Is thermal storage the key to the Clean Industrial Deal?

Request this Executive Brief in PDF format (FREE)

Industrial heat makes up two-thirds of industry's energy demand and nearly a fifth of global energy use. Most of it still produced by burning fossil fuels. As Europe moves to electrify its factories, "Power to Heat" systems will struggle to compete with natural gas unless they can store energy: generating heat when electricity is cheap or abundant, and recovering waste heat from intermittent processes. Yet no single technology has emerged as the standard. In this brief, we benchmark the thermal storage solutions now available in Europe and weigh their potential to make industrial heat both clean and competitive.

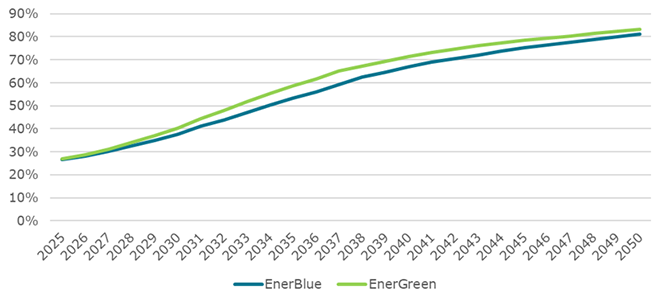

In 2024, industry accounted for nearly 20% of CO2 emissions in the EU (Source: Enerdata Global Energy & CO2 Database). The European Union has set binding climate objectives through the European Climate Law: reducing greenhouse gas (GHG) emissions by at least 55% by 2030 compared to 1990 levels, and achieving carbon neutrality by 2050, with industry as a key sector in this effort. To achieve this, two major plans structure European action: the European Green Deal, which establishes the overall regulatory framework (green taxonomy, strengthened EU Emission Trading Scheme, energy efficiency directive), and the Clean Industrial Deal, launched in 2025, which specifically aims to make decarbonisation a driver of industrial competitiveness by supporting the electrification of processes, the deployment of heat storage, and access to affordable energy for energy-intensive industries. The share of renewable energy in industry is therefore expected to rise from 20% today to nearly 50% by 2035 if national targets are hit (Enerdata, EnerFuture, EnerBlue and EnerGreen scenarios1). These renewable energies in industry are primarily used for heat production.

Figure 1: Share of renewables in industry consumption in the EU

Source: Enerdata, EnerFuture

The deployment of electric boilers and so-called 'high-temperature' heat pumps is one of the key means of electrification and decarbonisation for industry.

The generic term 'Power to Heat' designates systems that convert electricity produced from renewable sources into heat. It is generally composed of an electric boiler or heat pump, heat exchangers, and a thermal battery.

These Power to Heat technologies must be able to compete with natural gas, which is currently the primary energy source used for heat production in industry. They must also be capable of adapting to the fluctuating power requirements, temperatures, and needs of industrial processes. Their deployment therefore faces numerous challenges, particularly the need for storage.

Thermal storage is a key technology for enabling competitiveness against natural gas because it can optimise the costs of a Power to Heat project, notably through two means:

- Leveraging energy price fluctuations to produce and store heat during hours of low and negative prices and/or photovoltaic overproduction.

- Recovering and storing waste heat from intermittent industrial processes and reusing it.

These energy price variations and industrial process patterns are the main justifications for installing a thermal battery. However, this market remains emerging and so far, no single technology has established dominance. We will therefore examine the different options currently available.

Benchmark of thermal storage technologies

Before presenting the technologies, it is important to recall that there are three temperature levels in industry:

- Low Temperature (LT): below 100°C with industrial processes using hot water (food, processing industry, etc.)

- Medium Temperature (MT): between 100 and 300°C with steam and superheated water processes (chemistry, plastics, etc.)

- High Temperature (HT): above 300°C with processes using burners (glass, steel, etc.)

For low temperatures, the most commonly used heat storage materials are water and glycol water. However, new solutions are emerging, such as Phase Change Materials (PCM) or refractory bricks. This temperature segment is the most technologically mature with numerous projects already implemented.

This is not the case for the medium and high temperature segments, where no single solution has established dominance and each material has its advantages and disadvantages in terms of efficiency of charge/discharge cycles, energy density, temperature range accepted by the solution, and most importantly, in terms of price.

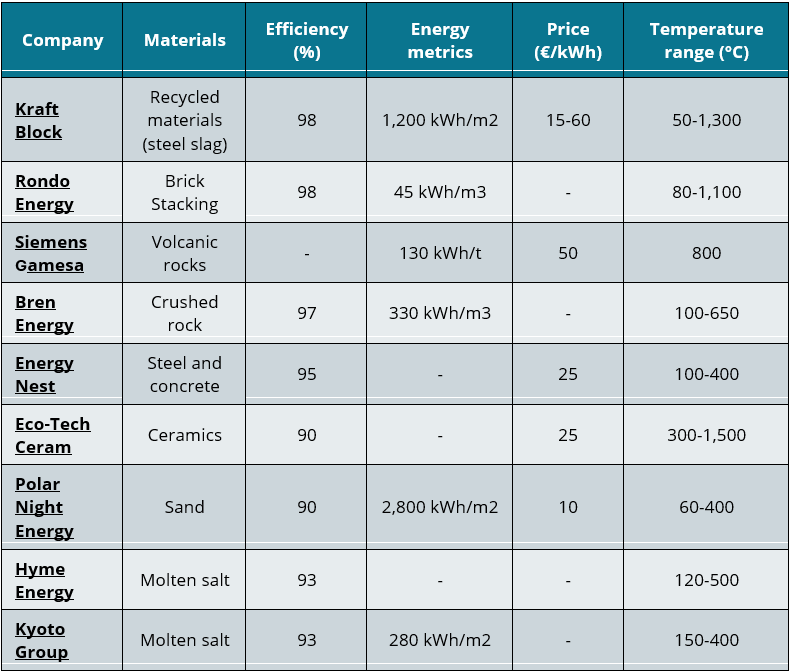

Despite the lack of maturity, a general technological trend is emerging for medium temperature applications: the use of readily available and low-cost materials, such as sand, steel slag, crushed rock, or molten salts.

Finally, for high temperatures, industrialised technologies are limited to recycled materials such as steel slag, bricks, or ceramics.

The technologies mentioned above are summarised in the table below, which lists the main commercial thermal energy storage solutions (medium and high temperature) currently available in Europe. Apart from Hyme Energy and Kyoto Group—both of which use molten salts—each company offers a distinct solution.

Figure 2: Heat storage technology benchmark (non-exhaustive)

Source: Enerdata

Innovative Economic Models to Make Industrial Heat Storage Profitable

CAPEX, the main challenge for Power to Heat projects

Industrial thermal storage can prove cheaper than other storage technologies, with investment costs lower than conventional electrochemical batteries. Where a lithium-ion battery requires between 200 and 300 euros per kWh, a sensible thermal storage system such as Polar Night Energy's sand battery2 or Kraftblock's3 high-temperature modules can be installed for only 10 to 60 euros per kWh4, a cost ratio 3 to 30 times lower.

Additionally, thermal batteries can generate additional revenue, since they can participate in flexibility markets (such as frequency reserves and other mechanisms) and engage in arbitrage on electricity spot markets. Polar Night Energy, through its sand battery, already takes part in Finland’s primary and secondary frequency reserve markets, achieving a 50% increase in returns over the project’s lifetime compared to a standard electrification project without a battery5. It is worth noting that the potential earnings from these markets are highly dependent on the local context (further details are available in Flex Enerdata’s product).

Despite the competitive nature of the thermal battery itself, its installation must be coupled with energy conversion technologies (electric to thermal) and heat recovery (heat exchangers). The total cost of a Power to Heat project can therefore quickly increase with the electric boiler or heat pump plus the thermal battery plus the heat exchangers. To be competitive, the complete solution must be able to provide heat at a kWh price equivalent to or lower than that of natural gas (including carbon pricing for large industrial users).

Heat-as-a-Service: A financing model that removes the last obstacles

For industrials reluctant to mobilise capital on still-emerging technologies, the Heat-as-a-Service (HaaS) model constitutes a decisive response. A pioneer of this approach, the Norwegian group Kyoto Group has deployed its 56 MWh Heatcube at KALL Ingredients in Hungary without a single euro of CAPEX being requested from the industrial client: the Kyotherm investment fund financed the installation via a dedicated company (SPV), while KALL signed a 15-year guaranteed-price decarbonised heat supply contract, in complete replacement of its natural gas boilers. This model transforms capital expenditure into a predictable operating charge.

According to McKinsey, heat electrification projects combining heat pumps and thermal energy storage could achieve an internal rate of return (IRR) of around 15% by 2030 as renewable electricity prices continue to fall, and flexibility markets develop across Europe—making industrial thermal storage one of the most attractive energy assets of the next decade. (Source:mckinsey: industries-energy-and-materials/our-insights/blog/industrial-heat-electrification-in-europe-new-business-models-emerge).

Major Projects Already Under Implementation

Thermal batteries for industries and district heating

Numerous battery projects are already being implemented across Europe. One of the most emblematic is the system installed by Finnish startup Polar Night Energy in Pornainen, Finland. This project consists of 2,000 tons of soapstone and can reach temperatures up to 500°C. It supplies the local district heating network and has a storage capacity of 100 MWh.

For industries requiring large heat volumes, German group Energy Nest inaugurated in 2025 one of Europe’s largest industrial thermal storage systems at the Leonhard Kurz thin-film processing plant in Fürth, Germany. This project is composed of a 3 MWe electric heater and a 12 MWhth ThermalBattery™ integrated into the existing thermal oil infrastructure delivering over 3 GWhth of clean heat annually and covering over 70% of the heat demand for one production line with over 40% coming directly from stored heat. Another notable example is the industrial electrification project led by German company KraftBlock, which involves deploying two 35 MWh units in a food processing plant.

It is notable that these projects are led by stakeholders with multi-year visibility into their operations, which facilitates investment, and who face no land or operational constraints for hosting storage systems on their sites. Indeed, these factors, combined with the lack of national clarity regarding decarbonisation goals and regulations for industry, make project deployment uncertain. Nevertheless, these three projects illustrate a clear dynamic: industrial thermal storage can become a key technology for the decarbonisation of European industry.

KEY TAKEAWAYS

- The question of costs is not yet fully resolved: Indeed, while thermal storage costs are relatively low at 10 to 60 €/kWh, the overall cost of electrification projects remains a major barrier for industries especially in an unstable political and regulatory context that prevents long-term planning.

- European reference projects that prove technological maturity: From a sand battery in Finland (100 MWh), to steel slag modules at PepsiCo in the Netherlands to the molten salt Heatcube in Hungary (56 MWh, 30 GWh/year of clean heat), several concrete industrial projects demonstrate that thermal storage is now operational at large scale in Europe.

- Innovative financing models to remove investment barriers: The complete Power to Heat system (boiler plus heat recovery plus storage) represents by its total cost a brake on adoption. The Heat-as-a-Service (HaaS) model, allows industrials to decarbonise their heat without CAPEX, via a long-term supply contract (15 years) financed by third-party investors—a model that, combined with valorisation on electricity flexibility markets, could unlock significant deployment.

Notes:

- EnerBlue Scenario: Achievement of new NDCs submitted up to end of 2024; EnerGreen Scenario: Ambitious GHG emissions budget in line with the Paris Agreement.

- Polar Night Energy publication

- KraftBlock publication

- Benchmarking thermal energy storage cost for industrial process heat, Osti

- Reserve markets offer additional revenue potential, Polar Nignt Energy publication