What future for coal in Asia?

Request this Executive Brief in PDF format (FREE)

Coal in Asia - A historical central role in the region’s economy

As the global energy transition accelerates, Asia stands at a critical crossroads where economic momentum meets climate urgency. This brief analyses why coal remains so deeply embedded in the economies of China, India, Indonesia, and Japan—four nations that control the majority of the global coal value chain. By exploring the tension between energy security, industrial growth, and net-zero ambitions, this analysis identifies the structural barriers and strategic shifts defining the region's path toward a lower-carbon future.

Coal in Asia - A historical central role in the region’s economy

Four countries drive global coal demand

Global coal consumption has doubled over the past forty years. Over the last decade, despite the proliferation of climate commitments, consumption has remained stable at its historical peak. The efforts made by some nations are offset by 4 Asian countries, key players of the entire coal value chain: China, India, Indonesia, and Japan.

In 2025, China (52%), India (11%) and Indonesia (9%) collectively drove 72% of global coal production, despite holding just one quarter of the world’s proven reserves. Trade dynamics are equally concentrated, with Indonesia acting as the leading global exporter and Japan as a highly advanced, technology-driven importer.

Power generation and heavy industry are the main sectoral drivers of coal use

Coal has historically represented up to 70% of the primary energy mix in China, and up to 45% in Indonesia and India.

Power generation is the leading coal sector across all four countries: accessible and cheap domestic resources explain the cases of China, India and Indonesia. Japan, on the other hand, has strategically favoured coal as a baseload fuel for its electric industry following the 70s oil shocks and more recently the Fukushima incident. A secure baseload is essential for Japan, whose high-tech industry (automotive, electronics, robotics) requires a cheap and all-day electricity supply.

On the other hand, coal critically supports heavy industries, both as a fuel providing a high-temperature input (>1000°C) and as a feedstock in some cases (iron reduction in the steel industry, limestone calcination in the cement industry). The historical rise in the coal demand is therefore both an enabler and a consequence of the major economic development observed in China and India over the past twenty years.

To a lesser extent, coal remains a prevalent space-heating fuel in Northern Chinese buildings and in India (~8% of buildings final consumption in both countries in 2022, compared to up to 30% in China in the early 2000s).

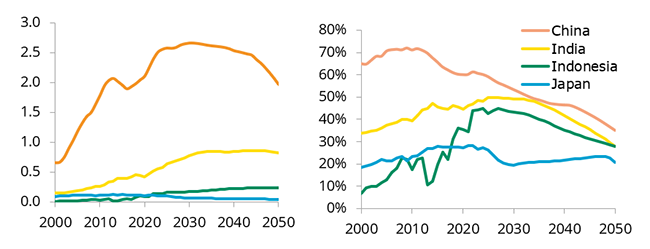

Under EnerBase’ business as usual trajectory, coal’s relative share in the energy mix may dip, yet absolute consumption remains stubbornly high

The EnerBase scenario explores the evolution of energy demand, assuming the continuation of established policies and historical demand drivers. In such scenario, the share of coal in the primary energy keeps growing in India and Indonesia, driven by industrialisation and rising power demand sustained mainly by coal-fired power generation. From 2030 onwards, a downward trend is observed in all four countries thanks to the implementation of existing policies. However, these declining shares of coal still translate into a flat or increasing coal demand in a context of rapid economic growth (except in Japan).

Figure 1: Coal primary consumption (left) and share of coal in primary energy consumption (right) - EnerBase

Source: Enerdata, EnerFuture, POLES-Enerdata Model

In power generation, renewables are expanding, driving coal capacity to peak before 2030 in China and Japan—where nuclear is also taking a growing share. For India, this milestone will only occur after 2035, while coal capacity grows until 2050 in Indonesia: coal remains a long-term security fuel in China and India, a grid stabiliser in Japan and a sovereignty issue for Indonesia.

Indonesia is a textbook case of an environmental paradox: the nickel industry is critical to the transitioning global economy and especially EVs battery manufacturing. Yet, it strongly relies on coal, thus driving the construction of captive coal plants. Other coal lock-ins are noted in the so-called hard-to-abate industries, currently dependent on coal with only few mature alternatives.

Overall, EnerBase tendential projections therefore show that coal consumption could remain high despite slightly declining shares in the primary mix, confirming coal’s central -and historical - role in the region’s economy, provided no additional effort is made toward a phase out.

EnerBlue: How to dissociate economic prosperity from coal dependency?

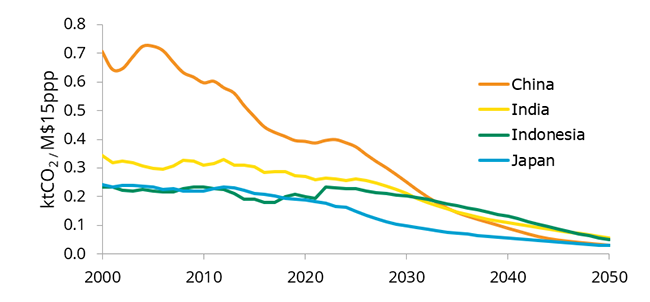

All four countries have committed to Net Zero emission goals, planned from 2050 (Japan) to 2070 (India). These involve the design of a whole framework of policies aiming at reducing carbon intensive resources from the countries’ energy mix and/or substituting them with renewable or less emissive resources. In addition, intermediate targets have been set for 2030 to keep track of the progress. Considering the current heavy economic reliance on coal demonstrated above, are these goals reachable? In other words, is the tension between sustaining economic momentum and meeting climate commitments defining the future of energy in Asia? The EnerBlue scenario offers insights on what the future energy demand could look like if the countries have deployed policy instruments to reach their ambitious targets. Emissions decrease sharply, progressively decoupling from GDP as these countries increasingly shift away from coal. This trend is driven by improvements in energy efficiency, greater electrification, and the expansion of renewable power sources. The emission intensities of population of Indonesia and Japan synchronise, while China and India reach even lower values.

Figure 2: Emission intensity of GDP - EnerBlue

Source: Enerdata, EnerFuture, POLES-Enerdata Model

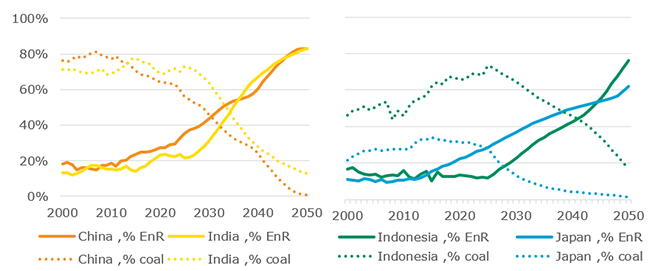

Power sector emissions decline as renewables displace coal as the leading power generation source

In the power sector, two distinct trends are emerging regarding how these four countries manage the coal issue: on the one hand, Japan and Indonesia focus on the retirement of coal assets. In Japan, the 6th Strategic Energy Plan mandates the "decommissioning of inefficient coal-fired power plants" by 2030. By 2040, the coal baseload will be replaced with a diversified mix of nuclear (20% of power generation) and low-carbon technologies: coal super-critical plants retrofitted for ammonia co-firing, and renewables covering 40-50% of power generation. Similarly, Indonesia has pledged to phase-out coal, leveraging schemes like the Just Energy Transition Partnership (JETP) or the Energy Transition Mechanism (ETM) designed to finance early retirement (e.g., the Cirebon-1 pilot, scheduled to close 10 to 15 years before its technical end-of-life). However captive coal plants dedicated to the nickel industry are so far exempt from phase-out pledges.

Conversely, China and India have adopted a different approach, prioritising economic and energy demand growth over an early coal phase-out, as both nations are still experiencing a 4-6% annual demand growth. In India, where coal is viewed as essential for energy security, the strategy shifted from a “phase-out” to a “phase-down” of coal – a stance ratified during COP26. Meanwhile, large-scale renewable capacities are installed to meet the new electricity demand and progressively curb the share of coal in power generation. Existing coal capacities will remain in place as backups for high-load times, meaning their load factors are expected to steadily decrease in the coming years. China is slightly ahead of India in this phase-down process, having already reached peak coal consumption in 2025. The transition from coal to renewables as the dominant power source is well underway, driven by massive targets—such as reaching 3,200 GW of wind and solar capacity by 2035—and materialised by mega-projects like the Gobi Desert renewable hub.

Ultimately, the rapid decline in power emissions demonstrates that targeted policy mechanisms are highly effective in the electricity generation sector.

Figure 3: Shift from coal to renewables in power generation - EnerBlue

Source: Enerdata, EnerFuture, POLES-Enerdata Model

Industrial emissions are harder to abate and persist

The narrative is different for industrial emissions: these remain flat in the projections, except for China, which sees a relative decline. Several schemes are set to decrease industrial coal emissions: China and Japan use market-based pricing by including high-carbon coal generation and industrial use in their national ETS. In addition, China’s Carbon Dual Control system specifically targets coal displacement in steel and cement, while ultra-high voltage grid expansion aims to convey low-carbon electricity from the western to the eastern, industrial part of the country. India targets inefficient coal plants in cement, steel and thermal power, and bets on the National Green Hydrogen Mission to displace coal in heavy industry, notably steel (Hydrogen-DRI) and fertilisers. Yet, the young nature of China or India’s industrial fleet make for a slow decline in coal consumption, since assets are used until the end of their economic life. Furthermore, innovative technologies lack scalability to ensure a rapid decarbonisation of the industry in the medium-term.

Moving away from a coal-heavy system, in alignment with stated policies, creates financial, technical and socio-economic challenges. The friction between the sustainability, security and equity pillars of the energy trilemma must be addressed to turn these targets into reality.

Significant challenges to exiting coal

High CAPEX costs and stranded asset risks create financial barriers

As stated above, the early phase-out of coal-fired power and industrial plants is a requirement for net zero pathways. However, this transition poses a formidable challenge for emerging economies like China, India, and Indonesia. Their coal fleets are relatively young, and an accelerated phase-out entails significant stranded asset risks, as plants would be retired 15 to 20 years before the end of their economic life. Financial viability issues arise for both plant owners, who must repay long-term loans, and utilities bound by take-or-pay contracts. This raises the critical question of funding: should companies and utilities bear the entire burden, should the state subsidize the phase-out, or should the international community help fund it, as envisioned by Indonesia’s Just Energy Transition Partnership (JETP)?

Furthermore, large-scale renewable expansion is highly capital-intensive (high CAPEX). When coupled with the high interest rates these emerging countries face on international markets, the financial burden becomes twofold—especially for nations that currently benefit from cheap, domestic coal reserves. Ultimately, a balance must be struck between immediate access to affordable energy and the long-term costs of decarbonization.

Grid stability limits and industrial "lock-ins" limit the pace of coal phase-out

Shifting from baseload coal to intermittent renewables requires specific strategies to ensure grid stability during peak power demand. The rising cooling demand in India, coupled with generalized electrification creates challenges that are yet to be fully addressed through storage, low-carbon backups or demand-side management. Moreover, island nations like Japan and Indonesia face unique geographical challenges. These limit the feasibility to building grid interconnections between power production and consumption centres, as envisaged in China with the West-to-East power transmission strategy. In Indonesia, new and future captive coal plants cannot easily be replaced with geothermal or hydropower, whose resources are located on different islands from the nickel smelters. Hence, local resources like coal are favoured and become the default choice to meet grid congestion issues. For net importers like Japan, coal-to-gas switching relying on LNG imports becomes a viable short to medium term alternative to reduce power sector emissions.

Just transition and geopolitical concerns slow down phase-out ambitions

Finally, beyond purely economic concerns, the central role of coal poses significant local challenges. Coal industries are major employers, generating revenues that fund regional wealth and infrastructure development. Consequently, decommissioning plants without providing alternative economic activities or compensation could severely impact affected communities. This may trigger social unrest and political instability in regions such as Kalimantan in Indonesia, or Jharkhand and Odisha in India.

From a macroeconomic perspective, the ripple effects of national policies on the broader coal value chain must be carefully considered. As the world's largest coal exporter (accounting for about 50% of global seaborne coal trade), Indonesia heavily relies on top clients like India, China, and Japan. A coal phase-out in these client countries would pose a severe economic risk to exporters, driving down both demand and revenues. Conversely, a domestic coal phase-out in Indonesia could undermine the country's industrial competitiveness, as current substitutes remain more expensive. To safeguard its domestic industry, Indonesia recently enforced a Domestic Market Obligation (DMO), requiring producers to sell at least a quarter of their coal domestically at a capped price. While such mechanisms favour economic equity, they risk undermining renewable expansion and slowing down the energy transition. Furthermore, the European CBAM will eventually impose carbon taxes on Indonesian ferronickel and batteries if they fail to meet the scheme's carbon intensity thresholds.

Additionally, as nuclear plant restart and expansions often come with unexpected delays, Japan may have to rely on coal and LNG imports for energy security longer than anticipated. Although coal-to-gas switching has already been observed, tight LNG supplies and price volatility in the current geopolitical context could trigger a reverse 'gas-to-coal' shift, further delaying the phase-out process. The ongoing conflict in Iran and associated supply disruptions (e.g. damages on the Ras Laffan LNG terminal) could indeed jeopardize the trends in coal-to-gas switch.

The need for a coordinated transition

The risks identified in this section should not be seen as insurmountable barriers, but rather call for proactivity, planning, integrated policy frameworks and regional cooperation. Initiatives such as the GX-ETS in Japan, the JETP in Indonesia or the Production Linked Incentive (PLI) in India are paving the way for new, coal-free and more sustainable value chains. These frictions can drive innovation and establish the countries’ industrial leadership on hydrogen-DRI technologies, ammonia-cofiring, large-scale CCUS… From an energy security perspective, renewables and fossil-free sources offer the safest and most resilient path toward energy access and sovereignty.

KEY TAKEAWAYS

- Coal is fundamental to Asian energy security and economic expansion, driving both baseload power and heavy industry.

- Coal phase-out relies on diverging strategies: Japan and Indonesia focus on the early retirement of coal assets through decommissioning and international financing, whereas China and India prioritize a "phase-down" approach through massive deployment of renewable capacity while keeping coal as a strategic backup for energy security.

- The transition is hindered by significant challenges, including the financial risk of stranded assets, grid stability issues with intermittent renewables, and the socio-economic necessity of a "Just Transition" for regions whose economies rely on coal mining and exports.

- A successful phase-out is contingent on a coordinated effort to manage the financial burden of the world's youngest coal fleet and to accelerate the deployment of large-scale industrial technologies for the "hard-to-abate" sectors.