Download the full publication (FREE)

Spotlight on China’s energy and climate strategies

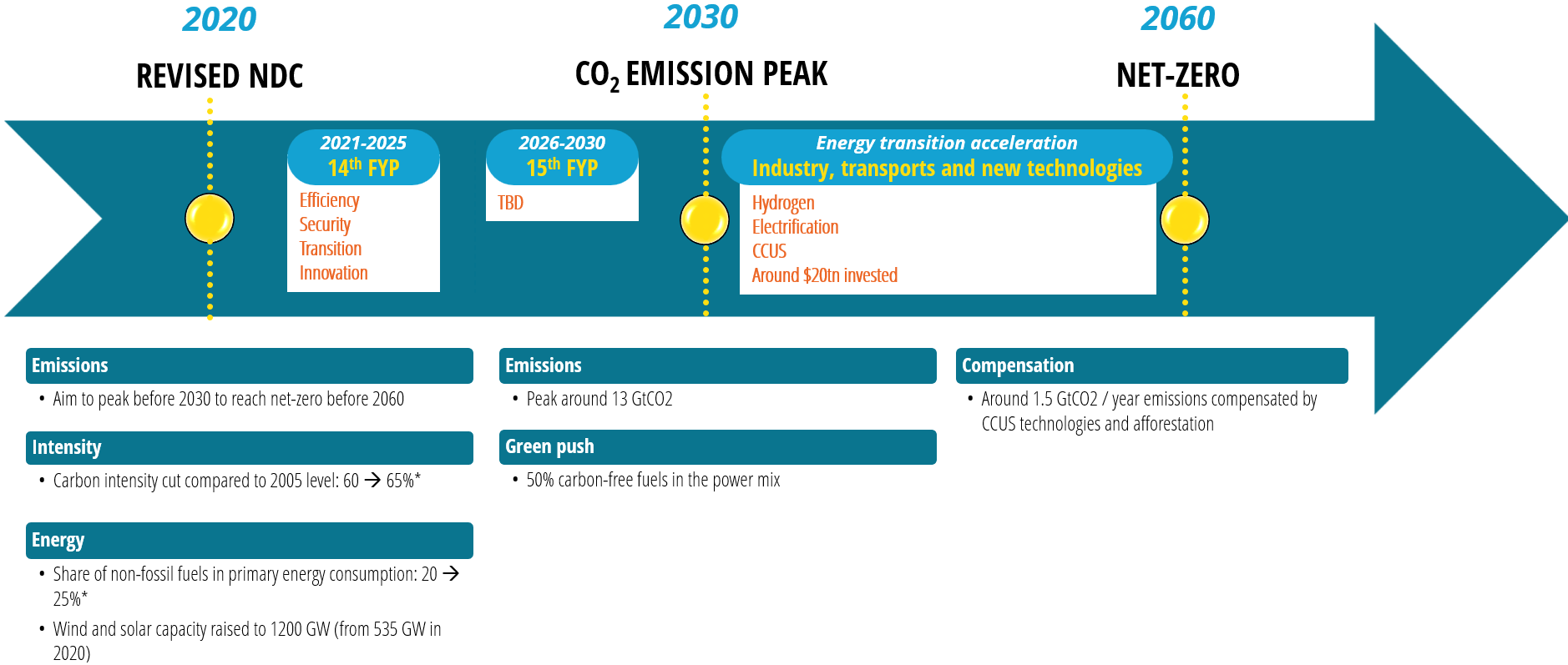

The energy industry in China was historically designed to support rapid growth, turning China into the world’s factory. As an engine of global economic development, China is now facing the fallout of its carbon-intensive prosperity. The country is torn between sustaining growth, and launching energy transition to deal with climate and pollution issues. As the #1 CO2 emitter, the power sector must adjust. Recently, the country has made notable progress in fostering renewable energies. The targets are clear: a peak of CO2 emissions in 2030 and net-zero by 2060. However, Chinese coal consumption surged last year, raising questions on the ability to shift out of carbon dependency.

As a self-asserted diplomatic leader on transition and climate issues, China acknowledges its huge responsibilities. Since the country accounts for a third of global emissions, its role is key and influences the global trends. At a time when uncertainties loom over our ability to mitigate global warming, there exists no credible pathway to limit the global temperature rise to 2 °C without the involvement of China. This is the reason why, while the Sixth Assessment Report synthesis provided by the IPCC in March warns that emission levels are inconsistent with warming mitigation targets, most eyes are on Chinese energy transition achievements. Through this report, Enerdata aims to shed light on the latest energy figures and climate policies in China, with a medium and long-term outlook.

CATALYSING ENERGY TRANSITION: CONTEXT AND STAKES

On the back of economic rebound, CO2 emissions recorded a 5.5% y-o-y increase in 2021 and 1% in 2022. The surge in domestic coal consumption by 8.8% in 2022 was offset by a slowdown in industrial production and a lower coal heating value in the energy sector, keeping the emission level rather steady (Enerdata 2023). Time will be needed to assess whether this reflects a short-term adjustment or a worrying trend. China’s dependency on coal destroys the requirements for a +2 °C warming scenario, as China CO2 emissions per capita are more than 3 times higher (7.4tCO2 /cap, Enerdata 2023) than the 2tCO2 /cap target from the Paris Agreement. Electricity generation and industrial production share the top spot, each accounting for a third of the country’s GHG emissions.

-

Economic and CO2 emission features

Over the past three decades, China has positioned as the main engine of global economic growth and is now ranked second in terms of GDP (behind the US). While China’s growth has historically been fuelled by manufactured products and exports, the economic structure is gradually shifting towards service activities, which now represent more than half of the country’s value added (53%, WB 2021). Expanding at more than 5% a year during the 2010s, Chinese economy suffered from the pandemic and the zero-Covid policy. The 2022 growth was sluggish, with a 3% increase in GDP, making it the second-lowest rate (behind 2020) for about 50 years. Energy-wise, final consumption per capita never fell, rising at 4.2% per year on average since 2018 (Enerdata, 2023). As a drawback of its economic structure and power, China is the top GHG emitter, accounting for a quarter of worldwide emissions with 13.5 GtCO2eq/ year (including 12.5 Gt of CO2, a third of world total) spurred by high coal-fired power generation. ...