Macroeconomics impacts of shale gas extraction and Mitigation of Climate impacts of possible future shale gas extraction in Europe.

Enerdata's Global Energy Forecasting team contributed with POLES modelling of EU and global scenarios for the reports of two DGs of the European Commission (CLIMA and ENV) together with ICF (lead) and Cambridge Econometrics using different assumptions on domestic EU shale gas (provided by ICF): resource levels, production costs, risk management option costs. Enerdata studied the effects on the domestic production level, the needs for imports and the impacts on the prices of commodities. CE provided the macroeconomic impacts with their E3ME model.

Both reports published are now available online (after free registration) :

- DG ENV: Macroeconomic impacts of shale gas extraction in the EU

- DG CLIMA: Mitigation of climate impacts of possible future shale gas extraction in the EU: available technologies, best practices and options for policy makers.

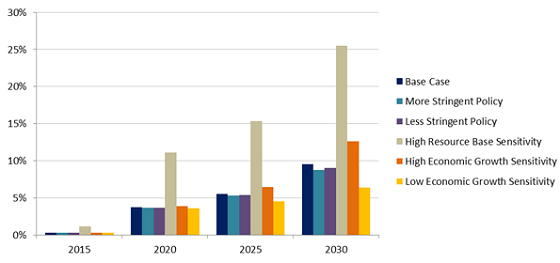

Some key results from both reports are :

- Production of shale gas starts with over 1 bcm in 2015 and ramps up gradually to between about 30 bcm (low economic growth) and about 130 bcm (high resources) in 2030, with development trends pointing to higher volumes expected after 2030 for all scenarios.

- Production levels differ relatively little between risk management policy options (-8% with the more stringent policy option explored compared to the base case).

- Conventional gas production is largely not impacted between scenarios assumptions, due to uniformly geologically depleting resources in the EU and to similar gas prices between scenarios.

- In all scenarios, including the sensitivity run with high domestic shale gas production (with the more stringent policy scenario), the exposition of the EU to international markets is such that the differences in domestic shale gas production have little effect on global supply and thus on international gas prices. As a result, prices between scenarios are largely similar, and we observe essentially a trade-off between domestic shale gas production and imports in all scenarios defined by internal EU factors (i.e. risk management policies and domestic shale gas resources).

- In all cases, the contribution of shale gas to domestic gas consumption gradually reaches around 10% in 2030, i.e. 15 years after start of production (except in the “high resources” scenario, which does not take into account any possible access restrictions due to Natura 2000 areas or population density, where it reaches 25%).

- With gas prices being significantly similar between scenarios, the only differentiating factor between scenarios for total gas demand and total CO2 emissions in the EU is economic growth.