REQUEST THE FULL PUBLICATION (FREE)

The curse of marginal costs

This publication was written using an analysis carried out jointly by an Enerdata expert in energy sector innovations and a weather risk management expert from New-Re (Munich-Re group), one of the main global reinsurers.

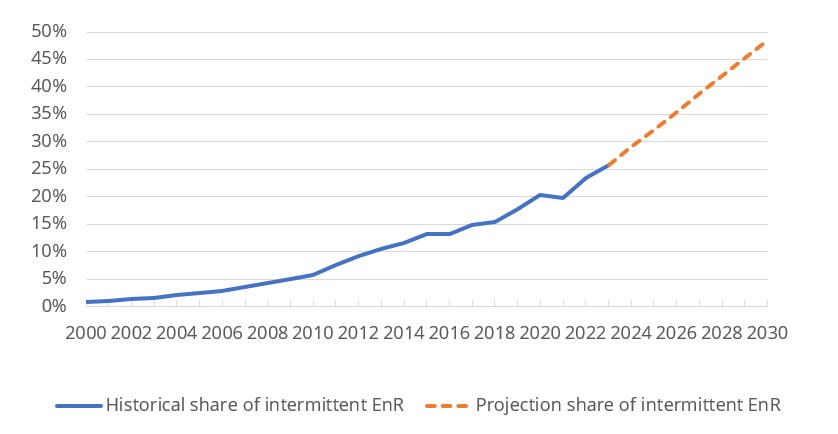

In the last 5 years, the amount of energy provided by renewable sources has increased dramatically (up by 39% since 2017 in Germany) and is expected to satisfy one third of EU requirements in 2026. This change has produced unexpected volatility in energy prices due to the unpredictability of renewable energy output.

The net demand (demand minus renewable energy output) indicates the amount of electricity required from dispatchable assets and is therefore a main driver of power prices.

- In hours with high renewable energy outputs, the net demand falls, so very few dispatchable assets are required and power prices plummet (sometimes becoming negative).

- In hours with low renewable energy outputs, dispatchable assets are required and the European markets (particularly those with little hydro or nuclear) experience much higher power prices.

The cannibalisation effect occurs when too much availability of renewable assets creates higher sales, which then puts pressure on power prices and drives them down.

In addition to the cannibalisation effect, the increasing gap between the highest and the lowest net demand during a day is a massive challenge for conventional power plant operators, and the intrinsic design of power spot markets combined with increasing capacity of intermittent renewable energy sources (IRES) poses ever greater challenges to all energy asset owners.

Share of intermittent renewables in total EU power generation

Source: Enerdata - Global Energy and CO2 Database

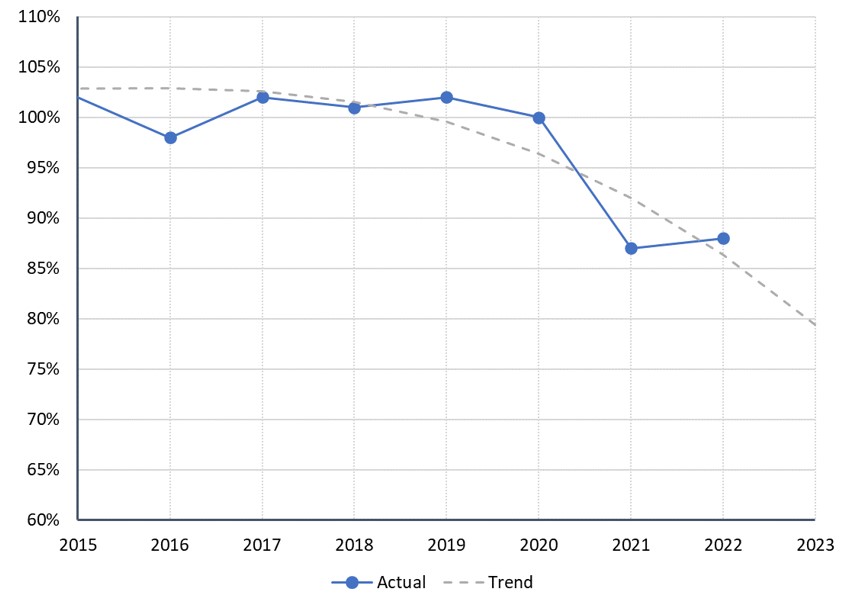

The most powerful way to visualise and quantify this challenge is to compare the sum of the hourly revenues over a certain period with the total cumulative product valued at the average price. This ratio, the “Quality Factor", quantifies the difference between the cost of selling hourly production on the spot market and selling it at the average base price (typical hedge on the future market).

Spanish Solar Annual Quality Factors

Source: New Reinsurance’s calculation based on Speedwell’s production index and EPEX data

The average power prices, and the misalignment between renewable production profiles and power price levels is a threat to the financial viability of these assets.

To avoid negative prices putting energy asset owners out of business requires implementation of new market design or technological mitigation measures. Energy firms, renewable investors, local municipalities, and an increasing number of other industries, will have to actively hedge the volume risk of hydroelectric, wind, and solar parks, and progressively add cannibalisation risks.

The inevitable transition of power markets towards zero-marginal-cost systems will surely continue over the coming years with new low carbon and renewable technologies. The cannibalisation effect reveals the necessity of flexible assets for our power systems: electric vehicles, load management, large electricity storage, hydrogen production, etc. as well as new hedging and risk management solutions.