Where does the region stand on its renewables and energy efficiency objectives?

Request this Executive Brief in PDF format (FREE)

In October 2025, the 43rd ASEAN Ministers on Energy Meeting (AMEM) endorsed the ASEAN Plan of Action for Energy Cooperation (APAEC) 2026-20301. As part of the plan, the ASEAN countries have collectively set ambitions to achieve a 30% share of Renewable Energy (RE) in total primary energy supply (TPES) and a 45% share of RE in installed power capacity by 2030. In addition, the region aims to achieve a 40% reduction in energy intensity (EI) based on TPES by 20302, compared to 2005.

Previously, in 2015, the ASEAN member states agreed under the APAEC 2016-20253 to reach a 23% share of RE in total primary energy supply (TPES), a 35% share of renewable energy in installed power capacity by 2025, and a 32% reduction in energy intensity by 2025 based on 2005 levels.

These targets are set in a context where the region is experiencing rapid economic development (GDP: +4%/year) and a fast increase in final energy demand, with a growth rate of 3%/year over the last decade, driven by a rising population and manufacturing expansion. By 2030, ASEAN aims to become the world’s fifth-largest economy4.

This brief examines ASEAN countries’ achievements of their 2025 regional targets and the ambition of their 2030 objectives compared with our EnerFuture scenarios and past trends. This analysis is based on data extracted from our Energy and Climate Country Reports, which compile key insights from the full Enerdata platform. This analysis highlights that the region has underachieved its 2025 objectives, and that its 2030 targets would require a rapid acceleration of renewable installations and energy efficiency improvements.

The ASEAN has likely missed two of its 2025 energy targets

Leveraging Enerdata’s Global Energy & CO2 Data database, this section studies how ASEAN has fared in terms of decarbonising its primary energy mix, increasing renewables capacity, and improving energy efficiency.

Coal covered most of the recent increase in energy demand

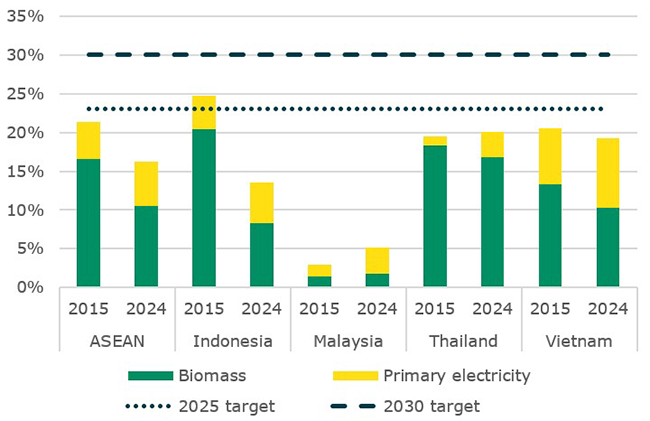

ASEAN member states are targeting a 23% share of renewables in primary energy consumption by 2025 and a 30% share by 2030. The 2025 target is unlikely to be met as the share of renewables in primary demand fell from 21% in 2015 to 16% in 2024.

Figure 1: Share of renewables in primary energy supply

Source: Enerdata, Global Energy & CO2 Data

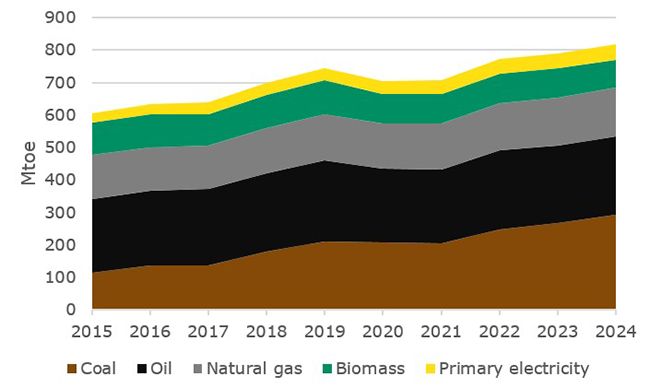

In a context where primary energy consumption in ASEAN grew by 40% between 2015 and 2024 to 817 Mtoe, most of the increase in demand was met by coal (84%), followed by primary electricity (8%), oil (8%), and natural gas (7%). Meanwhile, consumption of biomass, which is statistically classified as renewable even in its traditional form, recorded a decline.

The driving forces behind this increase in energy consumption in ASEAN were Indonesia and Vietnam, which accounted for 53% and 27%, respectively, of the additional energy consumption in ASEAN over 2015-2024. They represented 64% and 22%, respectively, of the increase in coal demand at the regional level between 2015 and 2024.

Figure 2: Primary energy demand in ASEAN, 2015-2024

Source: Enerdata, Global Energy & CO2 Data

The ASEAN may reach its renewable capacity target thanks to Vietnam

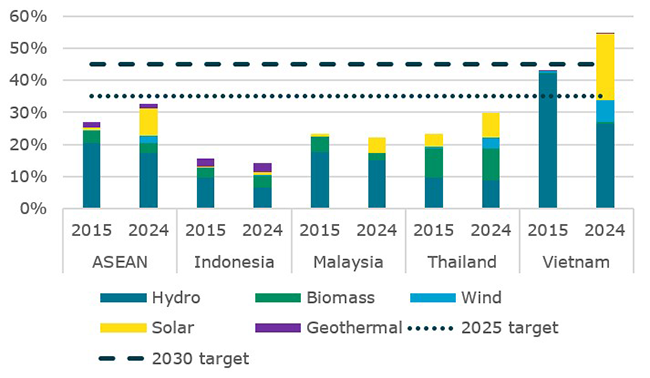

The region aims to achieve a 35% share of renewables in its power capacity mix by 2025 and a 45% share by 2030. Between 2015 and 2024, the share of renewables in the ASEAN’s total capacity increased from 27% to 33%. The region is close to reaching its 2025 target.

Figure 4: Share of renewables in total capacity

Source: Enerdata, Global Energy & CO2 Data

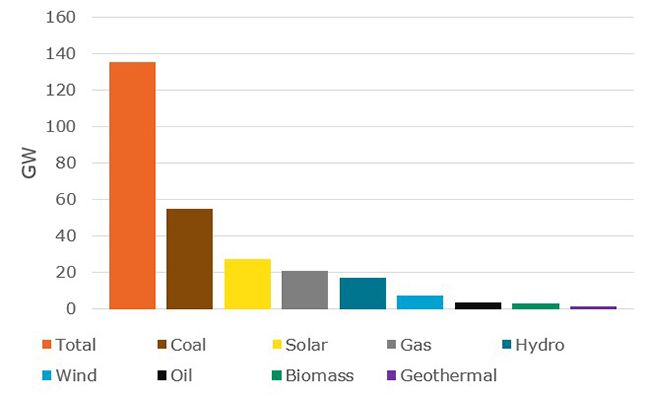

Between 2015 and 2024, the region added 135 GW of electricity capacity, including 56 GW of renewables – primarily 27 GW of solar and 17 GW of hydro – and 79 GW of fossil fuel-fired power plants (split between 55 GW of coal and 21 GW of gas).

Vietnam was the dominant driver of renewable expansion, accounting for 57% of the region’s additions, significantly outpacing Indonesia’s 10% share. Meanwhile, these two countries also led fossil fuel capacity expansion, with Indonesia contributing 48% and Vietnam 23% of the total additions in this segment.

Figure 5: Added capacities in ASEAN, 2015-2024

Source: Enerdata, Global Energy & CO2 Data

Since 2005, energy intensity has improved by a quarter

Countries in the ASEAN region intend to reach a 32% reduction in energy intensity by 2025, based on 2005 levels, and a 40% reduction by 2030. In 2024, energy intensity in ASEAN was 25% lower than in 2005, slightly underachieving the regional objective for 2025. This fall was driven by the residential sector, with a 63% drop over 2005-2024, while the decline was more limited for industry (-25%) and transport (-16%).

At the national level, the performance in terms of energy efficiency has been quite uneven among ASEAN member states. In 2024, Malaysia’s and Indonesia’s energy intensities were 33% and 29% lower than in 2005, respectively. Thailand was close to the regional average with a 22% reduction over 2005–2024, while Vietnam cut its energy intensity by only 4% over the same period, in a context of rapid industrialisation and growing energy demand.

New regional objectives require a significant effort in terms of renewables development

This section analyses the ambition of ASEAN’s new 2030 targets in terms of decarbonising its primary mix, increasing renewable capacity, and improving energy efficiency, comparing them against Enerdata’s EnerFuture scenarios, national plans and historical trajectories.

Three scenarios are used to contrast ASEAN’s 2030 targets with their projected trajectory: EnerBase, our business-as-usual scenario; EnerBlue, a scenario accounting for Nationally Determined Contributions and other national pledges at the end of 2024; and EnerGreen, a scenario aligned with the Paris Agreement. This brief uses our scenarios for Indonesia, Malaysia, Thailand, and Vietnam as a proxy for ASEAN. These four countries accounted for 82% of ASEAN’s primary energy demand in 2024.

The target for renewables in the energy mix is slightly above NDCs trajectory

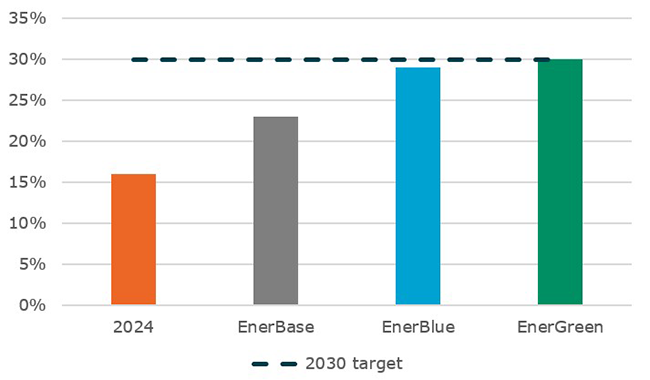

The share of renewables in primary energy supply in ASEAN reaches 23% in our EnerBase scenario, 29% in our EnerBlue scenario and 32% in our EnerGreen scenario by 2030. Set at 30%, the regional target for 2030 seems relatively ambitious, situated between our scenario accounting for NDCs and our scenario in line with the Paris Agreement.

Our EnerBlue scenario takes into account achievement of new NDCs, and national pledge submitted up to end of 2024. Since then, Indonesia and Vietnam, two of the largest regional economies, have released new plans: Jakarta has watered down its objectives in terms of renewables, while Hanoi has reinforced its ambition.

Figure 6: Share of renewables in primary energy supply in ASEAN in 2030

Source: Enerdata, EnerFuture

Regional renewable capacity objective is ambitious and requires a significant effort

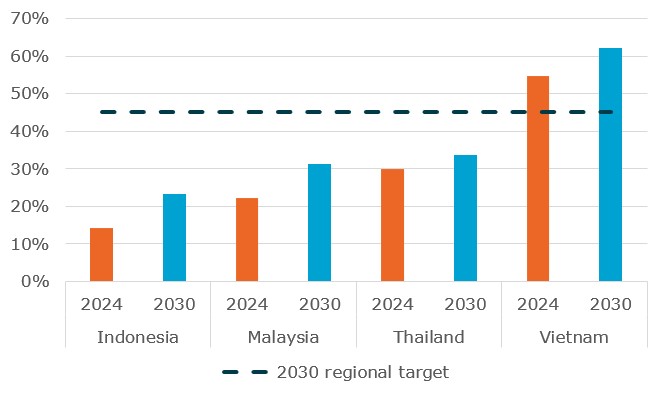

The regional target of 45% renewables share in total capacity seems largely in line with targets set at the country level.

Indonesia5, Malaysia6, Thailand7 and Vietnam8 plan to add around 190 GW of capacity over 2025-2030, including 120 GW of renewables when taking into account national plans and targets for power capacity.

This translates at the regional level to an estimated share of renewables in total capacity of 44% if each country realises its objective, according to our calculations based on national planning documents.

Figure 7: Share of renewables in capacity mix in 2024 and 2030 targets

Source: Enerdata, Energy and Climate Country Reports

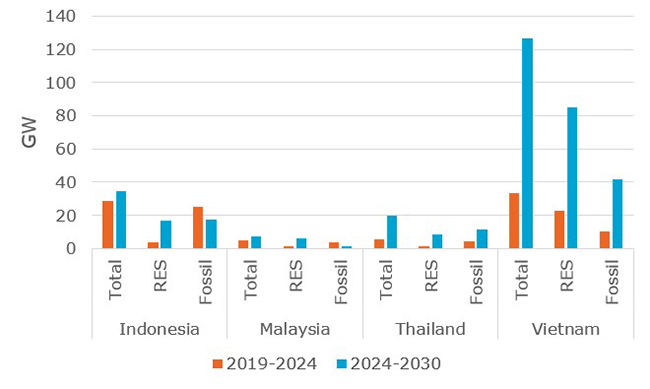

But how realistic is this objective for 2030? When comparing with historical trends, the region will have to install 3 times more capacity over the 2024-2030 period than it did between 2019 and 2024. For renewables, capacity additions must quadruple compared to the previous period.

In addition, most of the capacity additions will depend heavily on Vietnam. The country, which has an ambitious capacity development plan, should account for 73% of capacity additions over 2025-2030 at the regional level, and 59% of renewables capacity additions. Indonesia, Malaysia and Thailand anticipate a more limited growth in capacity.

The scale and ambition of targets for Vietnam raise questions about their realism, which could hamper the realisation of the 2030 regional target. Renewables objectives in Indonesia, Malaysia and Thailand also require a significant effort: those countries will have to multiply their capacity additions by at least 5 between 2025 and 2030 compared to the last six years.

Figure 8: Historical and projected capacity additions over 2019-2024 and 2024-2030

Source: Enerdata, Energy and Climate Country Reports

Energy efficiency improvement target is quite unrealistic in comparison with past trends

The region aims for a 40% reduction in primary intensity by 2030 compared to 2005 level. Between 2019 and 2024, primary energy intensity decreased by 1.1%/year and in 2024, it was only 25% lower than in 2025. ASEAN countries will thus have to accelerate energy saving efforts (3.5%/year reduction between 2024 and 2030) to meet this 2030 target.

Although ASEAN countries have developed energy efficiency policies, implementation remains uneven and constrained, in a context where most gains remain driven by technology. Weak policy frameworks, limited political commitment, and insufficient funding are likely to hinder progress, making any significant acceleration in energy efficiency improvements over 2025-2030 appear unrealistic.

CONCLUSION

In conclusion, the ASEAN has missed its 2025 objectives in terms of renewables in primary mix, as most of the new demand over last decade was covered by coal, and energy efficiency. However, the goal in terms of renewables may be achieved thanks to a strong increase in solar capacity in the last 5 years, especially in Vietnam.

Regarding the 2030 objectives, they appear to be quite ambitious in relation to past trends, especially for renewables capacity and energy efficiency, which puts their realism into question.

A key bottleneck for the development of renewables in ASEAN has been the level of investment. According to a recent report released by the ASEAN Centre for Energy, “ASEAN mobilised only USD 30 billion in energy investment in 2021, indicating the huge financial gap of around USD 170 billion in annual required energy investment by 2030”. Moreover, almost all energy investments tend to go to fossil fuels. rather than renewables

In addition to renewable capacity, there is also a major challenge in modernising grids so they can integrate more renewables; they were built for centralised, fossil-fired power plants and lack the flexibility to integrate intermittent energy sources. The geographical specificities of archipelagic countries, such as Indonesia and the Philippines also constrain the capacity of power grids. In the short run, the deployment of BESS could help integrate more renewables.

Several programs have been launched at the regional level in the field of energy efficiency, such as the ASEAN Energy Efficiency Database and Investment Platform for buildings, but they appears to be limited in scope and funding.

Recent initiatives have been put in place to tackle this issue. ASEAN has recently released a green taxonomy, which aims to promote sustainable investments. The regional body also launched a program named the ASEAN Power Grid (APG). It aims to establish an integrated power grid at the ASEAN level by 2045, which would facilitate the integration of renewables into the power system.

Finally, Indonesia and Vietnam, which are large fossil fuel consumers and accounted for most of ASEAN’s energy demand increase in the recent decade, have officially joined Just Energy Transition Partnership (JETP) with international partners to secure financial and technical support to move away from coal dependency and develop renewables.

KEY TAKEAWAYS

- ASEAN has missed its 2025 energy targets, except for renewable capacity, as the power system is decarbonising faster than the entire energy system.

- ASEAN’s 2030 energy targets are ambitious and require a significant effort to achieve.

- A key factor for ASEAN to achieve those objectives is the level of investment, which is currently lagging behind and too oriented towards fossil fuels.

Notes:

- aseanenergy.org/publications/asean-plan-of-action-for-energy-cooperation-apaec-2026-2030/

- Energy intensity is the amount of energy required to generate one unit of output, here expressed as the amount of primary energy used per unit of GDP.

- ASEAN Plan of Action for Energy Cooperation (APAEC) 2016-2025 - Phase I: 2016-2020

- ASEAN Sets Path Towards Becoming the World’s Fourth-Largest Economy with Release of AEC Strategic Plan 2026 – 2030

- Indonesia’s RUPTL 2025-2034: Fossils first, renewables later

- Malaysia’s National Energy Transition Roadmap

- Resolution of the National Energy Policy Committee meeting, Meeting No. 4/2024 (Meeting No. 170)

- Adjustments to the National Power Development Plan for the Period 2021-2030, with a Vision to 2050