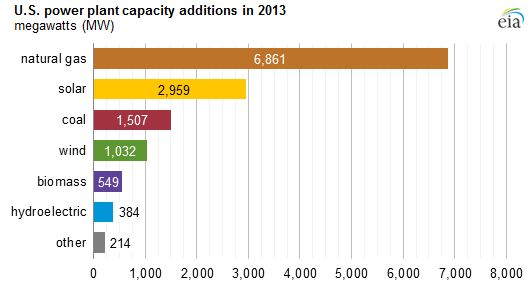

In 2013, more than 13.5 GW of new power generating capacities were added in the United States, of which about 51% came from gas. A total of 6,861 MW of gas-fired capacities were installed during the year, which is 26% less than in 2012 (9,210 MW). The capacity additions came nearly equally from combustion turbine peaker plants, which generally run only during the highest peak-demand hours of the year, and combined-cycle plants, which provide intermediate and baseload power. Solar photovoltaic added 2,193 MW of capacity in 2013, continuing the trend of the past few years of strong growth, helped in part by falling technology costs as well as aggressive state renewable portfolio standards (RPS) and continued federal investment tax credits. Two coal plants, initially expected in 2011-12, accounted for all of the coal capacity added in 2013: the 937 MW Sandy Creek plant in Texas and the 571 MW Edwardsport integrated gasification combined-cycle (IGCC) plant in Indiana. Wind capacity additions (1,032 MW) dropped sharply in 2013 to less than 10% of the capacity added in 2012 (12,885 MW). This was a widely expected result of the rush to complete wind projects in 2012 to qualify for the federal production tax credit. Almost half of all capacity added in 2013 was located in California (nearly 60% of the gas fired additions, 75% of solar additions and a significant part of wind additions.

Source: EIA

Interested in Global Energy Research?

Enerdata's premium online information service provides up-to-date market reports on 110+ countries. The reports include valuable market data and analysis as well as a daily newsfeed, curated by our energy analysts, on the oil, gas, coal and power markets.

This user-friendly tool gives you the essentials about the domestic markets of your concern, including market structure, organisation, actors, projects and business perspectives.