The Electricity storage and H2 electrolysis production momentum

Get this executive brief in pdf format

With the incorporation of Renewable Energy Sources (RES)1 into the power grids at a larger scale, and the phasing out of some flexible fossil fuel power plants, electricity storage solutions are surging strong to provide flexibility and balance electricity supply and demand. In addition, e-fuel and H2 generated from carbon neutral electricity, are expected to play a significant role in the decarbonisation of key energy systems such as transportation and industry processes. In this analysis we will focus mostly on Electrochemical Battery Energy Storage Systems (BESS), Pumped Hydro Storage (PHS) and H2 electrolysers. It is important to pinpoint that H2 electrolysis can be used as an electricity storage system (Power to H2 to Power) but only to a certain extent and most projects are focuses on the decarbonisation of other sectors.

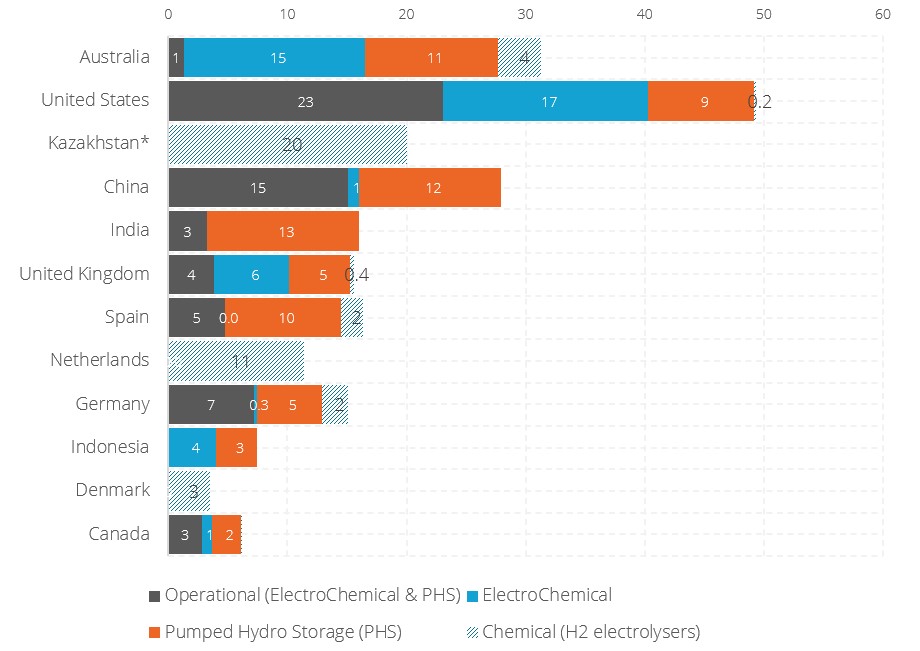

Australia and the US rise as leaders in terms of BESS and PHS project development with a pipeline comprising 26 GW of new capacity each. Australia is also expected to house some of the largest electrolyser projects announced to date.

The BESS market, although not included in most energy targets, rises as a key market with most projects proposed located in Australia, the US and the UK. Project configuration can be of standalone BESS our systems coupled with other technologies. Regardless of the configuration there is a clear preference for BESS < 50 MW and discharge durations of up to 4 hours. Within the residential sector, BESS development is driven by strong support schemes. This market is quite concentrated with companies like Tesla and LG holding the lion’s share of capacity additions in key geographical areas such as the US.

Meanwhile countries begin to publish their H2 strategies and some incorporate ambitious H2 electrolysis national targets that could result in over 110 GW of electrolysis capacity addition by 2030 (including EU, UK, Chilean and Colombian targets, China and Japan development estimates, and Indian tender ambitions).

RES here are considered all intermittent renewable technologies (mostly wind and solar).

ELECTRICITY STORAGE AND H2 ELECTROLYSIS PRODUCTION CAPACITIES: A PROJECT DEVELOPMENT PODIUM TAKES SHAPE

Regarding announced projects, Australia, and the US lead BESS and PHS project development announcements despite not having a national development target.

India and China run close, and the market awaits to see their development strategies unfold.

Australia is expected to house some of the largest RES projects built for green H2 production.

Total operational capacity of Electrochemical BESS and PHS varies from country to country. Australia for instance, despite so many project announcements, still only has around 1 GW of operational capacity2. Countries with significant operational capacity include the US (23 GW), China (15 GW), Germany (7 GW), Spain (5 GW), and the UK (4 GW).

Australia takes the lead in terms of project announcements even though no long-term national development target has been disclosed.

The Australian electricity storage project pipeline is huge and comprises 26 GW. Over half of the total is composed of ElectroChemical BESS projects. The country is one of the few that houses gigawatt-scale BESS projects, namely CEP Energy’s 1.2 GW Kurri Kurri (expected by end 2023) and SolarQ’s 1 GW regional energy hubs which total 3 GW of BESS capacity (Gympie Regional Energy Hub - Stage 2, Ipswich Regional Energy Hub, Wivenhoe Regional Energy Hub). Over 11 GW of the project pipeline comprises PHS including the 2 GW Snowy 2.0 expansion project, to be built at the existing Snowy Scheme (also known as Snowy Mountains scheme), a hydropower complex consisting of nine power stations with a combined capacity of nearly 4.1 GW.

Another major market for electricity storage development is the United States, which expects to add massive amounts of BESS (over 17 GW) including the 600 MW Morro Bay BESS (expected for 2024) and the 650 MW Swiftsure (2023) projects. The country also expects to develop various PHS projects including the 2.6 GW Halverson Canyon and the 2.2 GW Navajo Energy Storage Station. With BESS and PHS combined, up to 26 GW of capacity could be added (assuming 100% project completion rate), more than doubling the current 23 GW installed capacity.

Operational capacity is based on Enerdata’s Power Plant Tracker database which focuses on utility scale BESS in front-of-the meter. Coverage varies depending on the level of transparency of the countries’ Ministries and Energy agencies.

Although China seems to take the lead in terms of project development with a proposition to take the country’s BESS capacity to 30GW by 2025. Indian ElectroChemical storage deployment, however, accelerates to accompany RES. Recently the Solar Energy Corporation of India (SECI) issued plans to tender a 2,000 MWh standalone energy storage system following multiple renewable + storage tenders. In July, India’s largest utility, NTPC, launched an expression of interest (EoI) among Indian and global companies to build 1 GWh of grid-scale BESS at its power plants. The company aims to reach a 130 GW power generation capacity portfolio including 60 GW of RES by 2032.

The UK has also a substantial project pipeline of 11 GW that will almost triple the current capacity levels (at 4 GW).

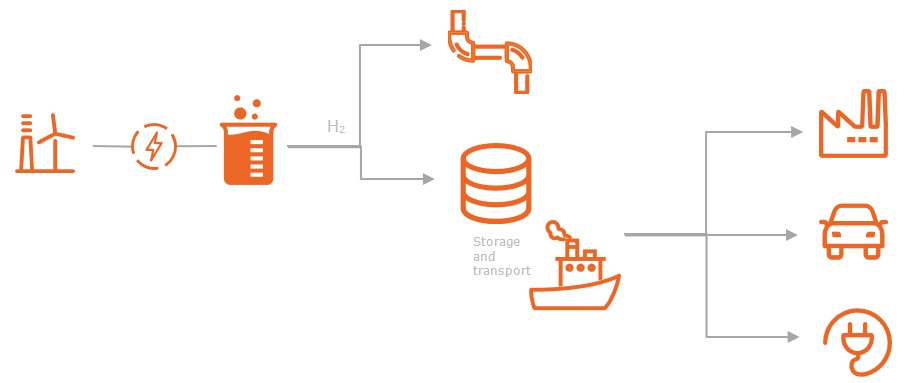

Beyond PHS and Electrochemical storage it is possible to analyse the development of H2 electrolysers, which can be used for power storage but mostly consist in a way to transform RES electricity into another energy carrier. It can also provide flexibility to the grid when the RES electricity is not consumed at times of peak RES intermittent generation. The development of these installations is marked by a clear ambition of decarbonising sectors such as industry (metal treatment, fertiliser production, food processing, etc.), and transport (in synthetic fuel production).

Regarding electrolysis capacity to produce green H2, multiple projects take shape in Australia. Beyond Stanwell’s 3 GW H2 electrolyser project in Aldoga, the country is also expected to house some of the largest RES projects targeted to produce power to generate green H2 (with exact capacities for electrolysis yet unknown). The Asian Renewable Energy Hub proposed by NW Interconnected Power (a consortium of CWP Energy Asia, Vestas, Pathway Investments and InterContinental Energy) will include 26 GW of RES capacity for green H2 generation and is expected to be operational in 2028. Meanwhile, the Western Green Energy Hub (WGEH) proposed by InterContinental Energy, Mirning Green Energy, and CWP Global will comprise 50 GW of RES capacity to produce 3,500 t/year of H2 and 20,000 t/year of ammonia.

In terms of H2 electrolysis capacity development in the US, no national strategy has been issued yet but multiple initiatives are emerging, and state-level targets can be expected.

Figure 1: Electricity storage and H2 electrolysis project pipeline and total current operational capacity by country and technology in GW

Source: Enerdata, Power Plant Tracker

This graph only includes announced projects and operational installations. Long term national development targets are not included. For an overview of national development targets see Enerdata’s country Energy reports.

*In Kazakhstan SVEVIND Energy announced a MoU with the Mangystau region to develop a 20 GW electrolyser for green H2 production, with a broader ambition to reach 30 GW countrywide. Being at very early stages of development, this project is not considered as a trend setter for now.

BESS PROJECTS: COUPLED OR NOT COUPLED?

Numerous Utility scale BESS projects emerge where the political framework is adapted

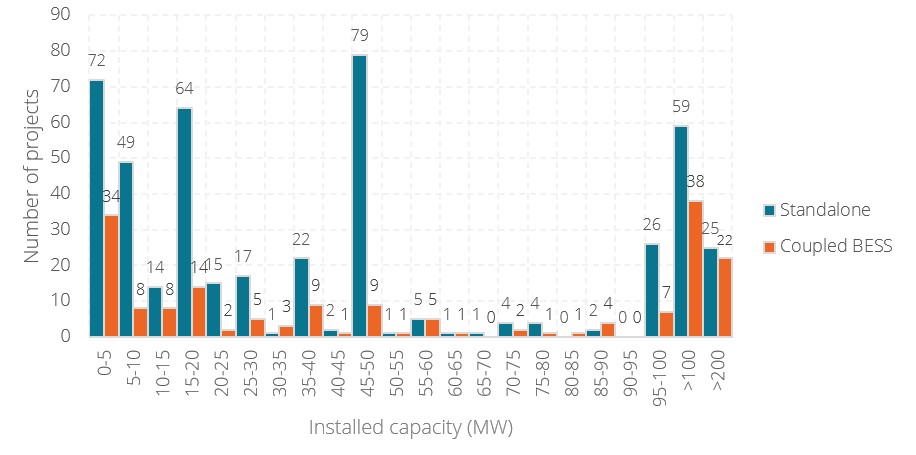

The project pipeline for utility-scale standalone BESS is three times larger than the one for coupled utility-scale projects.

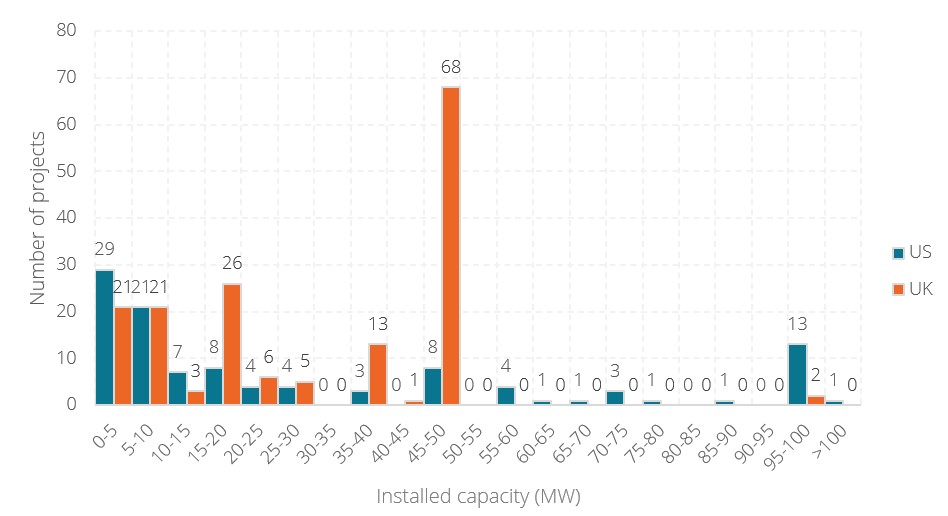

UK standalone projects tend to be of larger scale than in the US.

Although there is no doubt regarding the rise of utility scale BESS with increasing flexibility needs in power grids, very few policies state a clear target for BESS development capacity in the long term. The political framework focuses much more on explicit targets for RES development. That is why this section focuses on project announcements rather than national development plans.

According to Enerdata’s Power Plant Tracker3, almost 90% of utility scale BESS projects (mostly of electrochemical technology) are below 100 MW of installed capacity. A clear preference for projects ≤ 50 MW can be identified. Although discharge capacity is not often disclosed, project developers tend to propose BESS discharge durations of 1 hour, 2 hours and 4 hours. This is mainly because li-ion batteries dominate the market and are not yet competitive at higher discharge durations. Beyond standalone projects, projects coupled with other technologies (mostly renewables) are of a similar configuration with the bulk of the project pipeline being below 50 MW. Overall, the project pipeline for utility-scale standalone BESS is three times larger than the one for coupled projects. This is mostly due to the strong advancements of the political framework surrounding the incorporation of such systems into the grid and its remuneration in the top developing countries (namely US, UK and Australia). To some extent, it is also due to the extinction of existing RES supports such as Feed-in Tariffs (FiT), which reduces the economic benefit of coupled projects vs. standalone ones.

Figure 2: Distribution of utility-scale standalone and coupled BESS projects by installed capacity in MW (worldwide)

Source: Enerdata, Power Plant Tracker

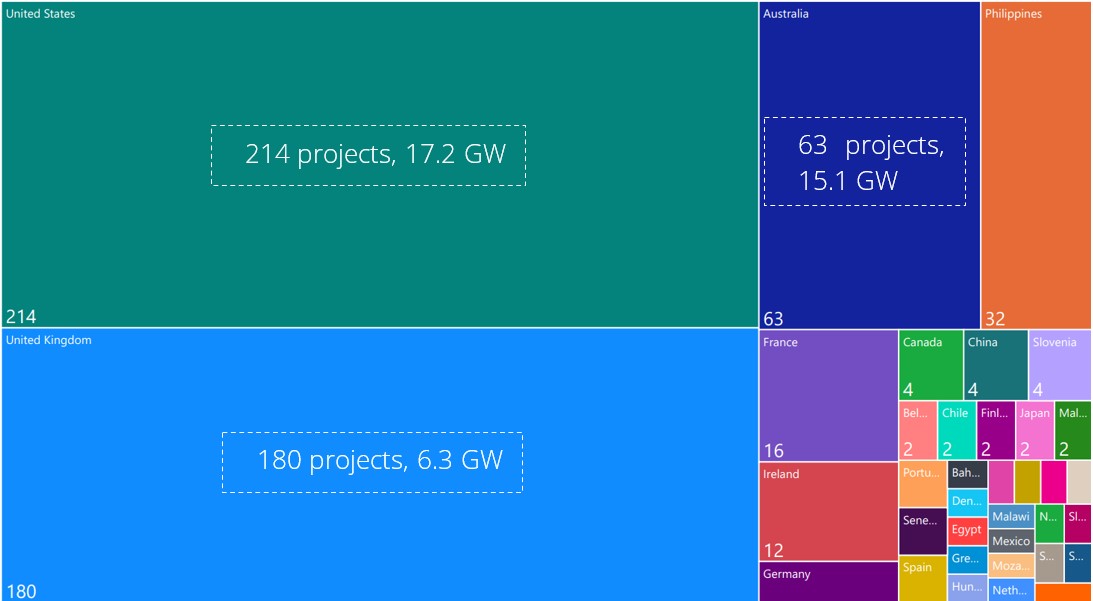

In terms of utility-scale Electrochemical BESS project development, three countries take the lead. The US has a project pipeline of over 200 plants totalling 17.2 GW of planned added capacity. Meanwhile larger scale projects expected in Australia (around 60 projects) will add over 15 GW to the grid, and in the UK, smaller, but numerous projects (180 plants), will help add over 6 GW of capacity to the grid.

Figure 3: Number of proposed electrochemical BESS projects by country and total expected capacity in MW

Source: Enerdata, Power Plant Tracker

Standalone project configuration is fairly different between the US and the UK. In the UK almost half of the project pipeline is between 45 MW and 50 MW of installed capacity. This is likely due to the Nationally Significant Infrastructure Project (NSIP) process which, until December 2020, demanded projects > 50 MW to obtain approval through the national planning regime which takes longer. With the Infrastructure Planning (Electricity Storage Facilities) Order 2020 passed into law, projects larger than 50 MW in England and larger than 350 MW in Wales were allowed to be processed through the local planning regime thus expediting licensing. Therefore, a change in the project pipeline can be expected in the upcoming years. In the US standalone BESS projects are usually of smaller scale, mostly below 20 MW. Around 60% of coupled projects in the US (over 50 projects) have BESS components below 50 MW. There are very few utility-scale BESS coupled projects in the UK.

Figure 4: Distribution of standalone BESS projects by installed capacity in MW (US & UK)

Source: Enerdata, Power Plant Tracker

The residential sector relies heavily on support schemes and is dominated by solar-coupled BESS deployment

In the US the attachment rates of newly added solar in households reached 8% driven by FiT and net metering support schemes.

The residential market is highly concentrated with Tesla and LG systems taking a large portion of new additions.

In Australia, solar + storage system additions rose by over 17 times between 2015 and 2020.

In Europe, Germany is responsible for two thirds of residential BESS additions.

In 2020 around 3.2 GW of new BESS was installed in the US, 30% of which was of behind the meter systems including half of those systems paired with solar4. In the US the adoption of solar + storage systems increased in all sectors but especially in the residential sector5. Estimates indicate that the attachment rates (level of new systems with an attached BESS) in this sector rose to 8.1% of newly added solar capacity, from virtually 0% in 2015. 80% of the current BESS residential installations are paired with solar as the national solar Investment Tax Credit (ITC) and the net energy metering (NEM) support schemes provide higher revenues. The residential market is dominated by 2 battery models: the 5 kW / 13.5 kWh Tesla Powerwall and the 5 kW / 9.3 kWh LG Chem RESU (each company holding around 20% of the market share) although systems over 5 kW are becoming more common (40% of the added capacity in 2020).

In Australia the amount of small-scale renewable systems with coupled BESS has been consistently increasing. Yearly additions went from almost 550 systems/year in 2015 to almost 9,500/year in 20206.

In Europe, Germany, Italy, and the UK were responsible for 90% of new BESS installations in the residential sector which reached 350 MWh (around 2% of all home solar systems)7. In 2018 up to 65,500 residential BESS were added totalling 505 MWh with other markets such as Austria, France, and Switzerland witnessing strong development. In 2019, as European total additions reached 745 MWh (63,000 systems added), Germany held two thirds of the market with Italy, UK, Austria, and Switzerland adding to 25%. Attachment rates for newly added solar are higher in Europe’s main markets when compared to the US, in Germany this rate was 17% in 2019, and in Austria 16%.

GREEN H2: MORE THAN ELECTRICITY STORAGE

H2 production emerges as a very flexible energy carrier solution for a decarbonised world.

Ambitious H2 electrolysis national targets foresee over 110 GW of capacity addition by 2030 (including EU, UK, Chilean and Colombian targets, China and Japan development estimates, and Indian tender ambitions).

This section focuses mostly on the long-term development targets rather than individual projects.

Green H2 has emerged as a key energy carrier to decarbonise several key sectors and end-uses. Many national decarbonisation strategies rely on a strong development of green H2EnerFuture’s EnerGreen) foresees that green H2 could account for 2% of global energy consumption in 2050 and up to 7% of total energy consumption of the transportation sector.

H2 produced via electrolysis can be stored and transported to be used as chemical feedstock in multiple industries (metal treatment, fertiliser production, food processing, etc.), for synthetic fuel production, as fuel for transportation vehicles, or it can be converted into power again using fuel cells, internal combustion engines, and gas turbines. It can also be directly injected into the heating network.

Source: Enerdata

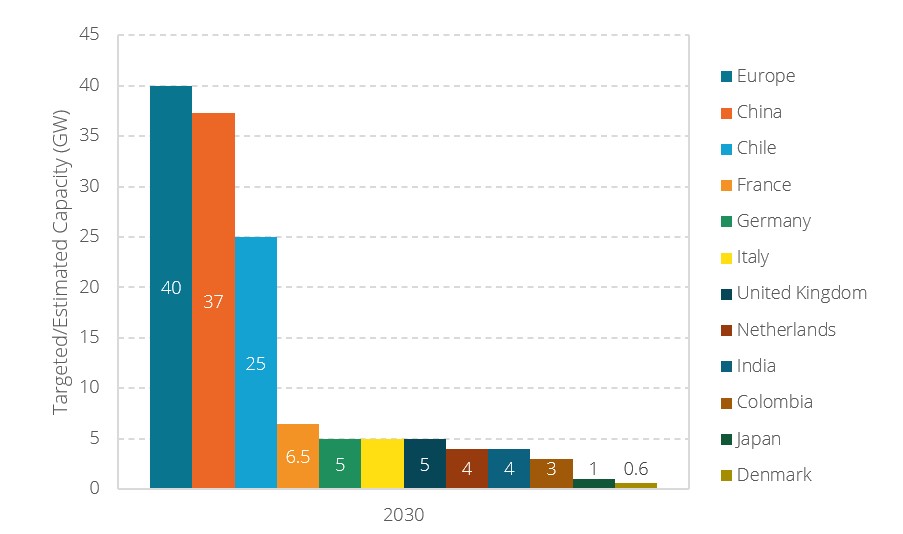

Although major players have not yet set up objectives (US, Australia, China, and India), Europe is taking the lead with an objective of 40 GW of electrolysis capacity by 2030. The main targets announced (namely by: Chile, EU, and the United Kingdom) sum up to 70 GW of electrolysis capacity by 2030. The UK, Germany, and Italy each set 5 GW of capacity as their goal for 2030 and Germany will double this capacity by 2050. France is also planning on adding 6.5 GW in this timeline.

It is also estimated that major players such as Japan and Denmark could require up to 1 GW8 and 580 MW9 of electrolysis capacity, respectively, to meet their foreseen green hydrogen needs. Meanwhile, The Indian Power Minister revelled plans to launch a 4 GW tender for green electrolysers (likely to be developed within the decade) which should occur before end 2021. In China, estimates indicate that the current 0.7 GW electrolysis capacity could jump to 8.1 GW, 38 GW, 608 GW and 930 GW respectively in 2025, 2030, 2050, and 206010.

Figure 5: H2 electrolysis capacity targets/estimates

Source: Enerdata, based on countries’ H2 strategies, expert estimates, and recent tender announcements.

Take aways

- The road towards a decarbonised economy will be strongly supported by the development of new technologies:power storage systems, especially BESS to provide flexibility and green H2 to decarbonised key energy end-uses.

- Project development for Electrochemical BESS and PHS is clearly led by Australia and the US, with a 26 GW pipeline each and strong expectations on the reduction of electricity storage installation costs.

- The UK and the US currently propose most of the inventoried BESS projects in terms of number of projects.

- The residential BESS development in the US, Australia and European countries is driven by adapted support schemes and new systems are rarely standalone.

- The residential market is highly concentrated. In the US, Tesla and LG hold 40% of residential market.

- Ambitious H2 electrolysis national targets foresee over 110 GW of capacity addition by 2030 with Europe being responsible for most pledges.

Notes:

- RES here are considered all intermittent renewable technologies (mostly wind and solar).

- Operational capacity is based on Enerdata’s Power Plant Tracker database which focuses on utility scale BESS in front-of-the meter. Coverage varies depending on the level of transparency of the countries’ Ministries and Energy agencies.

- Based on individual projects for an overview of national development targets see Enerdata’s country Energy reports.

- BERKELEY 2021a

- BERKELEY 2021b: Residential: Single-family and, depending on the data provider, may also include multi-family

- CER 2021

- SolarPower Europe (2020)

- METI Ministry of Economy 2020

- Fuel Cells and Hydrogen Joint Undertaking (FCH JU) 2020

- National Press (2021)