The evolution of the European electricity markets to 2050: policies, power mix, prices

Following a European Commission proposal last year, EU leaders agreed in December 2020 to cut greenhouse gas emissions by 55% compared to 1990 levels by 2030. This represents a substantial increase from the earlier target of 40% and was initially met with some resistance by several Member States.

To meet this new objective, the European power sector will need a major overhaul. What impacts will this have on the power markets evolution, and on prices?

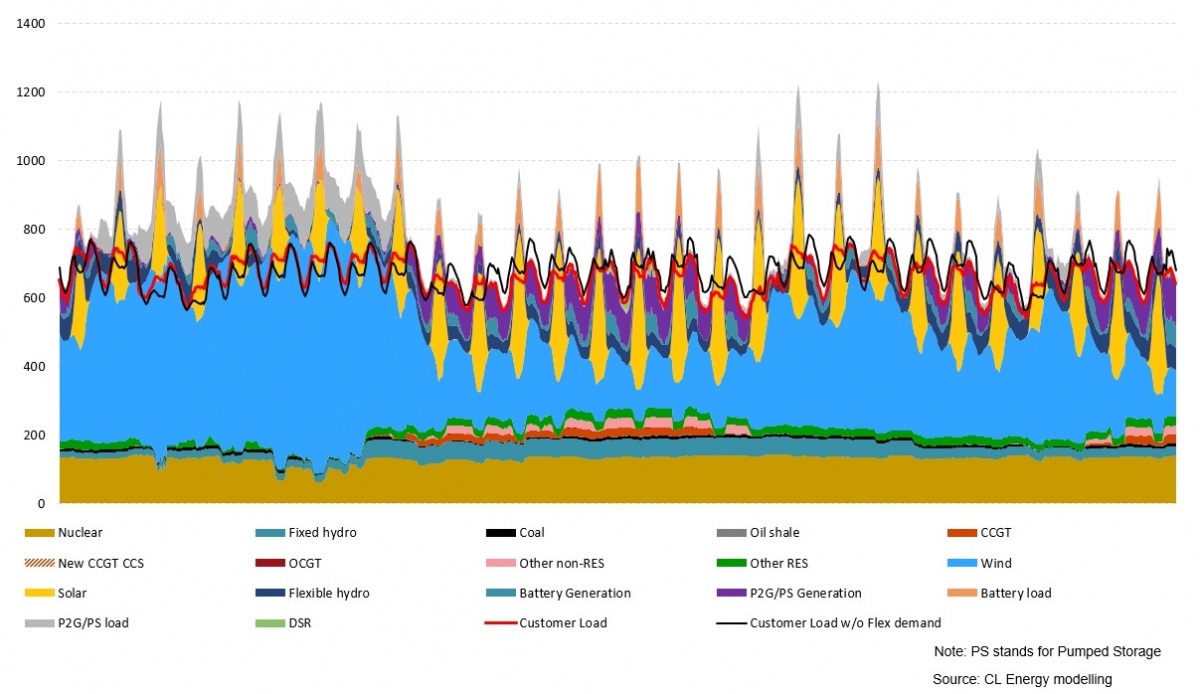

European power market modelling – Hourly equilibrium

Enerdata and Compass Lexecon have leveraged their European Power Markets Outlook Service in this detailed presentation, which includes:

- An overview of the latest energy policies

- European Green deal,

- National coal phase-out plans and nuclear strategies,

- Transmission networks development

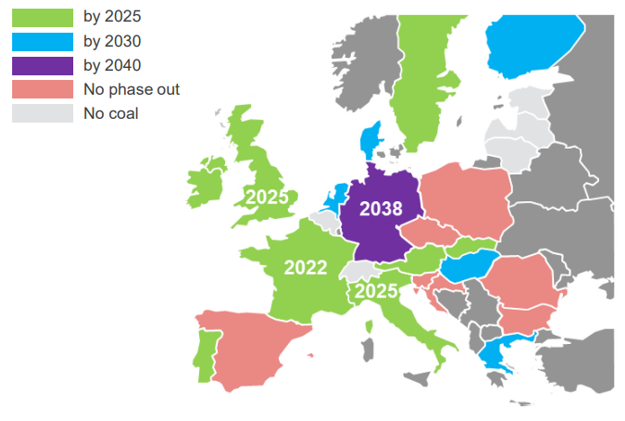

Coal phase out plan in Europe

- Focuses on:

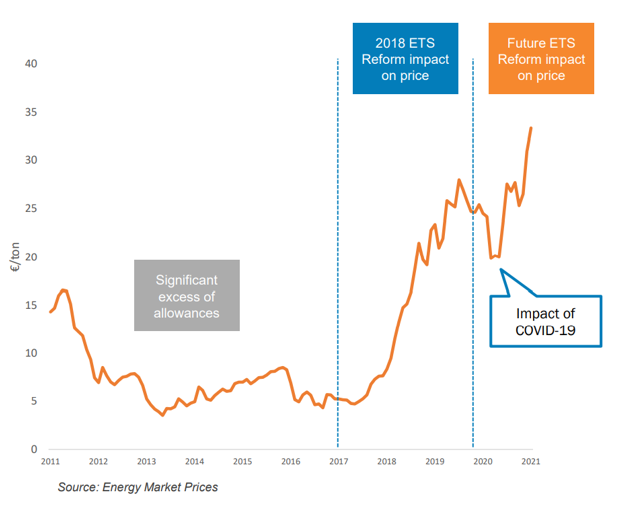

- The recent evolution of the EU CO2 ETS market (short term), with significant CO2 prices increases following the 2018 ETS reform and the latest EU ambitions towards decarbonisation. Possible further ETS reforms in the context of the European Green Deal are also reviewed.

Evolution of CO2 price (€/ton, nominal)

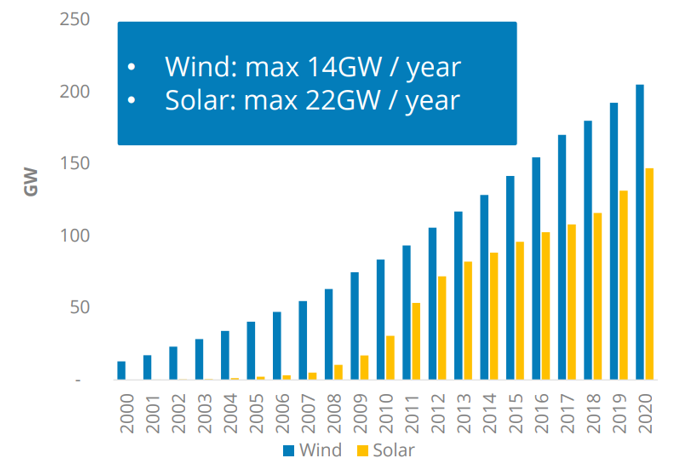

- The increased renewables penetration in the power sector (medium term). Capacities have soared over the last decade, enabled by support schemes, and they should continue to grow at a sustained pace to support decarbonisation.

Cumulative additions in Wind and PV (EU27+GB)

Source: Enerdata, Global Energy and CO2 data

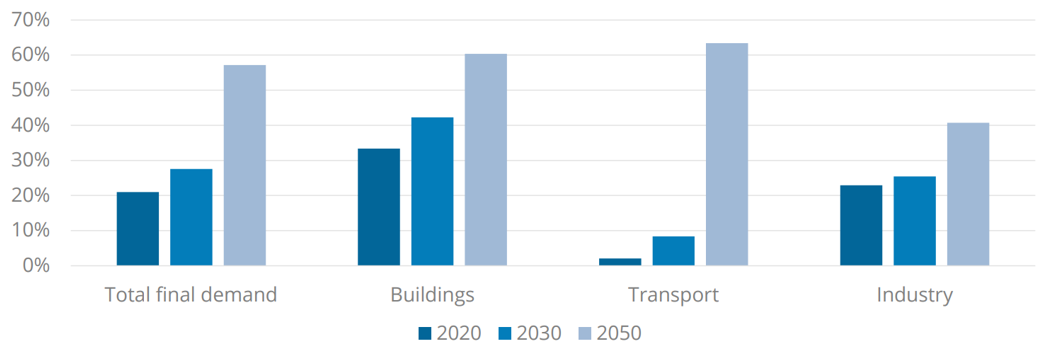

- The role of electricity in decarbonisation (long term). All scenarios towards more decarbonisation lead to an increase in electricity demand with the electrification of end uses.

Share of electricity, EPMO base scenario

Source: CL Energy Analysis, Enerdata

- An analysis of the latest annual EU countries price projections to 2050, including EPMO outlook scenarios.