Request the Publication (FREE)

The world’s largest power generation companies (GenCos) play a critical role in the energy transition. However, for investors and policymakers, distinguishing between ambitious corporate pledges and on-the-ground reality remains a significant challenge.

How do global utility strategies truly stack up against climate targets? Leveraging our Power Plant Tracker database, our experts have consolidated data from the top 40 GenCos globally. By drilling down into subsidiary-level data, they provide a unique perspective on the true progress towards the energy transition.

The global power landscape: Chinese dominance and the “Big 5”

The scale of global power generation is increasingly concentrated in Asia. Currently, the Chinese "Big 5" (CEIC, China Huaneng, China Datang, China Huadian, and SPIC) represent half of the total installed capacity of the 40 largest GenCos analysed.

Backed by the Central Government, these giants have reached unprecedented levels of new renewable energy implementation. This surge is driven by national pledges to ensure that renewables account for at least 50% of all new capacity additions by 2025.

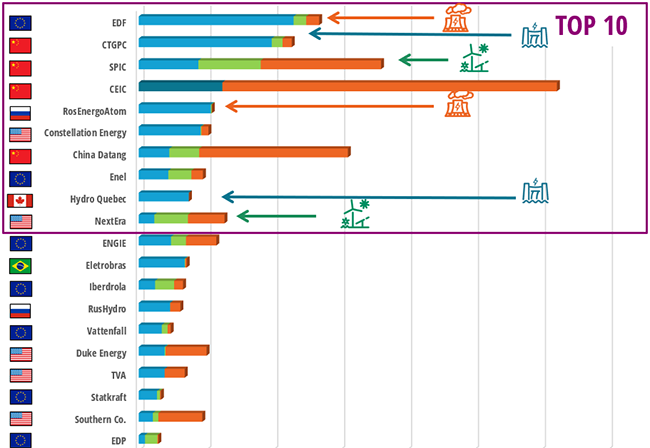

World ranking of zero direct CO2 emissions producers in 2024 (TWh)

Source: Enerdata – Power Plant Tracker

Decarbonisation trends: thermal decommissioning and the Carbon Factor

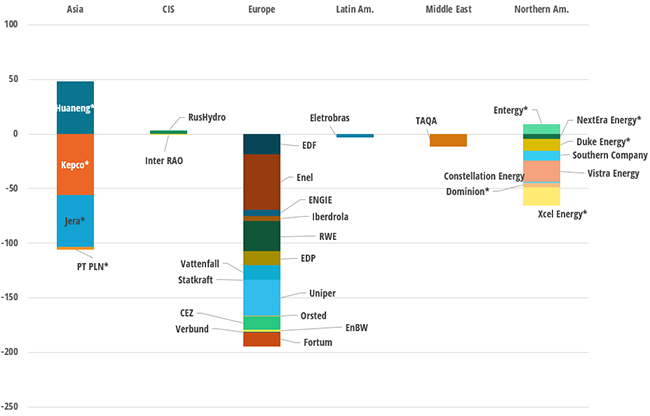

While Asia leads in capacity volume, the structural shift away from fossil fuels is most visible in Europe and North America. Low-carbon strategies implemented since the 2010s, reinforced by the EU ETS schemes and rising CO2 costs, serve as the primary drivers for emission reductions.

To accurately measure this transition, we monitor the Carbon Factor (gCO2/kWh) alongside absolute emissions (MtCO2). This intensity metric allows for a fair comparison between utility giants, revealing which companies are successfully "greening" their production mix regardless of their total size.

Evolution of CO2 emissions 2019-2025 (MtCO2)

Source: Enerdata – Power Plant Tracker

The granularity gap: why drilling-down into subsidiary-level is crucial

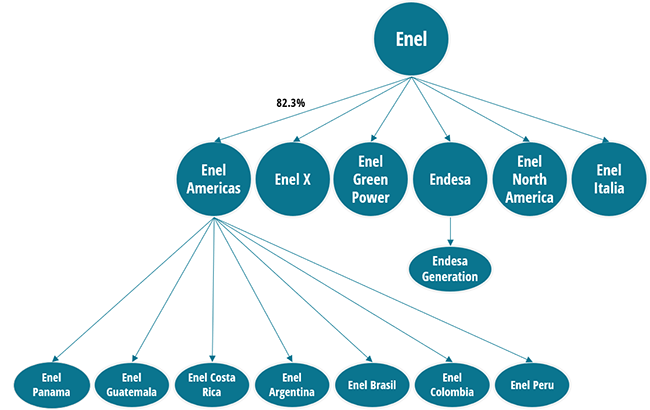

To perform a granular strategic analysis, it requires looking beyond group’s consolidated annual report. Detailing power plant ownership at the subsidiary level is crucial for understanding true market share and actual operational strategies.

Non-exhaustive overview of Enel’s Subsidiaries

Source: Enerdata – Power Plant Tracker

Using our case study of Enel’s Subsidiaries, our experts demonstrate why a deep-dive approach is essential:

- Understanding local realities: A global utility may appear as one of many players at a group level, but its subsidiaries often hold dominant or monopolistic positions in specific local markets.

- Mapping ownership complexity: Modern utilities operate through a complex web of Special Purpose Vehicles, asset managers, and autoproducers. Distinguishing between these is vital to identify who holds true operational control.

- Assessing market concentration: Granular data reveals the true impact of corporate decisions on regional power supply, providing a clearer picture of market concentration than aggregated data.

- Targeting opportunities: Subsidiary-level analysis allows investors to identify specific growth pockets or divestment risks that are otherwise hidden in group-level financial statements.

The full publication will provide you with a comprehensive analysis of this 40 GenCos:

- capacity and power generation mix in 2024

- evolution over the last 10 years of:

- thermal capacity and intensity factors

- installed capacities

- CO2 emissions

- Short and mid-term developments

- And more…