Smart grids are seen by many as an effective solution to address some of the toughest challenges the electricity industry has faced so far; the integration of renewables on a very large scale, the promised rise in number of electric vehicles, the necessity of energy efficiency, the improved security of supply or the arrival of the ‘prosumer’. Equipment manufacturers and IT solution providers are eagerly awaiting the hundreds of billions of euros to be invested over the next decades.

In this article, we advocate that smart grid technologies have the potential to transform the electricity markets given they are for the most part readily available, but, the correct regulatory framework first needs to be put in place. Failure to recognise the need for a regulatory overhaul can only hamper and delay the deployment of smart grids and their expected benefits.

From vertical integration to network unbundling

The present European electricity system is the result of a process that started shortly after World War II. National or regional vertically integrated monopolies rapidly became the dominant business model in the electricity industry. This model proved highly efficient in developing the numerous European electricity networks in times of vigorous growth.

To this day, the European electricity system has been characterised by a high degree of centralisation with mostly unidirectional electricity flows. In the current configuration, large-scale power plants generate electricity that is transported over long distances through a high voltage grid and distributed locally to end-customers through medium and low voltage distribution grids.

Following the market liberalisation experience initiated in the UK and the US in the 80’s and 90’s, continental European electricity markets have been progressively liberalised. The European Commission itself has pushed the European electricity supply industry towards unbundling through a series of Directives, the last of which - the so-called “third energy package” - came into effect in March 2011. As a result, European electricity systems now comprise a mix of regulated and competitive elements. Power generation, wholesale supply and retail supply have become competitive segments of the value chain while transmission and distribution have remained regulated businesses because of their natural monopoly characteristics.

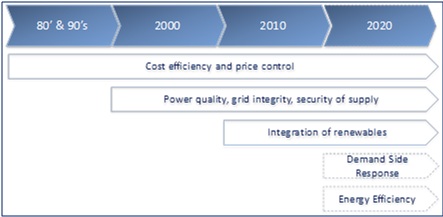

Evolution of network regulation objectives

Source: Enerdata

The primary objective of market liberalisation was to lower costs for users. Accordingly, the first regulatory phase that followed unbundling was geared towards a cost-efficient management of existing grids through the minimisation of operational expenditure (OPEX) and the rationalisation of investments. This economic objective was to be achieved without endangering the quality of power and the security of supply.

For regulators, the main challenge is how to introduce new objectives such as the integration of renewables on a large scale, the enabling of demand side response (DSR) and energy efficiency.