Energy dilemma: Balancing economic growth with decarbonisation

Get this executive brief in pdf format

India became the most populated country in the world this year, with 1.4 billion inhabitants, overtaking China. As the nation strides forward with the strongest economic growth among G20 countries, energy demand is booming. In the pursuit of a sustainable future, India stands at the forefront of a monumental energy transformation. Fuelled by a one-of-a-kind young and educated workforce, India is poised to have the second-largest GDP (in PPP terms) behind China, within the next 30 years. An immense green technology market potential is triggering investments, but much remains to be done for India’s energy transition. Against the backdrop of towering challenges and boundless opportunities, the decarbonisation journey is still in its early stages. During COP 26, the country endorsed emission reduction commitments, setting a net-zero target for 2070. However, the climate policy agenda lacks consistency, as the priority is comprehensively given to poverty alleviation, from which millions of Indians still suffer.

As energy needs continue to grow, the challenge of phasing-out coal in India is massive. However, the rapid birth of hi-tech industries and infrastructures draws a profitable landscape to build a highly competitive domestic market for clean technologies. In recent years, the country has made significant strides towards embracing renewable energy sources. The dual challenge of meeting its escalating energy demand and sustain economic growth remains of utmost importance for the country’s welfare.

India’s (or Bharat’s) G20 presidency this year, with the New Delhi summit held on September 9-10th, was an opportunity to reinforce its diplomatic stance and attract investments, amidst geopolitical tensions with the war in Ukraine. Ahead of COP28 in December, this report delves into the Indian energy transition journey. We hereby present the key elements shaping the fascinating potential of the energy market in India.

Unrivalled economic potential challenged by climate fallouts

Fastest growing G20 economy, booming energy demand

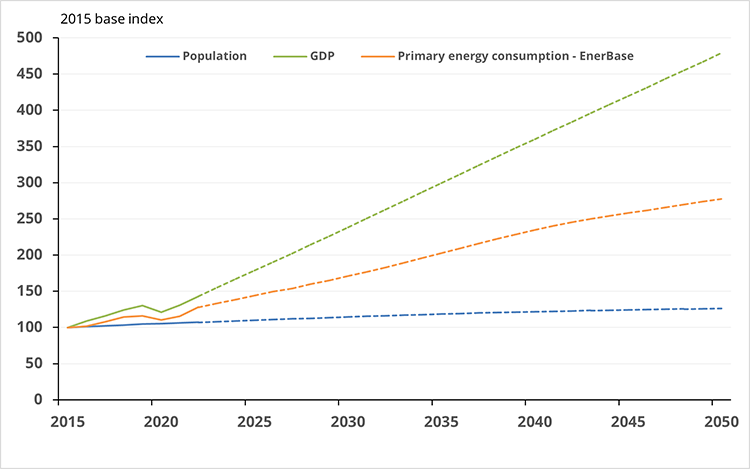

India is on track for the decade’s most substantial surge in . Unlike the aging populations in China, Japan and European countries, India’s population is thriving, driving robust domestic demand supported by a youthful workforce. Consequently, the country is expected to be the fastest growing G20 economy, sustaining a GDP growth rate above 6% throughout the decade. Primary energy demand is projected to rise by 3-4% annually for the next 10 years before levelling off to 1-2% in the long term.

Figure 1 : A huge demand to fill in the short-term

Sources: Enerdata, Enerfuture

Taking a step back in 2010, India had an electrification rate just above 75%. Through the “Power for all” plan, over 99% of households now have electricity access. Significant progress has been made in developing energy capacities and grids. The Central Electricity Authority of India anticipates a power requirement increase to 817 GW by 2030, up from the 482GW installed capacity in 2023 (of which 32.5% from renewables).

Rapid industrialization, digitalization, and high-tech development urge further energy needs. If most of the later were filled through fossil fuels (coal still represents 55% of the power mix), India has broadly scaled up its renewable energy capacities. They have more than tripled over the past 7 years, with a strong emphasis on solar. Hydro capacities grew from 42 to 52 GW since 2015, wind installations nearly doubled from 25 to 42 GW, while solar capacities soared from 5 to 63 GW.

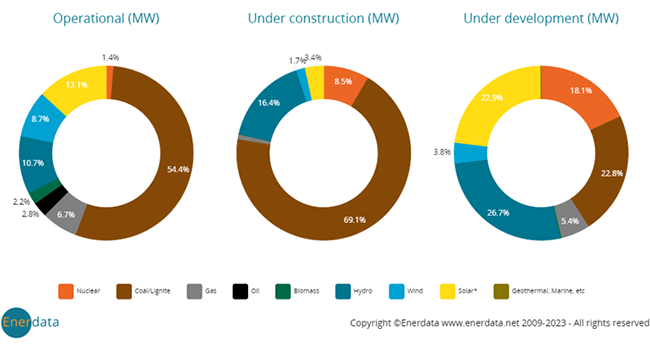

The power sector is undergoing significant changes, shaping the industrial outlook. In the short-term, coal plants still occupy almost three quarters of projects under construction, as dozens of lands were recently sold by the government for coal mining. In the meantime, India is likely to carry out a massive push towards solar, nuclear and hydroelectricity over the next ten years. This trend is depicted by our Power Plant Tracker service which covers operational and future plants (Figure 1).

Figure 2: Power plants technology mix in India – May 2023

Sources: Enerdata, Power Plant Tracker

Third largest CO2 emitter, best of its class though

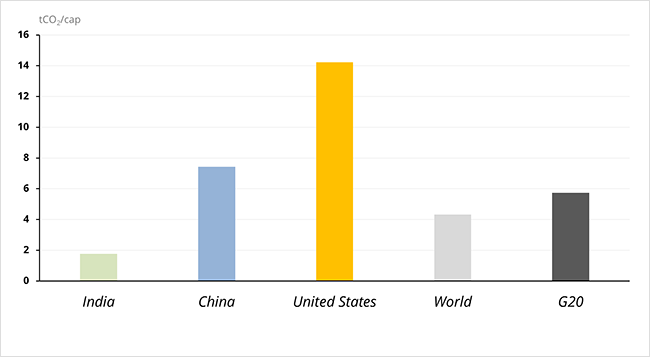

Unsurprisingly, India ranks second in coal production and consumption, following China. Production spiked by 14% last year, reaching 937 Mt in the wake of the gas crisis. As of 2022, India is the 3rd largest CO2 emitter with 2.8 Gt. However, it is important to clarify that while India’s emissions are substantial in volume, they remain far from the USA (5.0 Gt) and China (12.6 Gt). Additionally, India recently became the world’s most populous country with 1.43 billion inhabitants, surpassing China. Population size significantly impacts emissions. In per capita terms, India emits 1.9 tCO2/cap, well below the global average of 4.7 tCO2/cap. In fact, India has the lowest per capita emissions among G20 countries, despite being the third-largest global emitter.

Breaking down emissions by sector, the energy sector accounts for 47%, followed by industry at 34% (including direct fuel combustion and process), 12% from transports and 7% from residential and tertiary sectors.

Although it is crucial for India to reduce emissions, its burden and responsibilities fall miles behind those of the USA, China, or the EU. In the coming years, whether India meets its growing energy needs with fossil fuels or green alternatives will determine its emissions' trajectory. The country stands at a pivotal moment, balancing economic growth and the imperative to mitigate climate consequences if domestic emissions continue to rise.

Figure 3: Per capita CO2 emissions in 2022

Sources: Enerdata, Global Energy & CO2 Data

Climate hazards due to global emissions already hit the country hard

India has already been witnessing increasing temperature and irregular precipitations over the last few years. Many lands experienced devastating floods, heat waves or water stress, killing thousands, forcing millions to leave their home, and destroying crops. In addition, air pollution became a significant concern, particularly in densely populated areas where respiratory issues are spreading. As climate hazards will undoubtedly intensify, India faces the urgent need to adapt as South Asia and Sub-Saharan Africa are the most exposed regions. The most vulnerable states in India have seen slower growth and persistent poverty, with agriculture, forestry, and fishing at greater risk. More frequent natural disasters also deal severe damage to infrastructure, disrupt supply chains, and contribute to inflation. Therefore, environmental issues are a crucial matter for public health and long-term development in India.

Back in March 2019, India launched the Cooling Action Plan, a pioneering country-level effort for global warming resilience. Local governments have also implemented decentralized heat action plans in selected areas, as extreme temperatures threaten liveability. The Indian government has made climate an important focus, working on comprehensive action plans with international support.

Jumping on the bandwagon of decarbonisation

Quantified policies have been defined

India was lacking political agenda and climate commitments for years. During COP26 in Glasgow, PM Modi announced India’s pledge to achieve net-zero emissions by 2070. The target set is further in time compared to the usual 2050 target by most G20 countries. Nonetheless, it remains an important step. India has made notable progress in implementing its climate agenda, primarily by increasing the share of renewables in energy production and enhancing energy efficiency. The country boasts one of the lowest energy intensities among emerging countries.

Given its robust demographics and economic growth, the target may still appear ambitious. Colossal infrastructure investments to switch from fossil fuels to clean energy sources will be needed. As India is currently focused on leveraging its GDP growth, the peaks in emissions and energy consumption are not yet in sight.

Some quantified objectives and measures include:

- Allocation of $2.6bn from the Union Budget 2022-2023 for a Performance-Linked Incentive scheme to boost manufacturing of high efficiency solar modules.

- Plans to establish 21 new nuclear power reactors with a total capacity of 22 GW by 2031.

- A 45% cut in carbon intensity by the end of the decade (compared to 2005 level).

- A target of achieving a 50% share of renewables in total power capacity by 2030 (up to 500 GW).

To accelerate the shift away from fossil fuels, strong incentives like subsidies or carbon taxes will be necessary. A recent IMF report1 suggests that scaling up current renewable policies can help save many irreversible fixed costs associated with coal plants. Increased investment in renewables can amortize spending and foster long-term growth. Therefore, sticking with coal for too long could have harmful opportunity costs for future growth.

Seizing the opportunities of low carbon technologies and knowledge

Low-carbon technologies could create a market worth up to US$ 80 billion in India by 2030. The private sector has a key role by endorsing the opportunities to become global market leaders. Major Indian corporations like Adani or Tata have already made significant investments and are expected to conduct greater fundings into carbon-free technologies.

In FY22, Indian investments in renewable energy hit a record $14.5bn, more than twice the 2021 amount. This surge in capital flows is driven by the growing cost-competitiveness of green alternatives. India is home for one of the lowest per-unit installation costs for renewable energy, if not even the lowest worldwide2. Estimates suggest that by leveraging low-carbon technologies, India could add $1tn to its GDP by 2030. The government is multiplying auctions for wind and solar projects to maximize growth potential.

The energy sector opportunities in India are unrivalled worldwide. The key question is whether India can seize this opportunity and to what extent. The government and private sector are expected to focus on climate finance, energy security, and green hydrogen, facilitating fundings and technology provision. As the world is still in the early stages of green industrial revolution, India has a unique chance to emerge as an innovation hub. Levers include R&D investment and incentives for hi-tech companies blooming in India. The vast pool of highly skilled workers is a valuable asset for the Indian energy and technology market. On top of that, the opportunity lays on a multifold increase in domestic capital flows for greener consumption patterns, and substantial FDIs inflows to develop infrastructures and international partnerships.

A strong emphasis on electric vehicles, hydrogen, and CCUS

The Indian government launched the “National Hydrogen Mission” to produce at least 5 Mt of green hydrogen annually. This initiative aims to position India as a leading global supplier, reduce fossil fuel dependence and create business opportunities. Currently, most hydrogen production in India (and globally) is derived from fossil sources. However, the hydrogen alternative appears quite realistic in India. A large fuel shift in the transport sector can occur in the next decade, especially for heavy vehicles such as trucks or buses.

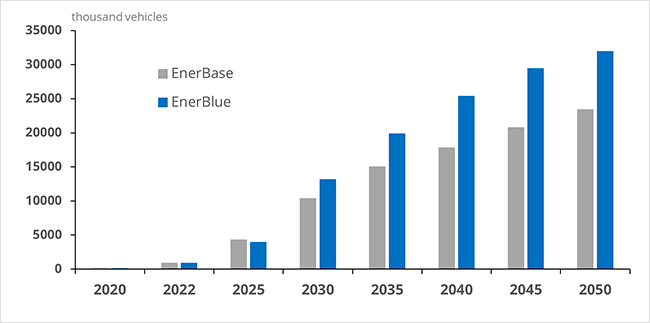

According to the Ministry of Road Transport, electric vehicle sales reached one million units in 2022, up from 320,000 in 2021, with car companies investing heavily to promote EV market penetration. India, as the third-largest automobile market, is poised for one of the fastest-growing EV industries, with a projected annual purchase of 10 million EVs by 2030. Moreover, in February, a 5.9 Mmt lithium reserve, the sixth largest known in the world was discovered in northern India. It will considerably propel India as a major player in global battery production.

Figure 4: Annual EV sales forecasts in India

Source: Enerdata, EnerFuture

Furthermore, there is no path towards net-zero in India without a wide adoption of Carbon Capture, Utilisation and Storage technologies in both industrial and power sectors. CCUS technologies could reduce GHG emissions by up to 50% in key industrial branches such as cement production. Although CCUS initiatives and projects are in their early stages, deployment is part of the policy agenda. India can become a major player in CCUS development, either through investment in foreign technologies or by taking a lead role in their development.

Sectoral breakdown and emissions path in a nutshell

This section presents several insights regarding 2050-scenarios on energy and emissions. The calculations are built according to our in-house POLES model. The model is divided into 3 scenarios, for which the characteristics can be found in the appendix.

A much smaller emission burden to handle

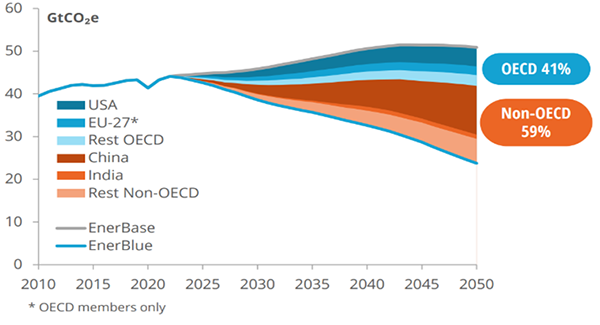

As previously mentioned in this report, India contributes to 7% of global GHG emissions, despite its population representing approximately 18% of the world’s total. Consequently, when it comes to designing global net-zero scenarios, India’s burden turns rather small. Figure 4 illustrates the emissions gap between the baseline scenario and the fulfilment of NDCs.

To put this in perspective, China alone should account for 36% of the cumulative emissions' reduction (equivalent to 141 GtCO2e of avoided emissions) to meet global pledges. In contrast, India’s efforts constitute only 4% of the required cut in emissions (15 GtCO2e).

Figure 5: Emissions reduction scenarios for NDC pledges achievement

Sources: Enerdata, EnerFuture

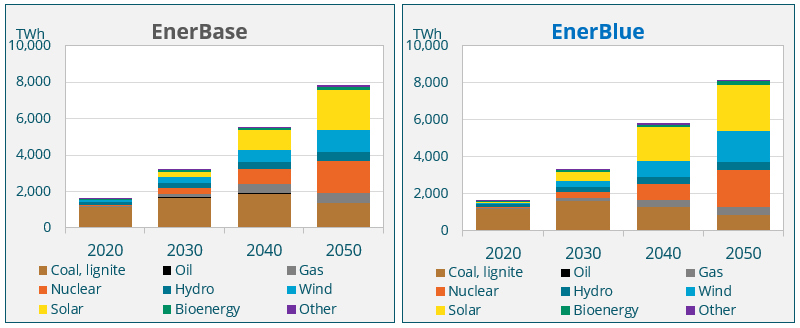

A nuclear and renewable push to compensate gradual coal phase-out

India’s power generation needs are set to quadruple by 2050. Indeed, it won’t ease a coal phase-out. However, a notable aspect of India’s energy transition projects is the massive deployment of nuclear power plants. By 2050, India’s nuclear generation is projected to reach a staggering 1 900 TWh, making it the top global player. Potentially, if the government’s ambitions are met, India could account for 35% of the world’s nuclear power generation. Starting virtually from scratch, nuclear power is expected to comprise up to 25% of the nation’s power mix.

On the renewables front, solar power generation is already on a promising trajectory. It should generate around 2 000 TWh accounting for another 25% of the electricity mix. Wind power has similar targets if coal phase-out goals are met, including an offshore wind energy potential estimated at 70 GW (The first offshore project was launched in 2019). Hydroelectricity and bioenergy are expected to remain secondary sources in the future power mix, though any capacity increases will contribute to the transition.

Figure 6: Power mix scenarios

Sources: Enerdata, EnerFuture

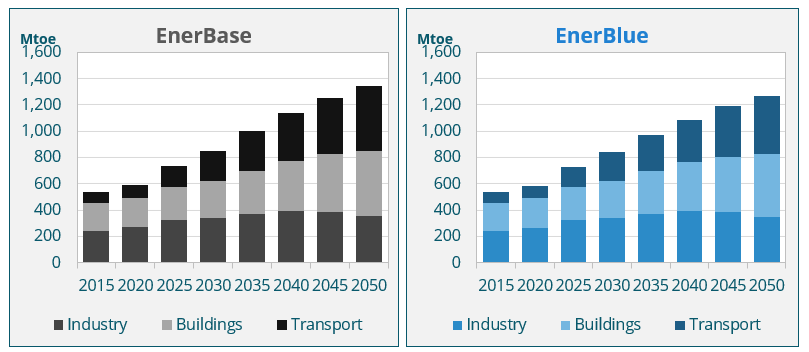

Improve energy efficiency in transports and industrial sectors

To align with a 2°C warming scenario, total final consumption should not exceed 1,200 Mtoe. Our calculations point towards a 2.5%/y average growth in primary energy consumption by 2050. Therefore, to meet its targets, India has to achieve significant energy savings through improved efficiency, with the key sectors being industry and transportation. In the EnerBlue scenario, final energy consumption in the industrial sector should decrease by nearly 15% between 2030 and 2050, representing over half of the required energy savings. However, optimizing energy usage without compromising overall industrial output will be very challenging.

Figure 7: Sector-level final energy consumption

Sources: Enerdata, EnerFuture

KEY TAKEAWAYS

- India is experiencing the strongest economic growth among G20 countries (around 6% annual GDP growth expected over the decade). Hence, a strong energy demand needs to be filled. The balance between economic growth and sustainability is challenging.

- India is highly dependent on coal to meet its energy needs, and coal consumption will continue to grow for years. However, renewable investments have skyrocketed, particularly on the PV side. The country also aims to operate a massive nuclear push.

- South Asia is among the most vulnerable regions to climate disasters. India already struggled with unprecedented heat waves and floods. Although India is not exempted from any emission cut efforts, its contribution to global emissions in the lowest of G20 countries in per capita terms.

- Quantified policies have been committed with a net zero-target by 2070.

- India is a massive market for low carbon technologies and innovation. Fed by a large and qualified manpower and hi-tech industries, it is expected to attract a sharply growing amount of FDIs. The potential for India to become a massive green hub is enormous and offers a wide range of opportunities for growth.

- India is still at an early stage of energy transition despite the recent push in renewables and energy efficiency improvements. Electrification in the transport sector and a rapid decline in the carbon intensity of industries will be key catalysers of the country’s decarbonisation.

- Adopting a neutral point of view, it is hard to blame India for its high volume of emissions. A question mark remains on the country’s willingness and ability to adapt rapidly to climate change. However, what appears straightforward as years fly is that the opportunities on the energy front are unique in India.

Notes

- IMF, India Article IV Consultation; Staff Report, December 2022

- WEF, Mission 2070: A Green New Deal for a Net Zero India, November 2021