See also

Power CAPEX and Renewables LCOE Module

Weigh investment decisions leveraging thousands of data points and meaningful averages.

Evolution of the Wind Turbines Manufacturers’ Market Share

Get this executive brief in pdf format (Free)

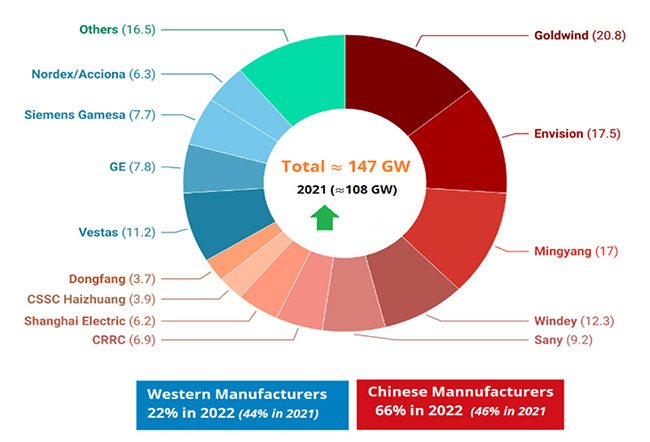

Enerdata's analysis of the wind market, a crucial facilitator of the energy transition, reveals a significant shift towards Chinese manufacturers. American and European leaders, such as Vestas, Siemens Gamesa, and GE, are experiencing substantial declines in both take-in-orders and market share. In contrast, Chinese manufacturers, led by Goldwind, Envision, and Mingyan, have seen a considerable increase in take-in-orders and market share. The overall world market by in-take-orders has grown from 108 GW in 2021 to 147 GW in 2022, representing a remarkable 37% year-over-year increase. Notably, prices have been continuously rising during 2022 and early 2023 for American and European manufacturers, with Vestas increasing to €1.2 million/MW, Siemens Gamesa to €0.8 million/MW, and Nordex/Acciona to €0.9 million/MW. These price escalations can be attributed to various factors, including the rising costs of raw materials such as steel and critical minerals, supply chain disruptions, and quality issues.

Figure 1: Global Wind Turbine Manufacturers' Market Share by Take-in-Orders 2022 (GW)

Source: Enerdata (Data derived from companies’ annual reports)

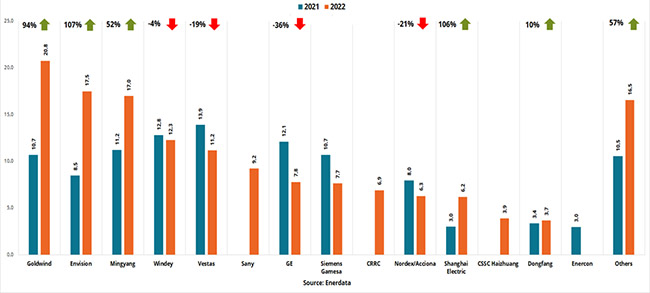

Enerdata’s statistics show that Goldwind, a Chinese manufacturer, increased its in-take-orders from 10.7 GW in 2021 to 20.8 GW in 2022, a year-over-year growth of 94%. This growth is incredible especially when we see declining shares of Western Manufacturers. Other Chinese manufacturers also saw substantial growth. Envision's in-take-orders increased from 8.5 GW in 2021 to 17.5 GW in 2022, a 107% year-over-year growth. Mingyang's in-take-orders increased from 11.2 GW in 2021 to 17.0 GW in 2022, a 52% year-over-year growth. Other key Chinese players include Sany 9.2 GW, Shanghai Electric 6.2 GW and CSSC 3.9 GW. This growth among Chinese manufacturers is driven by China's 14th 5-year plan, which targets a 50% increase in renewable energy generation between 2020 and 20251.

In contrast, European and American manufacturers experienced a drastic decline. Vestas, a Danish manufacturer, saw its in-take-orders decrease from 13.9 GW in 2021 to 11.2 GW in 2022, a 19% year-over-year decline. Similarly, GE, an American manufacturer, saw its in-take-orders plummet from 12.1 GW in 2021 to 7.8 GW in 2022, a 36% year-over-year decline. Siemens Gamesa in-take-orders plunged from 10.7 GW in 2021 to 7.7 GW in 2022 a 39% fall. Nordex/Acciona only producing onshore models also joined retreating list with in-take-orders falling from 8 GW in 2021 to 6.3 GW in 2022. Enerdata’s list of top 15 manufacturers by in-take-orders reveals that all Western manufacturers suffered significant decline in their 2022 records. Contrariwise, all Chinese manufacturers who made it to the list witnessed significant growth.

Figure 2: Global Wind Turbines Take-in-Orders 2021/2022 (GW) (onshore + offshore)

Source: Enerdata (Data derived from companies’ annual reports)

Market Shift

The shift in wind turbine manufacturing from Europe to China has been influenced by several factors. China's competitiveness as a manufacturing location, the Chinese government's push to develop the entire wind supply chain, and ambitious renewable energy targets have all played a significant role. China's emergence as the world's leader in wind energy markets, its expansion across wind energy value chains, and the development of the world's largest and most efficient wind turbines have also contributed to this shift. Additionally, China's wind industrial policy, including feed-in tariffs, domestic content requirements, and industrial subsidies, have supported the growth of the wind industry2. However, this shift has come at a cost, including inefficiencies in site selection and turbine model choices, as well as tensions with the West over technology acquisition.

Europe is the second-biggest manufacturing location for wind turbines worldwide, home to a large industrial ecosystem of wind turbine manufacturers and suppliers, with 250 factories across the continent. Almost all wind turbines installed in Europe have been assembled in Europe. The European Commission has recently doubled down on its commitment to the wind energy sector, proposing a set of actions to strengthen domestic production capacity for new wind turbines. Despite challenges, European wind turbine manufacturing remains a critical component of the industry, with a large industrial ecosystem of wind turbine manufacturers and suppliers. The European Commission has proposed a set of actions to strengthen the wind energy sector, aiming to double the continent's wind energy capacity to meet ambitious renewable energy targets3.

Zoom-in on Siemens Gamesa

Siemens Gamesa, a major wind turbine manufacturer, has faced significant challenges, losses, and defects in its onshore wind turbines. The company has encountered quality issues with its 4.X and 5.X onshore wind turbine platforms, including flaws in rotor blades and bearings, leading to component failures, small cracks, and other quality flaws. This has affected a substantial number of turbines, with an estimated 15-30% of the 4.X and 5.X models being problematic. The company's CEO, Jochen Eickholt, acknowledged that the turbines were not sufficiently tested, and the company is expected to incur significant costs, with up to $5 billion in net loss for the parent company and an estimated €1.6 billion to fix the issues, with most of the costs occurring in 2024 and 20254.

In addition to the quality issues, Siemens Gamesa has also faced supply chain turbulence, cost overruns, and construction delays. The discovery of a serial defect in its fleet has further added to its troubles. The wind turbine division losses are driven by restructuring costs and challenges in its onshore division. The problems have raised concerns about the wider wind industry, with analysts worried about potential industry-wide technical failures. However, industry bodies have emphasised that the problems are limited to the company and do not necessarily indicate a broader issue across the industry5.

Prices evolution:

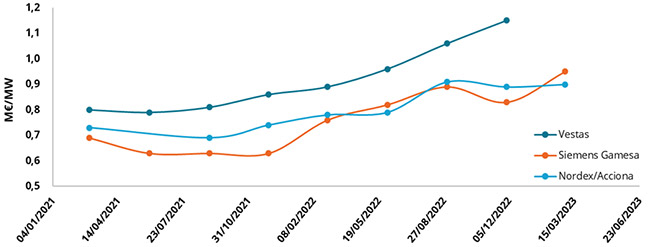

The evolution of wind turbine prices in recent years has been marked by significant changes. In 2021, most manufacturers maintained relatively stable prices, with Vestas at €0.8 million/MW, Siemens Gamesa at €0.7 million/MW, and Nordex/Acciona at €0.7 million/MW. However, by 2022, prices began to rise, with Vestas increasing to €1.2 million/MW, Siemens Gamesa to €0.8 million/MW, and Nordex/Acciona to €0.9 million/MW. The trend continued into 2023, with Vestas reaching €1.1 million/MW and Siemens Gamesa at €1.0 million/MW. These price increases can be attributed to various factors, including the rising costs of raw materials such as steel and critical minerals, supply chain disruptions, and quality issues affecting certain manufacturers. Chinese manufacturers don’t seem to have the same pressure of rising costs, as they can tap into abundant local supply of raw materials and generous subsidies. Prices circulating are rather conflicting or unrealistic, given that Chinese companies don’t publicly publish their prices. However, prices hovered around €0.6 million/MW in 2022, which is significantly lower than western manufacturers.

Figure 3: Average Selling Price of Wind Turbines (M€/MW)

Source: Enerdata (Data derived from companies’ annual reports)

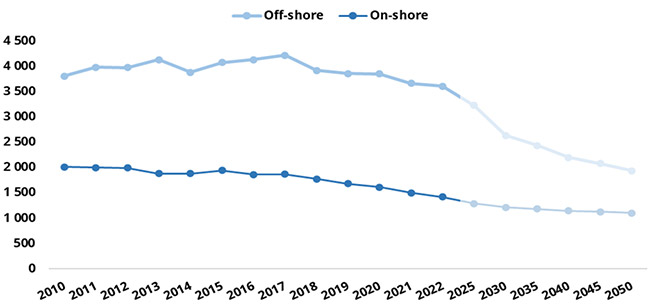

Despite the increasing trend of prices of wind turbines, the average for total projects’ CAPEX has declined continuously for both onshore and offshore wind projects. The declining CAPEX for offshore is greater than that of onshore wind. In 2022 average CAPEX for onshore wind stood at $1420 kW, while offshore stood at $3609 kW. According to the forecasting of Enerdata Power Plant Tracker the declining CAPEX is expected to continue until 2050 but at a slower rate. By 2030 it is estimated that onshore CAPEX will be $1216 kW and offshore wind will be $2636 kW6.

Figure 4: Average CAPEX for Wind Turbines ($/kW)

Source: Enerdata - Power Plant Tracker

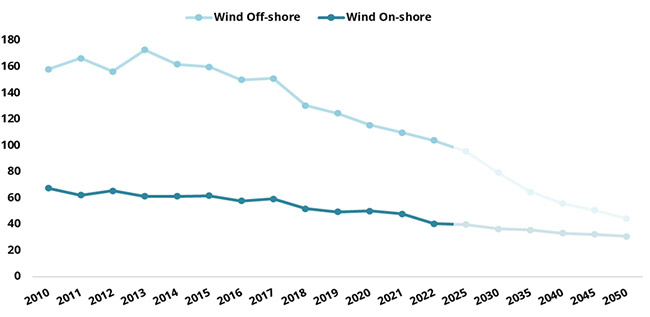

The declining overall CAPEX influence quite similar decline of the levelised cost of electricity LCOE for both onshore and offshore wind. In 2022, the average LCOE of onshore wind stood at $40,48 MWh and offshore $103,86 MWh. By 2030 Enerdata projects an average LCOE of $36,50 MWh for onshore wind, and $79,32 MWh for offshore wind – a substantial decrease of 34% for offshore wind. The declining average LCOE is projected to continue at a slower rate until 20507.

Figure 5: Average Levelised Cost of Electricity LCOE for Wind ($/MWh)

Source: Enerdata - Power Plant Tracker

Where is the industry heading?

The wind industry is experiencing significant global expansion, with China leading the way in both onshore and offshore wind power capacity. Additionally, the US wind manufacturing sector is making a comeback, buoyed by tax credits and improved market conditions8. The GWEC9 expects the installed capacity to hit the milestone of 1 TW worldwide, in 2023. Enerdata’s Power Plant Tracker10 database has detailed information on renewable and non-renewable electricity generation and storage assets around the world. The market is projected to add another 2 TW of installed capacity in the coming 7 years, reaching 3 TW by the end of the decade11. This growth is driven by increasing number of product launches, rising demand for floating wind technology, and rising number of wind farms. Floating turbines represent a gigantic potential of 10 TW in North America, 7.5 TW in Europe according to Enerdata12.

As the industry continues to grow, manufacturers adapt to the evolving market by focusing on either onshore or offshore segments, mastering logistical complexities, and continuously adapting operating models to meet new challenges. Bottlenecks, include lengthy and complicated permitting processes, supply chain disruptions, cost overruns, and construction delays. The industry is also experiencing fierce competition, with financial pressures on wind farm operators and original equipment manufacturers (OEMs) due to competitive bidding and a shift from fixed, subsidised tariffs to an auction-based system13. There is also a shortage of skilled labour, and transportation of turbines has become more complex due to increasing turbine size. Quality issues have also emerged, as seen in the case of Siemens Gamesa, where significant flaws in rotor blades and bearings have led to component failures, resulting in substantial financial and operational impacts. These challenges require the industry to focus on streamlining permitting procedures, expanding capacity, addressing supply chain disruptions, and investing in research and development to improve turbine quality and reliability14.

KEY TAKEAWAYS

- Substantial year-over-year of wind turbines take-in-order (37%).

- Chinese companies hold 66% of the market share in 2022 compared to 46 in 2021.

- American and European companies hold 22% in 2022 compared to 44% in 2021.

- Western companies are facing increasing pressure from Chinese competitors.

- Prices have seen steady increase during 2022 and early 2023.

- The industry is projected to continue growing worldwide.

- Supply chain, access to materials and quality issues are expected to be main concerns to all players.

Notes:

- China’s 14th Five-Year Plans on Renewable Energy Development (efchina.org)

- China's policy pathway for developing the wind power industry - ScienceDirect

- European wind turbine manufacturing | WindEurope

- What’s the problem with Siemens Gamesa’s onshore wind turbines? [Update] (electrek.co)

- Siemens Energy wind turbine problems could be an industry-wide issue (cnbc.com)

- World Power Plant Database | Power Plant Status & Capacity (enerdata.net)

- World Power Plant Database | Power Plant Status & Capacity (enerdata.net)

- US wind manufacturing makes a comeback | Canary Media

- GWEC - Global wind report 2023

- World Power Plant Database | Power Plant Status & Capacity (enerdata.net)

- Global Wind Report 2023 - Global Wind Energy Council (gwec.net)

- Offshore wind goes floating (d1owejb4br3l12.cloudfront.net)

- Wind - IEA

- Quality Problems Hit the Wind Energy Industry - IER (instituteforenergyresearch.org)

ABOUT THE AUTHOR