See also

Market Research / Studies

Granular and exclusive insight to address the most pressing business and strategic issues.

An emerging technology backed by public policies

Get this executive brief in pdf format (free)

Small Modular Reactors (SMRs) represent an innovative approach to nuclear fission technology. They offer power capacities of up to 400 MW per unit, or around a third of conventional ones. Thanks to their small size and special characteristics, several countries are positioning themselves on the technology. Indeed, they are considered promising for mitigating climate change while also meeting energy demand.

The development of SMRs is progressing worldwide. The primary end-use is power generation, meant to provide flexible power for both grid-connected and remote areas. This paper focuses on SMRs for power generation.

Experts stress the importance of technical and regulatory developments, fuel supply chains and international standardisation of licensing for wider adoption. The United States (US), Russia, China, the United Kingdom (UK), and Canada are amongst the most advanced countries in the development of SMR technology. The European Union plans to increase its nuclear power capacity by 2050 which includes deploying a fleet of SMRs.

Technology characteristics

SMR benefits and end-use potential

Thanks to their modest size, SMRs offer several sought-after advantages such as: 1) lower initial capital investment, 2) reduced construction time, 3) greater scalability, 4) geographic flexibility for locations unable to accommodate larger reactors, and 5) potentially enhanced safety compared to traditional designs.

Current SMR deployments target hard-to-abate sectors and applications where renewables and large-scale nuclear have limitations. Potential applications include coal replacement for on-grid power, fossil fuel cogeneration replacement for industries, diesel replacement for off-grid mining, fossil fuel replacement for district heating, hydrogen, and synthetic fuels, etc.

SMR end-uses applications depend on their size (capacity/module) and geography:

5-15 MW: for off-grid needs such as isolated communities, military and defence use.

15-200 MW: for heat and/or electricity in energy-intensive industrial sites (i.e., desalinisation, mines, O&G extraction, or hydrogen production).

200-400 MW: for network connected-power generation: 1) replacement of existing coal-fired power plants, 2) electrification of medium-sized cities and isolated industrial centres, 3) networks with insufficient capacity for higher power plants.

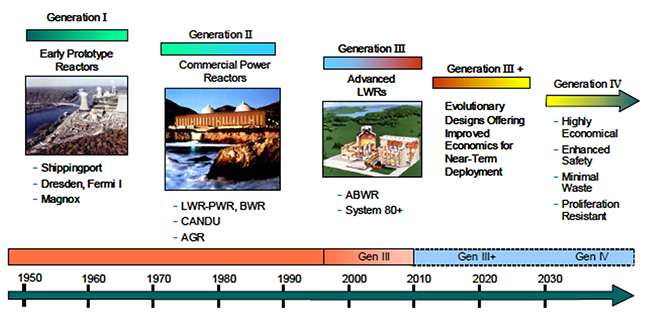

Nuclear reactor generations

Nuclear power technology developments started in the 1950-60s with Generation 1 (Gen I) reactors and have been evolving, triggered by learnings from experience (including nuclear incidents & accidents1).

Below (Figure 1) is illustrated the timeline of the different nuclear reactor generations. Each new generation aims at increasing safety and reliability and reduce costs.

Figure 1 – Technology roadmap, Gen4 International Forum (GIF), Dec. 2002

Gen I: “Uranium Naturel Graphite Gaz” (UNGG) or Gas Cooled Reactor (GCC)

These reactors were developed in France, in 1950/1960s and installed in 1970s. Gen I reactors were mainly based on natural Uranium (U238) fuel. The technology is now obsolete, and most reactors are dismantled.

Gen II: Technologies such as US’ Pressurised Water Reactors (PWRs), US’ Boiling Water Reactors (BWRs), Russian RMBK technology, etc.

Gen II technology represents around 2/3rd of nuclear reactors in operation, including those used in mobility (submarines & ships).

Gen III: “European or Evolutionary Pressurised Reactor” (EPR), by France & Germany

These reactors were designed to be safer and use uranium more efficiently than older Gen II reactors. Some designs also feature high power output capability. They include technologies such as US’s APWR and Russian’s VVER and others. As of May 2024, one deployment has been recorded in China (Taishan power plant), operational since 2018 (construction started in 2008) and one in Finland (Olkiluoto power plant), operational since May 2023. Other European projects are currently under construction (Flamanville 3 in France has just been allowed to load fuel and should be fully operational by the end of 2024)

Gen IV: Under investigation for 2030, Thermal reactors & Fast Neutron Reactors (FNR)

In 2001, the US joined by 13 countries2 & EURATOM, to establish the Generation IV International Forum (GIF)3. The goal was “to cooperate to develop the research necessary to test the feasibility and performance of 4th generation nuclear systems, and to make them available for industrial deployment by 2030”.

There were 7 key objectives set for 4th generation reactors:

- Improve nuclear safety,

- Reduce the risk of nuclear proliferation, by "burning" stocks of plutonium,

- Minimise nuclear waste, by recycling and transmuting the actinides produced by nuclear reactions,

- Save natural resources,

- Reduce the construction and operating costs of nuclear reactors,

- Reach a technical maturity by 2030,

Enable uses other than power generation, such as the production of hydrogen and drinking water (desalination), and the recovery of waste heat (generally lost in Gen I, II, and III of nuclear power plants).

Delivering on all the 5 objectives first would turn to be a radical breakthrough versus the previous generations. The challenge lies in the time to deliver these promises as most of these reactors are not forecast to operate before 2035 to 2040.

There are multiple technologies in Gen IV, these can be segmented into 2 main categories:

- Thermal reactors (using “slow” neutrons)

- Fast Neutrons Reactors (FNR) or Fast Breeder Reactors (breed = feeding on fuels such as MOX fuel, which is “burnt”; or for some types they can generate more fuel than they burn).

SMRs can use both Gen II and Gen III (e.g. Russian designs such as KLT-40S or RITM-200) but most current designs use Gen IV technology.

Current projects, technology maturity and foresight

Current SMR reactor designs and projects

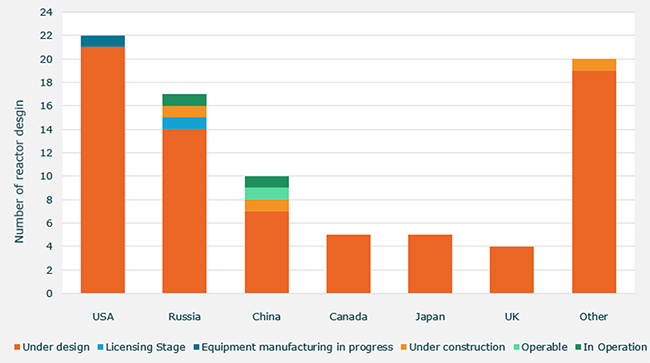

Over 80 SMR technology designs are currently under development in 18 countries (see Figure 3). The USA leads in terms of number of SMR technology design recorded (22 different designs), followed by Russia (17), China (10), Japan (5), Canada (5), and the UK (4) - Figure 2-. Most of SMR technologies worldwide are still under the design stage of development.

Figure 2: Worldwide SMR reactor designs by country of origin (2022)

Data source: IAEA, 2022; Enerdata 2024

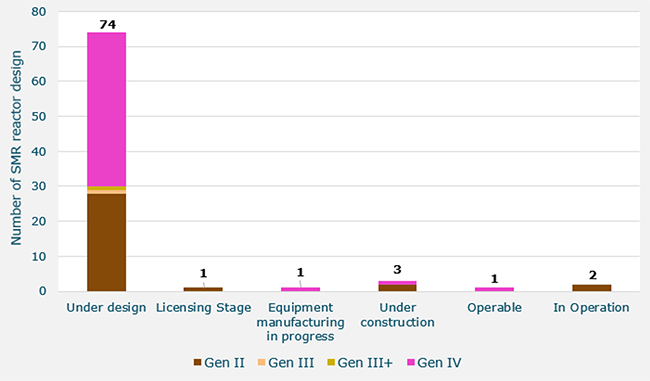

As per 2022 IAEA data, only two types of technologies are currently functioning: the 70 MW Russian KLT-40S by JSC Afrikantov OKBM (PWR, Gen II, used for the Akademik Lomonosov floating nuclear power plant), and the 210 MW Chinese HTR-PM by Tsinghua University (HTGR, Gen II). Another Chinese design by Tsinghua University, the 2.5 MW HTR-10 (HTGR, Gen IV), is operable.

While current operational projects are Chinese and Russian Gen II reactors designs, most of the new SMR technologies under design are Gen IV reactors – see Figure 4-. Most of Gen II designs are studied in Russia (12 out of 17 Gen II under design). On the other hand, Gen IV reactors are being studied globally: USA (15 reactor designs), Russia (5 designs), Canada (4), South Africa (4), Japan (4), etc.

Figure 3: Worldwide SMR reactor technology design by status and Generation (IAEA, 2022)

Data source: IAEA, 2022

Figure 4: Worldwide SMR reactor technology design by status and Generation (2022)

Data source: IAEA, 2022; Enerdata, 2024

About 22 GW4 of SMR projects are currently underway in the first quarter of 2024 (i.e. +65% since 2021); but none of those projects are under an advanced development phase. The US leads in announced SMR projects, with nearly 4 GW. Most SMR projects are still in the planning stages, but the industry achieved a milestone with the activation of the world's first commercial 210 MW SMR (Gen II) in China in 2023.

Technology maturity and foresight

The technological maturity of SMRs varies according to the design and the project. Several studies have been carried out to assess the maturity level of SMR technologies, considering factors such as design maturity, safety, economics, and operability. Overall, while some SMR designs have reached advanced stages of development and regulatory maturity, others are still in the early stages of technological maturation.

Overall progress in the SMR sector over the past decade has been modest, hampered by technological and economic challenges.

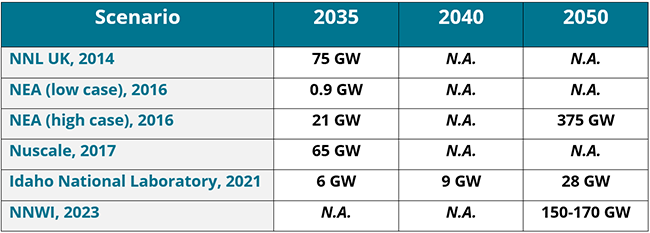

According to various expert scenarios, the world’s total installed SMR capacity for 2050 could range from 28 GW to 375 GW for the most optimistic scenario (see Figure 5). Average forecasts for 2035 have come down significantly from earlier predictions, from 65-75 GW forecasts made a decade ago against 6 GW in more recent scenarios. As the current pipeline of projects is estimated at 22 GW5 in 2024 (including less than 5% under development and advanced development phase), optimistic scenarios (65-75 GW) for 2035 seem quite unrealistic.

The first wave of deployments is expected to take place around 2030-20356. Advanced SMRs (Generation IV) could face greater delays due to complex technological, licensing, supply chain and fuel supply issues, which could materialise by 2040.

Figure 5: Worldwide SMR potential capacity pipeline development by 2050

Source: NNWI, 2023

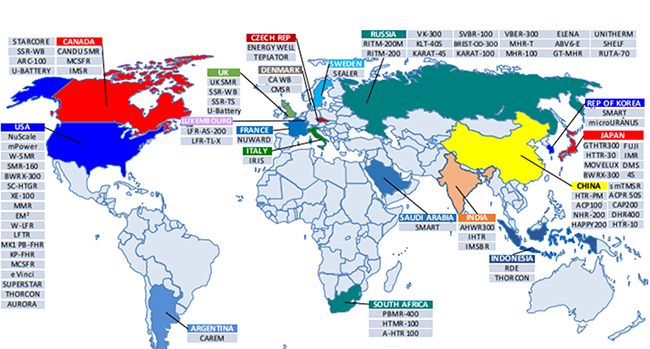

Many companies are amongst the designers of SMRs: for Gen II designs (Nuscale Power, Nuward, Holtec International, Westinghouse Electric, BWX Technologies, etc.); for Gen IV designs (General Atomics, Terrestrial Energy, Terra Power, Thorizon, Seaborg, Stellaria, etc). Many startups are also starting to work on the technology.

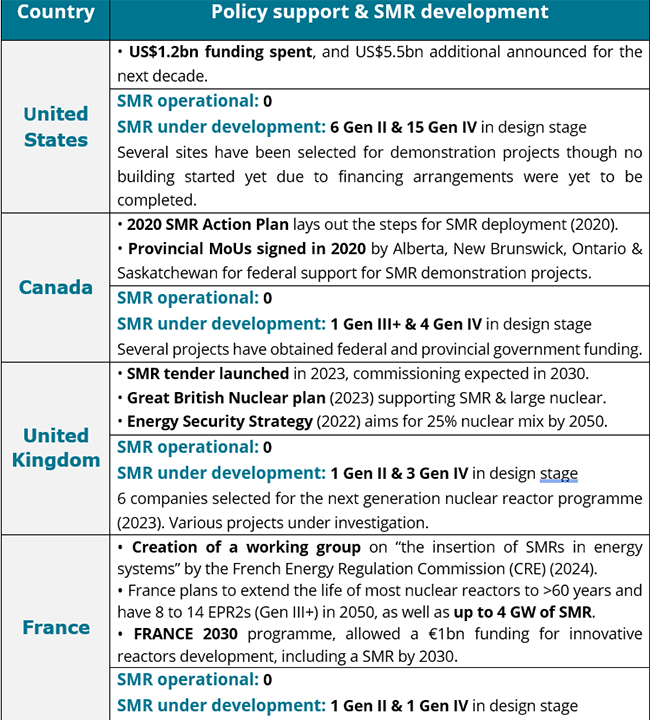

SMR developments resulting from interventionist policies

On a supranational level, the European Commission created the European Industrial Alliance in February 2024 to facilitate the development of SMRs in Europe by the early 2030s. The alliance will in a first phase identify: (i) technically mature and commercially viable SMR technologies that could be supported under the alliance, (ii) gaps and potential solutions in the European SMR supply chain, (iii) barriers to investment, funding opportunities and new blended funding options to support SMR development, (iv) future research needs and identification of existing skills gaps along the supply chain. By Q4 2024, the alliance will propose a roadmap for the technology development, and by Q1 2025 a strategic plan is expected to be in place.

The US government is keen to attract SMR project developments and private investors. The US Department of Energy has spent over US$1.2bn on SMR and has announced additional funding for the next decade that could amount to US$5.5bn7. No SMRs have been commissioned in the US yet, however, the US Nuclear Regulatory Commission certified NuScale Power's 77 MW SMR in 2023. At a regional level, the Governor of Virginia approved two bills in 2023: (i) the creation of the Virginia Power Innovation Fund, designed to support R&D in various advanced energy technologies, including SMR, and (ii) the creation of the Nuclear Education Grant Fund, which will award grants to schools setting up a nuclear education programme specialising in innovative technologies such as SMR. Virginia is the first US state in terms of installed data centres (i.e. a target for SMR installation).

Canada is positioning itself as a market leader thanks to government support at both federal and provincial levels. The largest commitment, which reached over US$745m, is from the Infrastructure Bank of Canada for the Darlington SMR project (2022). In August 2023, Canada approved US$55m in funding for the development of an SMR reactor in Saskatchewan, led by SaskPower. Several models have undergone design review by the supplier before being approved. According to the Canadian Energy Regulator's forecasts, the use of nuclear energy, and through the development of SMRs, will increase considerably between 2040 and 2050 in the country, with a growth of around 10%. The report notes that SMR generation will reach over 240 TWh in 2050 in the global net-zero scenario.

The US and Canadian governments are also keen to develop the nuclear sector for hydrogen production. The Canadian government introduced a 15% refundable investment tax credit for clean electricity in its 2023 budget, which can be applied to all new nuclear facilities (including SMRs, large facilities and new refurbishment projects). Canada is aiming for hydrogen from non-carbon emitting sources to provide up to 30% of end-use energy by 2050. Several Canadian companies are carrying out studies to determine the potential for hydrogen production in nuclear power plants.

The UK aims to supply up to 25% of the UK's electricity from nuclear power by 2050. In July 2023, the country launched the Great British Nuclear plan to support both SMR technology and large nuclear power plants. Following the plan’s announcement, a tender was launched for the development of SMR reactors, with the aim of commissioning in early 2030. Alongside the competition, the UK government unveiled a programme of grants of up to US$195m to accelerate the development of advanced nuclear businesses, support the design of Advanced Modular Reactors (AMRs) and develop new fuel production capacity. At the end of 2023, 6 companies were selected for the next generation nuclear reactor programme8. EDF, GE-Hitachi Nuclear Energy International, Holtec Britain Limited, NuScale Power, Rolls-Royce SMR and Westinghouse Electric Company UK Limited were selected for the next stage of the process. Independently, Holtec Britain received a grant of US$38m to complete Stages 1 and 2 of the Generic Design Assessment to develop Holtec's SMR-300 product. According to the Environmental Audit Committee (EAC), the UK government's position on SMR lacks clarity despite its public policies. Concerns have been expressed about waste management and regulatory processes.

China aims to generate 10% of its power from nuclear by 2035 and 18% by 2060. The overall state support for the nuclear sector is vast, therefore China does not publicly disclose the extent of its public support for SMR R&D spending. Estimates suggest it amounts to at least several hundred million US dollar9, not including corporate funding from China National Nuclear Corporation (CNNC) and China General Nuclear Power Group. Through its public companies, the country is strengthening its position in the SMR market. In 2023, China's National Energy Administration and China Huaneng commissioned the 210 MW Shidaowan nuclear power plant, featuring a high-temperature gas-cooled reactor (HTGR). Construction of a second model, the ACP100 or Linglong One, began in July 2021, six years later than planned, and start-up is now expected in February 2026. The 125 MW ACP100 reactor is developed by the CNNC. This 125 MW reactor is designed for a variety of uses, including power generation, district heating and desalination.

In 2012, South Korea’s nuclear safety authority approved the SMART (System-Integrated Modular Advanced Reactor) model developed by the Korea Atomic Energy Research Institute. No order has been placed for the model since then. In July 2023, South Korea launched a US$305m government project to develop a national SMR by 202810. A SMR Alliance11 was also launched in July 2023 grouping together 42 public and private entities to develop the SMR industry in the country. South Korea is betting on international collaborations, notably with the US, and an MoU12 has been signed between Ultra Safe Nuclear Corporation (US) and Hyundai Engineering and SK Engineering & Construction (both South Korean companies).

France is another example of a country seeking to establish a long-term foothold in the SMR market by using public intervention as a tool. In March 2022, the French Government launched a call for funding “Innovative nuclear reactors” project to support SMR development as well as other new concepts of innovative nuclear reactors. 11 winner companies received financial support of around €130m13 from the state between 2023-2024 for the call of project. The state-owned power group EDF announced in March 2023 the creation of its subsidiary NUWARD to strengthen the development of its own SMR - now in the preliminary design phase. France plans to extend the life of most nuclear reactors to 60 years and beyond and have 8 to 14 EPR2s (Gen III+) in 2050, as well as up to 4 GW of SMR.

As China, Russia does not disclose figures regarding SMR sector funding. Via its state-owned company Rosatom, the country holds its place as a player in the SMR market. Russia operates two 35 MW each SMRs on board a barge (the Akademik Lomonosov), coupled to the network in 2019 with a 9-year delay. The construction of a second SMR project, a lead-cooled breeder reactor called BREST-300, was launched in June 2021. This project had been under discussion for 10 years and was originally scheduled to enter construction in 2018. In 2023, the nuclear regulator granted a licence to build the country's first land based SMR in Sakha: Rosatom approved the design of a SMR suited for the Republic of Sakha project, scheduled for completion in 2028. The thermal capacity of RITM-200N reactor is 190 MW, while its electric capacity is 55 MW. In terms of international cooperation, Russia, via Rosatom, is discussing the construction of SMRs with Kyrgyzstan, Uzbekistan, and Myanmar.

Figure 6: Policy support & SMR development

SMR development facing challenges.

While SMRs offer some advantages, several challenges need to be addressed. In fact, many experts have raised the alarm about economic challenges. Some countries, including Argentina, China, Canada, France, India, South Korea, Russia, the UK, and the US, have encountered difficulties in SMR development.

The first challenge in developing SMRs is the high cost compared with other technologies, mainly as the technology is not stabilised yet.

Ongoing projects are jeopardised due to cost issues. In South Korea, a project consisting of the commissioning of six 77 MW NuScale units in Uljin County would have seen its investment cost increase by 220% compared to 2018 figures. For this project, investment costs have been revised upwards, while electricity production estimates have been cut by 23%. In the US, in 2021, eight municipalities withdrew from an investment project, reducing subscriptions to 101 MW for a six-module project (462 MW). Following a price increase deemed too significant, the project was abandoned in 2023. Additionally, NuScale Power's Utah power plant project has been halted due to cost issues: the estimated costs were increased from US$58/MWh to US$89/MWh. The Russian KLT-40S SMR project also suffered significant cost overruns, taking 13 years to complete.

The risks linked to lengthening implementation time explain partly the rising costs and can discourage investors. The costs of SMR projects depend in part on the time required for obtaining authorisation and their implementation. Although estimated lead times from plant order to grid connection are typically around three years, the regulatory approval, permitting and stakeholder involvement to manage the policy and public opposition extends the actual project deadlines. A countless number of experts are calling for the establishment of a harmonised international regulatory system regarding the characteristics of SMRs. In fact, one of the main challenges for SMRs is the need to obtain design and operating licenses within a reasonable time and at an acceptable cost, both in provider and user countries. National nuclear regulators have different laws and approaches to licensing, leading to a lengthy and costly process.

Waste management is another identified challenge for the technology development. While according to research from Stanford and the University of British Columbia most SMRs might increase the volume of nuclear waste by 2 to 30 times compared to traditional reactors14, the promise of Gen IV reactors is expected to reduce waste. Some Gen IV designs, as ARC Clean Energy’s ARC-100, aim to use its own waste and recycle its own fuel, leaving almost no-long term waste, while also recycling waste from traditional reactors15. As well, the development of SMRs may increase the potential risks of waste proliferation (particularly plutonium) and necessitates enhanced training in nuclear safety and security for countries adopting SMRs to enter the nuclear power sector.

Conclusion

The SMR market is ultimately quite new, with only 4 operational units worldwide: in Russia and China. These units are Gen II reactor designs; in other words, a technology that could be improved to enhance safety, reliability and reduce costs. Gen II technologies are still being designed and developed, but primarily in those two countries. The world is now looking towards newer technology: Gen IV reactor designs.

Various demonstration projects are being led but also face significant difficulties; especially related to costs and technical challenges. If current trends persist, US (due to fundings expected to be allocated to the technology) and Chinese (thanks to political ambitions) designs could dominate the global SMR market in the upcoming decades. While it is difficult to assess the scale of potential demand-side subsidies for the domestic development and exports of China's nuclear sector, experts estimate that over the next 15 years, China could allocate between US$25bn and US$35bn for the deployment of the Linglong One reactor fleet, both nationally and internationally. This allocation includes mechanisms to reduce the cost of capital, which would be important for countries with higher credit risk. The export potential of Chinese large reactors and SMRs is estimated between US$140bn and US$150bn, implying the construction of 25-30 GW of capacity abroad. Other OECD countries should also provide greater support for SMR development. To allow the technology to evolve, new elements will be required, including: 1) supply and demand-side incentives and political backing, 2) collaboration among nuclear regulators to establish common standards, and 3) the formation of alliances between companies.

Notes

- Nuclear accidents: Tchernobyl: 1986 & Fukushima: 2011

- Argentina, Australia, Brazil, Canada, China, France, Japan, Korea, Russia, South Africa, Switzerland, the United Kingdom and the United States

- GIF Portal - Portal Site Public Home (gen-4.org)

- WoodMackenzie, 2024

- WoodMackenzie, 2024

- English think tank "New Nuclear Watch Institute"

- World Nuclear Industry Status Report, 2023

- UK Government, 2023

- NNWI, 2023

- Invest Korea, 2023

- Korea Times, 2023

- WNN. 2023

- French Government, 2024

- Stanford, 2022

- ANSTO, 2022