third, and Chinese players are currently active in 11 European countries. It should be noted that not all Chinese ventures succeeded, as some coveted assets could not be acquired due to the opposition of local public authorities: for instance, the Spanish TSO REE in 2012, the Belgian distributor Eandis in 2016, or more recently the German TSO 50 Hertz and Energias de Portugal, the latter of which included American involvement.

Figure 1: Overview of Chinese projects and investments in Europe

Source: Cassini

Chinese technological and industrial expertise

If the realisation of the GEII requires networks, it also implies a thorough mastery of many electrical technologies. China, in the space of a few years, and taking advantage of the opportunity offered by the Paris Agreement of 2015, has become the world's largest producer, exporter and installer of solar panels, wind turbines, battery storage systems and their recycling and electric vehicles, and can thus establish itself as a champion of the energy transition. Moreover, China has also been the world leader in the development of nuclear and hydraulic energy, energy efficiency equipment and the most active player in the takeover of strategic raw materials such as lithium and rare earths.

A photovoltaic industry dominated by China

In principle, Chinese manufacturers in the sector now control more than 70% of the world market. Nine Chinese companies are among the world's top ten photovoltaic module manufacturers, led by Jinko Solar and Trina Solar.

The European Commission has ruled to discontinue the anti-dumping measures affecting imports of Chinese solar panels that had been in place for 5 years. This measure probably means the end of the European industry in this field, especially as the Chinese moratorium on solar installations in China has led to a massive Chinese supply at dumped prices.

Wind power industry, first onshore and eventually offshore

For the first time in the second half of 2019, Chinese wind energy companies reached more than half of the onshore market, with 52% of orders booked worldwide. Among the 10 leading wind turbine manufacturers in the world, six are Chinese groups. In addition, the main European operators, MHI Vestas and Siemens Gamesa RE are beginning to talk about the gradual relocation of their factories from Europe to Asia, with job cuts in Europe.

As regards offshore, China, which was slightly behind MHI Vestas, GE and Siemens Gamesa, is beginning to catch up with them, both in terms of turbine power and market share. Experts predict that China will be dominant in this sector by the end of the next decade at the latest, or as soon as next year.

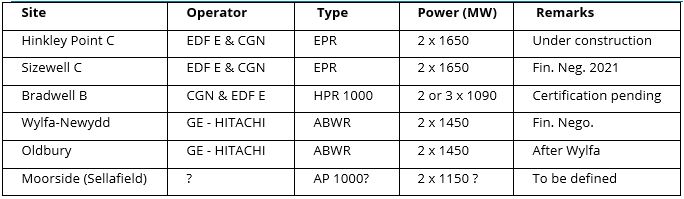

Nuclear sector: starting with the UK

China's nuclear programme is now opening up internationally, as China is no longer content to be a co-investor, as it was for HPC or SWC alongside EDF (33.5% and 20.0% respectively). For instance, in October 2016, CGN filed a request for validation of the generic design of the Hualong One reactor in the United Kingdom (completion of the process is scheduled for the end of 2021). The use of this model is notably planned by CGN and EDF for the Bradwell project. And China’s nuclear projects in the UK are multiplying.

Table 1: Chinese nuclear projects in the UK

Source: Enerdata

But the United Kingdom is no longer a unique case for Chinese nuclear power internationally; the country is now investing in other European countries.

Energy efficiency

In many areas, particularly in heating and cooling equipment, Chinese producers dominate the market, especially for heat pumps, mobile radiators and air conditioners. In fact, China already has more than 600 million air conditioners, five times more than Europe as a whole.

Storage

This is of course key to the development of the electric vehicle, but there is more at stake than that. Power storage is also a major challenge for the electrical systems of the future, characterized by the massive presence of intermittent renewable electricity. China accounts for 61% of the world battery market, compared with 21% for Japan/South Korea (combined) and less than 10% for the United States. China alone produces 65.7% of the anodes, 64.3% of the electrolytes, 44.8% of the separators and 39% of the cathodes.

China also has total market dominance in the recycling of lithium-ion batteries. Last year, China recycled around 67,000 tonnes of lithium-ion batteries, 69% of all stock available for recycling worldwide, and a further 18,000 tonnes were recycled in South Korea, mainly for the Chinese market. China aims to take a growing share in this sector to increase supply to its battery production sector.

Electric vehicles (EV)

For Europe, the rapid switch to EVs means the loss of the overwhelming advantage it had in the field of internal combustion engines against the USA and China, whereas the latter has a strong expertise in electric mobility.

Moreover, Chinese producers are moving closer to Europe. One of the Chinese leaders in the production of battery cells, CATL, is going to build a factory in Germany, which should eventually become one of the most important European sites in this field. BMW, on this occasion, noted that "CATL has the know-how to mass produce, know-how that does not yet exist in Europe", and has already signed a €4 billion contract with CATL, while specifying that it wants to retain control of the cobalt supply that it will make available to the supplier. Similarly, BYD will set up an EV production plant in Tangiers for Europe.

European manufacturers currently pay Chinese suppliers between €4000 and €7,000 for the batteries equipping their vehicles, with Chinese manufacturers thus capturing a major share of the added value per vehicle.

In addition to individual electric vehicles, China dominates the heavy electric vehicle segment with, in particular, 98% of the world e-bus market.

Supremacy over raw materials

The development of EVs and renewable energies implies securing the supply of strategic raw materials. Indeed, based on current technologies and according to the IEA's EV30 scenario, a global vehicle fleet of 130 million electric vehicles would increase demand for strategic metals from 200 000 tonnes per year in 2018 to 2 200 000 tonnes in 2030, i.e. by more than 1000%. China has already taken many options on these strategic metals, particularly rare earths. In 2019, the European Commission warned that as Europe moves away from fossil fuels to clean energy, it must avoid falling into another trap linked to raw materials and technological dependence.

But last September, Zijin Mining Group, China's third largest copper producer (and leading gold producer) bought the Bor copper mine, one of the world's best copper deposits, from the Serbian group RTB Bor for $1.46bn. It also bought for $1.66 billion the Canadian group Nevsun, which was prospecting on this deposit. Copper is a key element in the development of electric vehicles. This operation is part of the Belt and Road Initiative project and is part of a series of infrastructure investments in the Balkans, with in particular the construction of a railway line linking Serbia to the port of Piraeus, which was bought out for 67% in 2016 by the Cosco group, the world's third largest container ship owner, with the signing of a concession contract and an investment commitment of €350M.

China is in an unquestionable leadership position, with the temporary exception of the offshore wind energy sector. Moreover, in the three truly key sectors of the energy transition, namely solar energy, electricity storage and access to raw materials, its domination appears overwhelming compared to Europe's position.

Despite some recent setbacks, due to Europe's belated awareness of the risk of losing control of key elements of its electricity system, China has been able to implement important elements of Phase I of the GEII, and is therefore preparing to move into the second phase. Therefore, if the EU wants to maintain its independence in the evolution of its electricity system, which is a major strategic infrastructure, it needs to put in place safeguard processes. This could take the form of:

- Supervision of asset acquisitions by Entso-E (similar to the US FERC),

- A system of specific voting shares at the level of European TSO shareholders,

- Very close monitoring of the development of future interconnections linking the EU to the rest of the world.

Russia’s focus: nuclear energy

Contrary to Chinese ambitions, the Russian strategy is much more limited in scope, both in terms of resources and geography.

Russia is of course using oil and especially gas levers as a priority, which implies a frontal conflict with the American administration on gas, since the emergence of the huge American shale gas production and the development of a significant LNG export capacity.

In the electricity sector, Russia is focusing on nuclear, a long-standing and active industry. The country is taking advantage of the withdrawal of American companies on the subject, France's technological difficulties and a Chinese discretion that is perhaps only temporary.

Ground strategy

Eastern Europe, and particularly the Visegrad Group, appear to be Russia's natural market. Historically, Russia has supplied this zone with VVER technologies and fuel and has a perfect command of the networks of influence (industry personnel and certain political leaders having been trained in Moscow). Moreover, Russia is, like China, very actively funding projects in emerging markets. However, the financial resources of the Russian State are not as massive as those of China, and projects have already failed for lack of capital (in Slovakia, Ukraine, Argentina).

Russia, the world's fourth largest producer of nuclear electricity, has a state-of-the-art industrial complex and know-how that is exported internationally. The industry is under the leadership of Rosatom State Corporation, which has the largest portfolio of international projects in the sector as well as a competitive flagship model and is in the process of diversifying its portfolio.

Geographically, Russia's nuclear stranglehold is clearly exerted over almost all of eastern Europe and neighbouring areas such as Belarus and Turkey. Technically, however, this hold is also based on major partnerships with French players in the sector. It should be noted that there is no simultaneous presence of Chinese and Russian investments in any European country (see Map Part I).

Beginning of diversification

In 2018, Rosatom created a €40 million venture capital fund to invest in "artificial intelligence, renewable and smart energy, 3D printing, new materials and devices for smart and energy-efficient cities". This proves that Russia probably intends to develop other fields of influence around the nuclear issue, but for the moment the means implemented appear rather modest.

To sum up, Russia's essentially nuclear power approach complements very well the influence exerted by Gazprom over the whole of Eastern Europe. It can take advantage of these countries' strong enthusiasm for this energy, which represents a potential strategic break with Western Europe, which is showing itself to be cautious, even hostile, towards nuclear power generation.

The American digital approach: arrival of the GAFAM

In Europe, the American government is infinitely more discreet on the subject of electricity than on the subject of gas. In the past two years, the Secretary of State has several times stressed the importance of having an independent energy policy, with remarks aimed in particular at Eastern European states and Russia’s influence. But apart from this, the European electric field is left largely to the initiative of private American players, and in particular the GAFAMs (Google, Amazon, Facebook, Apple, Microsoft).

The basic mechanism

The "green" label has become for many companies, particularly "tech" companies, an image issue for the general public, and particularly for their core target group, the younger generations. These companies are therefore positioning themselves as players in the energy transition, by highlighting their social responsibility. Beyond “green” energy, the search for independence and long-term cost security is also a major trend, which is manifested by the search for self-consumption/self-production. Finally, in most cases, corporate Power Purchase Agreements (PPAs) offer a long-term financial guarantee to the project investor, who can thus protect himself against regulatory fluctuations.

On March 28, 2019, more than 300 "green-oriented" American companies, including Google, General Motors, Citigroup, Walmart and Disney, transformed the REBA (Renewable Energy Buyers Alliance), a non-profit organization, into a lobby group in its own right to advance the cause of climate change and solve the many problems that these companies face in their race to become "green". As part of this process, these players could reshape energy markets. REBA's primary objective is to increase the ability of companies to choose clean electricity, which means seeking better contracts, disseminating best practices and opening electricity markets to more competition. REBA aims to bring 60 GW of new green energy online by 2025.

The development of "green" PPA must therefore be seen as an irreversible underlying trend, which risks having an impact and profoundly changing electricity markets in the long term.

Concrete operations

It is in this context that the GAFAMs are beginning to influence the way the European electricity market operates. At the global level, the GAFAM have secured their supplies of RE, particularly wind power (except for Apple, which has opted for solar power), with nearly 5 GW of PPA negotiated in 2017, and Google has set a target of 100% RE supply by 2017 (with 1.1 GW, making it the leading American buyer).

This approach is now becoming commonplace, with many 20-year contracts (or even 25 or 30 years for equipment to be built). In the first half of 2018, 7.2 GW was signed, compared with 5.4 GW signed for the whole of 2017. Europe is moving in this direction with 1.6 GW compared to 1.1 GW in 2017. While the European approach remains dominated by the metals (aluminium, steel) and paper sectors, it is now opening up to pharmaceutical laboratories, biotechs, telecoms or car manufacturers (Mercedes), while the French transport companies SNCF, RATP and ADP have launched their first consultations.

- Microsoft

Microsoft was faced with the problem posed by the consumption of datacenters, which are estimated to account for a third of the digital sector’s energy consumption. Based on an annual growth of 7% in the sector by 2030, it has decided to implement a proactive policy by moving from a 50% supply of renewable energy in 2018 to 60% by the end of 2019 and to 70% by 2030, also using AI to streamline internal processes. To achieve its objectives, Microsoft is relying on an internal carbon tax of $15/t, created in 2012, which aims to make the group's divisions accountable for the target and to mobilize financing.

Thus, on 22 May 2019, Microsoft announced the conclusion of a PPA with Eneco, covering 90 MW of the 731.5 MW of the Dutch Borssele 3 and 4 wind farms, to supply its data centres for 15 years. It is Microsoft's second largest PPP in the Netherlands and 14th worldwide (1.5 GW). Both parks are scheduled to be completed in 2021.

Earlier in 2019, Microsoft chose Sweden as the location for a series of "sustainable" data centres, which will be powered 100% by renewable energy from local projects.

For its part, on 20 September 2019, Google announced its intention to invest €3bn in Europe in new data centres by 2021. Half of the energy supply for these centres will be provided by 10 new renewable energy projects, one offshore project in Belgium, five solar projects in Denmark, two wind projects in Sweden and two wind projects in Finland. In all, Google announced 18 new PPPs totalling 1.6 GW to increase its renewable supply (solar and wind) by more than 40% to 5.5 GW.

In this context, on September 30, 2019, Google announced that it had contracted the entire production of the Björkvattnet onshore wind farm as part of its supply strategy. The Swedish deal was negotiated with GE Renewable Energy, which supports the project developers and provides the turbines for 175 MW, GE 5.3 MW Cypress models which are expected to be commercially operational in 2020. The output of the site will be used exclusively by Google's regional data centres.

Google's chief operating officer said that the company is trying to develop renewable capacity where it is used. Google's European purchases of wind and solar power in Europe are a perfect fit with its data centres in Ireland, Belgium, the Netherlands, Finland and Denmark. Data centres require huge volumes of energy, much of which is used for cooling. Scandinavia is a big winner in the data centre market with low ambient temperatures and high availability of renewable energy, which is very attractive for Google, Microsoft and other major operators.

- Other active companies

Amazon joined Google in announcing a major commitment on 17 September 2019, namely a plan to achieve 100% renewable energy by 2030 and net zero carbon by 2040.

Facebook has also invested nearly $1 billion in two data centers in Luleå, Sweden to prepare for their renewable energy supply.

The prospects for increased demand from technology companies are clear: Cisco estimates the average annual growth of data centres in Western Europe at 17% from 2016 to 2021, mostly in Scandinavia.

And beyond technology companies, other US industries are getting involved: for instance, the aluminium group Alcoa has signed more than 800 MW of PPAs in Norway.

Long-term risks

Even if all these operations remain modest in terms of capacity in relation to the total capacity of the European power system, this form of "takeover bid" for renewable projects developed in Europe is likely to create, in the long term, an imbalance on the wholesale markets, problems of stability in the balance of the European power system, and the impossibility for less powerful players to access this type of energy resource. We could see a form of confiscation of European renewable resources by the GAFAMs.

These practices could give rise to the risk of economic overbidding, with some Member States seeking to attract American investors by using their energy advantages to the detriment of others.

Above all, however, this could ultimately weigh on the States' electricity policy by influencing the investment decisions of utilities, as can already be seen in the United States, where Google has invited itself into the decision-making bodies of certain regional TSOs. And in the end, the task of European TSOs could be made more complex by focusing certain generation capacities on specific consumers.

Summary:

- China has been massively investing in the European electricity sector since the 2000s, as part of its global strategy to create the first global electricity grid.

- China is investing in many technologies (photovoltaic, wind, nuclear, storage, electric vehicles, raw materials used in renewable energy technologies…) and its technological expertise has made it a key actor, which will play an always bigger role in the future.

- Russia is focusing on its nuclear strength, especially in its traditional area of influence (Central and Eastern Europe).

- US investments mostly come from the private sector, particularly its most successful tech companies, looking for opportunities to invest in “green” electricity.

This Executive Brief stems from an analysis by Enerdata, the French Institute for International and Strategic Affairs (IRIS) and Cassini for the French Ministry of Defence (full report available in French here).